If you own a free standing home in Everton Park, QLD 4053, you've probably wondered whether you're paying a fair price for your home and contents insurance — or quietly overpaying year after year. This article breaks down a real insurance quote for a five-bedroom brick veneer home in the suburb, benchmarks it against local, state, and national data, and offers practical tips to help you get the best value cover.

---

Is This Quote Fair?

The quote in question comes in at $1,877 per year (or $184/month) for combined home and contents insurance, covering a building sum insured of $550,000 and $50,000 worth of contents, with a $500 excess on both.

Based on our pricing data, this quote is rated CHEAP — below the suburb average for Everton Park. Across 23 comparable quotes collected for postcode 4053, the suburb average sits at $2,567/yr and the median at $2,535/yr. This quote falls well below even the 25th percentile of $1,931/yr, meaning it's cheaper than at least three-quarters of comparable quotes in the area.

In plain terms: this is a genuinely competitive quote. For a five-bedroom home with ducted climate control, solar panels, and timber/laminate flooring — all features that can push premiums higher — landing under $1,900 per year is a strong result.

That said, price alone shouldn't drive your decision. It's worth reviewing what's included in the policy, particularly around storm damage, escape of liquid, and accidental damage cover, to ensure the low premium isn't the result of stripped-back inclusions.

---

How Everton Park Compares

To put this quote in broader context, here's how Everton Park's insurance costs stack up against the rest of Queensland and the country:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Everton Park (4053) | $2,567/yr | $2,535/yr |

| Moreton Bay LGA | $3,435/yr | — |

| Queensland | $9,129/yr | $3,903/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out here. The Queensland state average of $9,129/yr is dramatically inflated by high-risk postcodes — particularly cyclone-prone coastal and far-north Queensland regions — which skew the mean significantly upward. The state median of $3,903/yr is a more representative figure, and Everton Park's median of $2,535/yr sits comfortably below it.

Compared to the national average of $5,347/yr, Everton Park also fares well. The suburb's proximity to Brisbane, its relatively modern housing stock, and its position outside cyclone risk zones all contribute to more moderate premiums than much of regional Queensland.

The Moreton Bay LGA average of $3,435/yr is notably higher than the Everton Park suburb average, suggesting that other parts of the LGA — potentially areas with greater flood or storm exposure — are pulling that figure up. Everton Park homeowners are in a comparatively favourable position within the broader region.

---

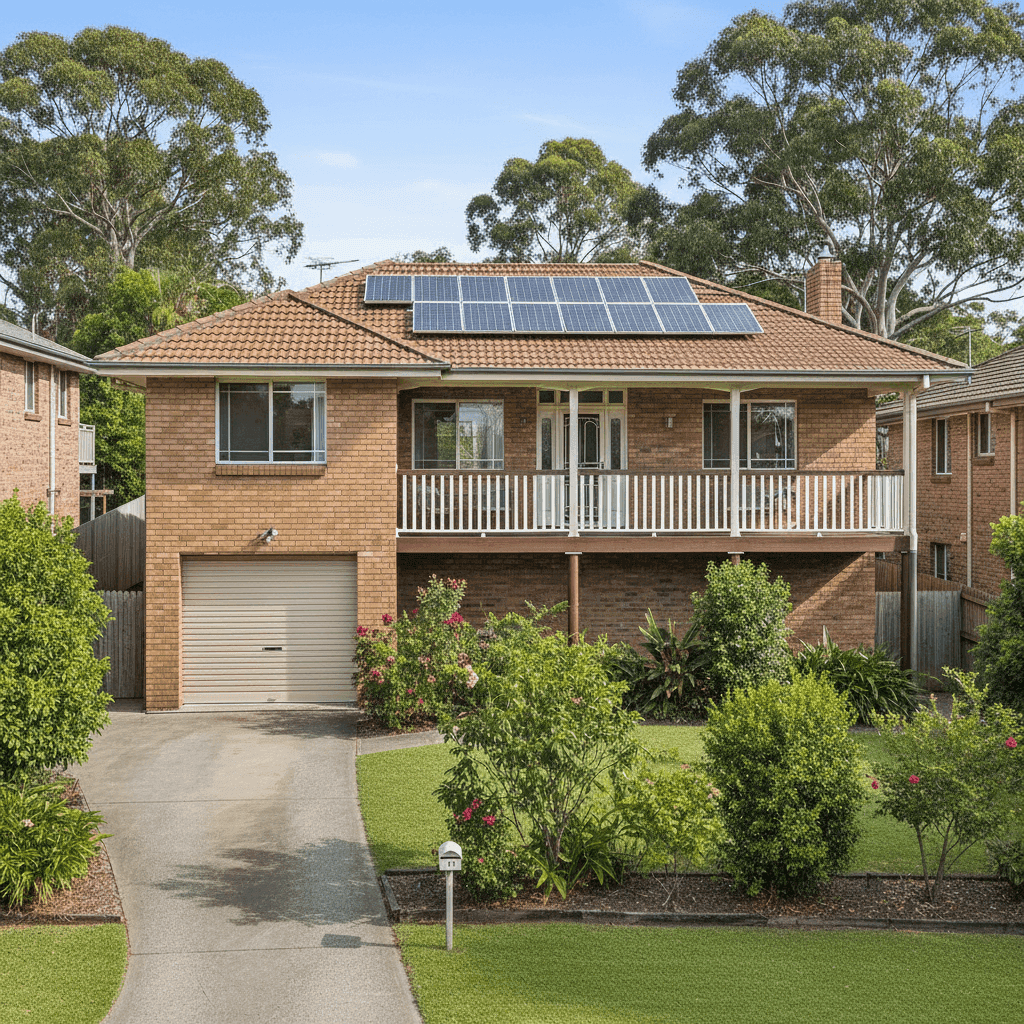

Property Features That Affect Your Premium

Several characteristics of this property influence how insurers price the risk — some favourably, others less so.

Brick veneer construction with a tiled roof is generally well-regarded by insurers. Brick veneer walls offer solid resistance to fire and moderate weather events, while tiles are considered a durable roofing material. Together, these features typically attract lower premiums compared to timber-framed or Colorbond-roofed homes.

Slab foundation is a neutral-to-positive factor. Concrete slabs are structurally sound and don't carry the same moisture and pest risks associated with older timber subfloors, making them straightforward for insurers to assess.

Elevated by at least 1 metre is an interesting characteristic for this property. While Everton Park isn't a designated cyclone risk area, elevation can be a double-edged sword. In flood-prone areas, being raised off the ground is a significant premium reducer. In non-flood areas, some insurers may treat elevated homes with slightly more caution around wind uplift risk — though this is generally minor for a well-built brick veneer home.

Solar panels add replacement value to the roof and can slightly increase the cost of a claim if damaged. Homeowners should confirm their policy explicitly covers solar panels as part of the building sum insured, as some policies treat them as an optional add-on.

Ducted climate control is a high-value fixture that contributes to the building sum insured. At 235 sqm, this is a sizeable home, and ensuring the $550,000 building sum insured accurately reflects current rebuild costs — including the ducted system, quality fittings, and timber/laminate flooring — is essential to avoiding underinsurance.

Timber and laminate flooring can be costly to repair or replace following water damage events. Escape of liquid claims (burst pipes, leaking appliances) are among the most common home insurance claims in Australia, and quality flooring is a significant cost driver in those scenarios.

---

Tips for Homeowners in Everton Park

1. Check your building sum insured annually Construction costs have risen sharply across Australia in recent years. A sum insured of $550,000 may have been accurate at the time of the quote, but it's worth reassessing each year using a building cost calculator to ensure you're not underinsured. Underinsurance is one of the most common — and costly — mistakes homeowners make.

2. Confirm solar panel coverage Solar panel systems represent a meaningful investment. Before renewing or switching policies, confirm whether your panels are covered under the standard building definition or whether a separate endorsement is required. Also check whether the policy covers inverter failure or just physical damage.

3. Review your contents sum insured $50,000 in contents cover is on the lower end for a five-bedroom, three-bathroom home. Take stock of your furniture, appliances, electronics, clothing, and valuables — many homeowners are surprised to find their actual contents value exceeds their insured amount. A shortfall here could leave you significantly out of pocket after a major claim.

4. Compare quotes at renewal time Even with a competitive premium like this one, the insurance market shifts each year. Insurers reprice risk based on claims data, reinsurance costs, and weather events. What's cheap today may not be the best value at your next renewal. Get a fresh quote at CoverClub before auto-renewing to make sure you're still getting a fair deal.

---

Find the Right Cover for Your Home

Whether you're buying a new policy or reviewing your current one, comparing quotes is the single most effective way to ensure you're not overpaying. CoverClub makes it easy to benchmark your premium against real data from your suburb and beyond.

Compare home insurance quotes for Everton Park today — it takes just a few minutes and could save you hundreds of dollars a year.