If you own a free standing home in Fennell Bay, NSW 2283, you're likely no stranger to the beautiful Lake Macquarie lifestyle — but you may be wondering whether you're paying a fair price for home insurance. This article breaks down a real home and contents insurance quote for a three-bedroom, two-bathroom weatherboard home in the suburb, and puts the numbers into context so you can make a more informed decision at renewal time.

---

Is This Quote Fair?

The quote in question comes in at $4,108 per year (or $394 per month) for combined home and contents cover, with a building sum insured of $650,000 and contents valued at $140,000. Both the building and contents excesses are set at $1,000.

Our pricing engine rates this quote as Fair — Around Average. That's a meaningful result. It tells you the premium isn't a bargain, but it's also not an overpriced outlier. For a property with several risk-relevant features (more on those below), landing near the middle of the market is a reasonable outcome.

That said, "fair" doesn't necessarily mean you can't do better. Insurance pricing varies significantly between providers, and even a modest improvement could save you hundreds of dollars a year.

---

How Fennell Bay Compares

To understand what this quote really means, it helps to look at the broader pricing landscape. Here's how the $4,108 annual premium stacks up across different benchmarks:

| Benchmark | Premium |

|---|---|

| This Quote | $4,108/yr |

| Fennell Bay suburb average | $5,382/yr |

| Fennell Bay suburb median | $6,170/yr |

| Fennell Bay 25th percentile | $3,251/yr |

| Fennell Bay 75th percentile | $7,138/yr |

| Lake Macquarie LGA average | $11,064/yr |

| NSW state average | $9,528/yr |

| NSW state median | $3,770/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

A few things stand out here. First, this quote sits below the Fennell Bay suburb average and median, which is a positive sign — it means the homeowner is paying less than most others in the same postcode who've sought quotes through our platform.

Second, the Lake Macquarie LGA average of $11,064 is strikingly high, which suggests there are pockets within the broader local government area that attract significantly elevated premiums — likely due to flood, bushfire, or other localised risks. Fennell Bay's own suburb figures are considerably lower, which is worth noting.

Third, while the NSW state average of $9,528 looks alarming, the state median of $3,770 tells a more nuanced story. Averages can be skewed upward by high-risk or high-value properties; the median gives a better sense of what a typical NSW homeowner pays. At $4,108, this quote sits just above the state median — which is consistent with the "fair" rating.

You can explore more local data on the Fennell Bay suburb stats page, compare it against NSW state-wide insurance trends, or take a look at national home insurance benchmarks.

Note: Suburb comparisons are based on a sample of 8 quotes, so results should be interpreted as indicative rather than definitive.

---

Property Features That Affect Your Premium

Insurance underwriters assess risk based on a wide range of property characteristics. For this particular home, several features are likely influencing the premium — both upward and downward.

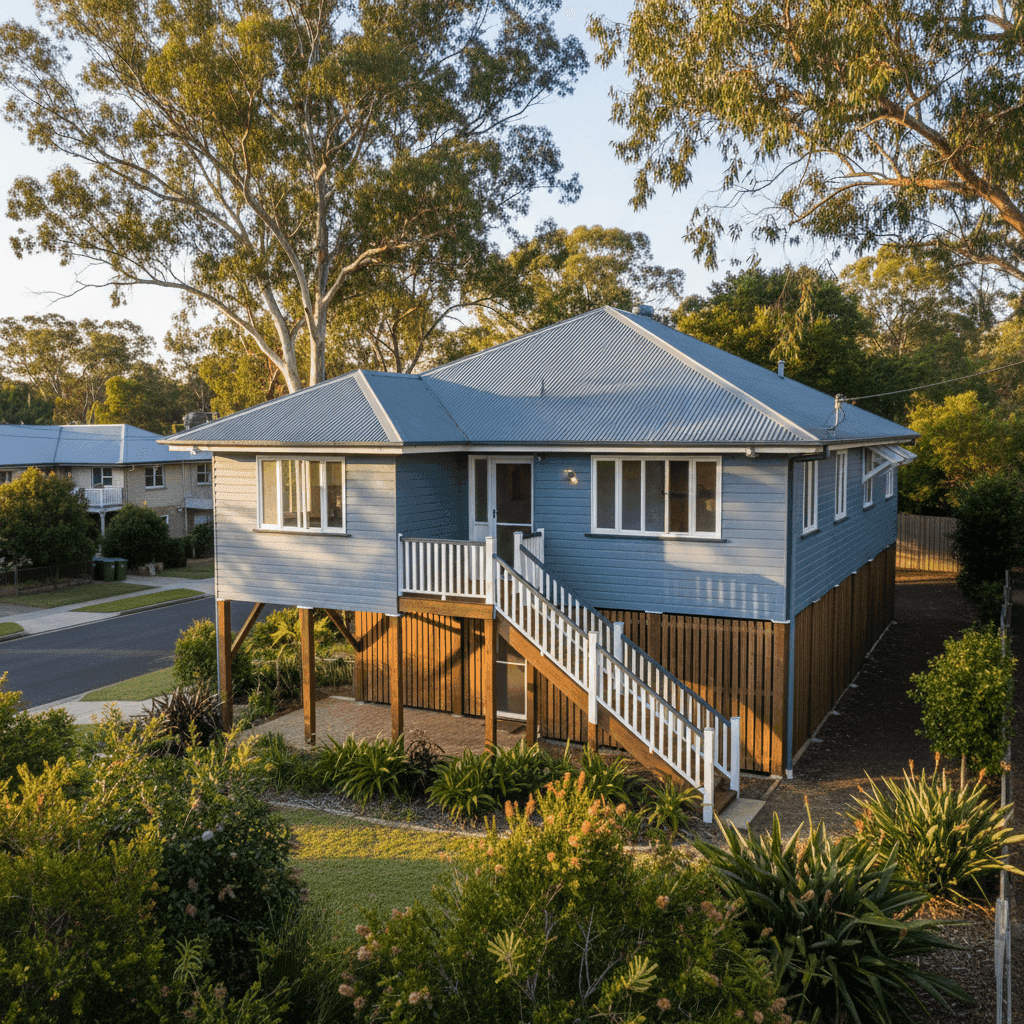

Weatherboard Timber Walls

Weatherboard construction is common in older Australian homes and carries a higher fire risk than brick or rendered masonry. Timber can also be more susceptible to moisture ingress and pest damage over time. Insurers typically apply a loading to weatherboard homes, which will be a contributing factor to the premium here.

Age of the Property (Built 1965)

At over 60 years old, this home predates many modern building standards. Older properties can have ageing electrical wiring, plumbing, and structural elements that increase the likelihood of a claim. This is a standard risk factor that most insurers price into their calculations.

Elevated on Stumps

Being elevated by at least one metre on stumps is actually a double-edged sword from an insurance perspective. On one hand, elevation can reduce flood risk by keeping the floor level above potential inundation — a meaningful advantage given Fennell Bay's proximity to Lake Macquarie. On the other hand, the subfloor space introduces its own risks (pest access, structural movement), and elevated homes can be more vulnerable to wind uplift.

Steel/Colorbond Roof

Colorbond roofing is generally viewed favourably by insurers. It's durable, fire-resistant, and low-maintenance compared to older materials like terracotta tiles or fibrous cement sheeting. This is likely a mild positive factor in the pricing.

Ducted Climate Control

The presence of ducted air conditioning adds to the replacement cost of the home and may slightly increase the premium, but it's a relatively minor factor compared to the structural characteristics above.

Timber and Laminate Flooring

Like the walls, timber flooring adds to fire risk and replacement cost. Laminate flooring is generally less expensive to replace but can be damaged by water — relevant given the lakeside location.

---

Tips for Homeowners in Fennell Bay

Whether you're renewing your policy or shopping around for the first time, here are some practical steps to help you get the best value on your home insurance.

1. Review your sum insured carefully A building sum insured of $650,000 for a 153 sqm home works out to roughly $4,250 per square metre — which is within a reasonable range for a weatherboard home with standard fittings, but worth validating against a professional building replacement cost estimate. Being underinsured can leave you significantly out of pocket after a major claim.

2. Consider your excess settings Both the building and contents excesses on this policy are set at $1,000. Opting for a higher excess (say, $2,000 or $2,500) can meaningfully reduce your annual premium. If you have an emergency fund to cover a larger out-of-pocket cost in the event of a claim, this can be a smart trade-off.

3. Don't auto-renew without comparing Insurers often increase premiums at renewal with little fanfare. Given that this quote already sits below the suburb average, it's worth checking whether other providers can beat it — especially as your property ages and your circumstances change. Even a 10–15% saving on a $4,108 premium represents $400–$600 back in your pocket.

4. Document your contents thoroughly With $140,000 in contents cover, it's worth maintaining an up-to-date home inventory — photos, receipts, and serial numbers for high-value items. This makes the claims process significantly smoother and helps ensure you're not over- or under-insured on the contents side.

---

Ready to Compare?

Whether this quote is your current policy or one you've just received, it's always worth seeing what else is available. CoverClub makes it easy to compare home and contents insurance options tailored to your property. Get a quote today and find out if you could be paying less — without sacrificing the cover you need.