Fern Bay is a relaxed coastal suburb sitting on the shores of Port Stephens in the Hunter Region of New South Wales. Known for its quiet streets, golf course, and easy access to the beach, it's an increasingly popular spot for owner-occupiers and retirees alike. This article breaks down a real home insurance quote for a two-bedroom free standing home in Fern Bay — and what it tells us about the cost of insuring property in this part of NSW.

---

Is This Quote Fair?

The quote in question covers both building and contents for a $1,222 annual premium (or $121 per month). The building is insured for $400,000 and contents for $35,000, with a $3,000 building excess and $1,000 contents excess.

Our pricing analysis rates this quote as CHEAP — below average — and the numbers back that up convincingly. When compared against other quotes collected for properties in Fern Bay, this premium sits well beneath the suburb average of $3,514 per year and the suburb median of $3,415 per year. In fact, it's less than a third of what most Fern Bay homeowners are paying for comparable cover.

So what's driving such a competitive price? A combination of factors is likely at play: the modest size of the home (130 sqm), the relatively low contents value, and the property's characteristics all contribute to a lower risk profile in the eyes of insurers. The $3,000 building excess is on the higher side, which also reduces the premium — essentially, the homeowner is self-insuring a greater portion of smaller claims in exchange for lower ongoing costs.

It's worth noting that a lower premium isn't always better if it comes with coverage gaps, so it's important to review the Product Disclosure Statement carefully and ensure the policy actually meets your needs.

---

How Fern Bay Compares

To put this quote in proper context, here's how Fern Bay stacks up against broader benchmarks:

| Benchmark | Premium |

|---|---|

| This Quote | $1,222/yr |

| Fern Bay Suburb Average | $3,514/yr |

| Fern Bay Suburb Median | $3,415/yr |

| Fern Bay 25th Percentile | $3,162/yr |

| Port Stephens LGA Average | $3,116/yr |

| NSW State Median | $3,770/yr |

| National Median | $2,764/yr |

| NSW State Average | $9,528/yr |

| National Average | $5,347/yr |

Based on 27 quotes collected for the Fern Bay 2295 area.

A few things stand out here. First, the Fern Bay suburb average of $3,514 is notably lower than the NSW state average of $9,528 — though that state figure is heavily skewed by high-risk areas and premium outliers across NSW. The state median of $3,770 is a more representative comparison point, and Fern Bay sits comfortably below it.

Against national benchmarks, the suburb also performs well. The national median of $2,764 is actually lower than Fern Bay's median, suggesting that while Fern Bay isn't the cheapest market in Australia, it's far from the most expensive. Coastal proximity and the age of local housing stock likely push premiums slightly above the national median for the area.

The quote analysed here, at $1,222, sits dramatically below every single benchmark — suburb, state, and national. This is genuinely cheap cover for this type of property.

---

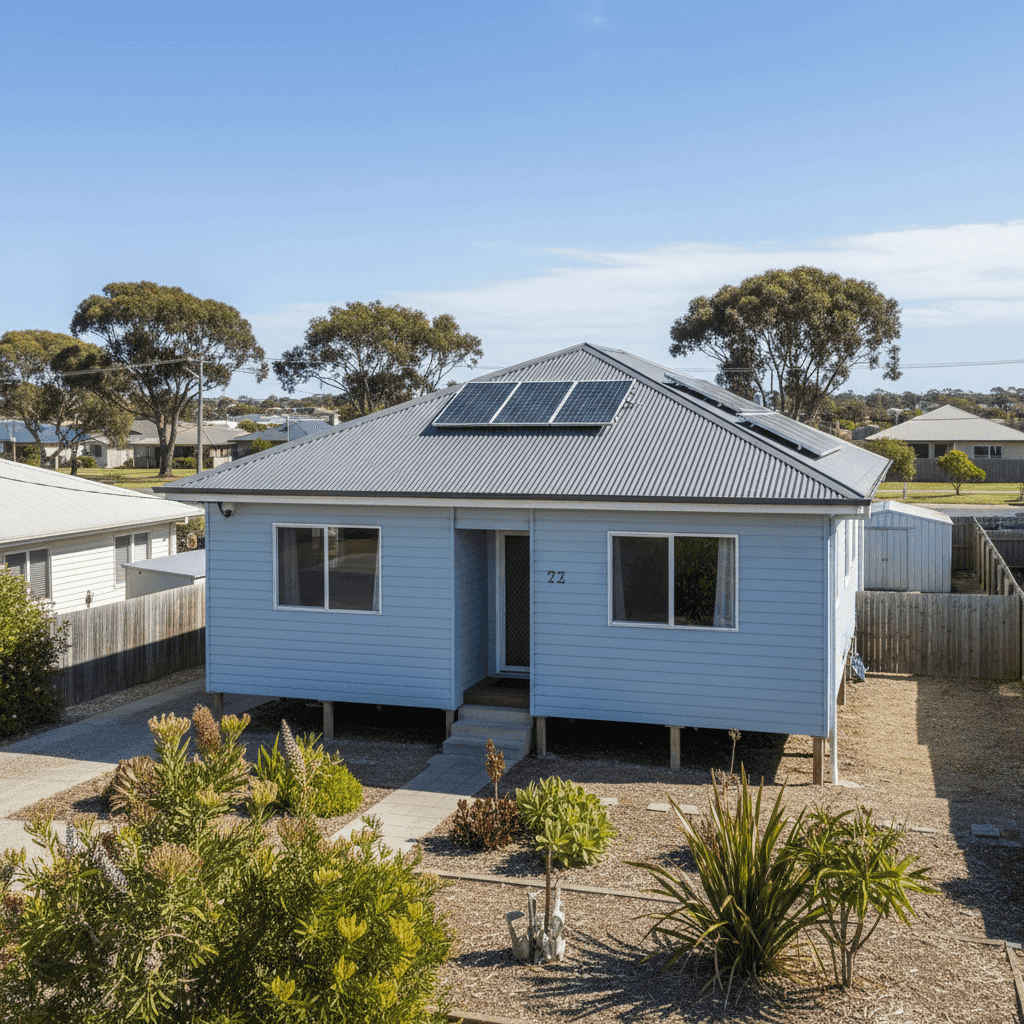

Property Features That Affect Your Premium

Several characteristics of this property are worth examining from an insurance perspective:

Weatherboard timber construction (1965 build) Older weatherboard homes are generally considered higher risk by insurers than modern brick or clad constructions. Timber is more susceptible to fire, and ageing materials can increase the likelihood of structural claims. A 1965 build is now over 60 years old, which may prompt some insurers to apply loadings — making the low premium here even more notable.

Steel/Colorbond roof This is actually a positive from an insurer's perspective. Colorbond roofing is durable, resistant to corrosion, and performs well in storms. It's a common and well-regarded roofing material across coastal NSW, and insurers typically view it favourably compared to older tile or asbestos-cement roofing.

Stump foundation Homes built on stumps (also known as pier or post foundations) can be more vulnerable to movement and underfloor damage, particularly in areas with moisture or termite activity. This is a factor some insurers may price for, especially in coastal or semi-rural environments like Fern Bay.

Solar panels The presence of solar panels adds replacement value to the property. Most insurers will cover rooftop solar as part of the building sum insured, but it's worth confirming this is explicitly included in your policy — and that the $400,000 building sum insured adequately accounts for them.

No pool, no ducted climate control The absence of a pool removes a common liability and maintenance risk. Ducted systems can be expensive to replace and are sometimes a source of claims, so their absence also simplifies the risk profile.

Vinyl flooring Vinyl is relatively inexpensive to replace compared to hardwood or tiles, which may contribute to the lower contents and building replacement estimates.

---

Tips for Homeowners in Fern Bay

1. Review your building sum insured regularly Construction costs have risen significantly in recent years across NSW. A $400,000 sum insured may be appropriate today, but it's worth getting a building replacement cost estimate every year or two — especially for older homes where materials and labour costs can be harder to predict. Underinsurance is one of the most common issues Australian homeowners face at claim time.

2. Confirm solar panels are covered If your policy covers the building, solar panels should generally be included — but not all policies treat them the same way. Check whether your insurer covers panels for accidental damage, storm damage, and electrical failure, and whether there's a sub-limit that applies.

3. Consider your excess carefully The $3,000 building excess on this policy is relatively high. While it helps keep premiums low, it means you'd be out of pocket for the first $3,000 of any building claim. If you have the financial buffer to absorb that, it's a sensible trade-off. If not, it may be worth comparing policies with a lower excess — even if the annual premium is slightly higher.

4. Get multiple quotes before renewing The fact that this quote came in at $1,222 against a suburb average of $3,514 demonstrates just how much variation exists between insurers for the same property. Don't assume your renewal price is competitive — shopping around at CoverClub can surface significant savings without sacrificing cover quality.

---

Compare Your Own Quote

Whether you're insuring a weatherboard cottage or a modern build, the best way to know if you're getting a fair deal is to compare. At CoverClub, you can enter your property details and see how your premium stacks up against real quotes from across your suburb, your state, and nationally. It takes just a few minutes and could save you hundreds of dollars a year.

Browse Fern Bay insurance data, explore NSW-wide trends, or check out national home insurance benchmarks to get a clearer picture of what you should be paying.