If you own a free standing home in Ferny Hills, QLD 4055, you've probably wondered whether you're paying a fair price for home and contents insurance — or quietly overpaying year after year. This article breaks down a real insurance quote for a three-bedroom, weatherboard home in the suburb, benchmarking it against local, state, and national data so you can make a genuinely informed decision.

---

Is This Quote Fair?

The quote in question comes in at $1,865 per year (or $179/month) for combined home and contents cover, with a building sum insured of $450,000 and contents valued at $150,000. Both the building and contents excess are set at $1,000.

Our price rating for this quote is FAIR — Around Average, and the data backs that up. Based on 22 quotes collected for Ferny Hills (postcode 4055), the suburb average sits at $2,122/yr and the median at $1,967/yr. At $1,865, this quote lands just below the suburb median — meaning roughly half of comparable properties in the area are paying more.

It's not a bargain-basement price, but it's also not cause for alarm. The suburb's 25th percentile is $1,444/yr, so there is room to potentially find a cheaper policy if you shop around. Equally, the 75th percentile reaches $2,745/yr, which shows just how wide the spread can be depending on insurer, coverage details, and individual risk factors.

---

How Ferny Hills Compares

Zoom out a little and the picture becomes even more reassuring. Here's how this quote sits against broader benchmarks:

| Benchmark | Premium |

|---|---|

| This Quote | $1,865/yr |

| Ferny Hills Suburb Average | $2,122/yr |

| Ferny Hills Suburb Median | $1,967/yr |

| Moreton Bay LGA Average | $3,435/yr |

| QLD State Average | $9,129/yr |

| QLD State Median | $3,903/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

The contrast with Queensland's state average is striking. At $9,129/yr for QLD, the state figure is heavily skewed by high-risk coastal and cyclone-prone regions — think Far North Queensland, where premiums can be eye-watering. Ferny Hills, sitting in Brisbane's north-western suburbs, is not a cyclone risk area, which goes a long way to explaining why local premiums are so much more moderate.

Even against the national average of $5,347/yr, this quote looks competitive. The national median of $2,764/yr is a more useful comparison point, and at $1,865, this quote sits comfortably below it. Homeowners in Ferny Hills are, broadly speaking, in a relatively favourable insurance environment compared to much of the country.

---

Property Features That Affect Your Premium

Every insurer prices risk differently, but several characteristics of this property are worth understanding in the context of your premium.

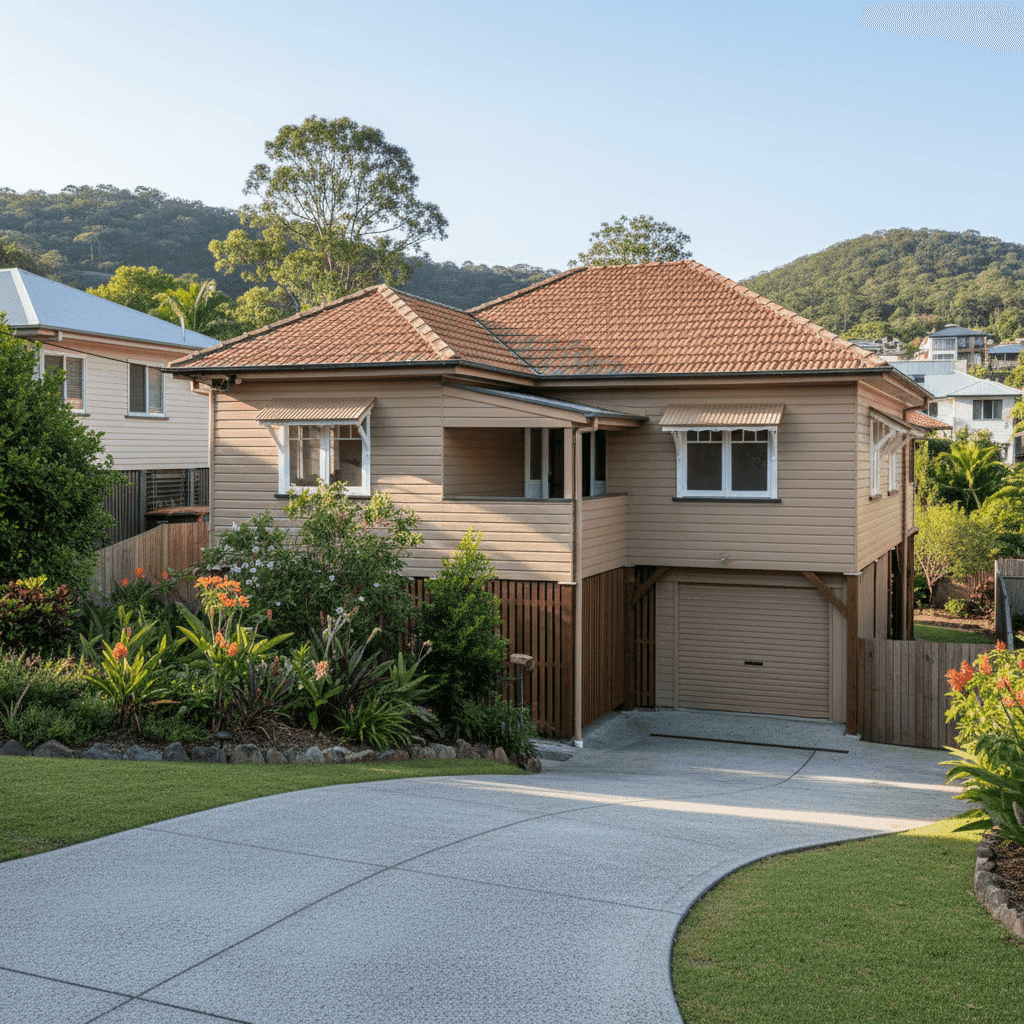

Weatherboard Timber Walls

Weatherboard construction is common in older Queensland homes and carries a higher fire risk than brick or rendered masonry. Timber can also be more susceptible to moisture damage and rot over time. Insurers typically factor this in, which can push premiums slightly higher compared to brick veneer or full brick properties.

Tiled Roof

A tiled roof is generally viewed favourably by insurers. Tiles are durable, fire-resistant, and have a long lifespan — all positives when it comes to risk assessment. This likely helps offset some of the additional risk associated with the timber frame construction.

Stump Foundation

Built in 1967, this home sits on stumps — a hallmark of traditional Queensland architecture. While stumps allow for excellent airflow beneath the home (a real asset in subtropical Brisbane), they can be a source of concern for insurers if not well-maintained. Older stumps may be subject to termite damage or subsidence, so keeping them in good condition is important both for safety and insurability.

Timber and Laminate Flooring

Timber and laminate floors are attractive but can be costly to repair or replace after water damage or flooding. This is worth keeping in mind when reviewing your contents and building cover limits.

Construction Year: 1967

Older homes often attract slightly higher premiums due to ageing infrastructure — wiring, plumbing, and structural elements may not meet current building codes. That said, many insurers are well-acquainted with this era of Queensland home and price accordingly.

Building Size: 130 sqm

At 130 sqm, this is a modest-sized home. A $450,000 building sum insured equates to a rebuild cost of approximately $3,460/sqm — broadly in line with current construction costs in South East Queensland when factoring in demolition, site preparation, and professional fees.

---

Tips for Homeowners in Ferny Hills

1. Review Your Sum Insured Annually

Construction costs have risen sharply over recent years. Make sure your $450,000 building sum insured still reflects what it would actually cost to rebuild your home from scratch — not just its market value. Underinsurance is one of the most common and costly mistakes homeowners make.

2. Shop Around at Renewal Time

Your insurer is unlikely to offer you their best rate automatically at renewal. Use a comparison tool like CoverClub to benchmark your renewal quote against the market before you accept it. Even a saving of $200–$300 per year adds up significantly over time.

3. Consider Your Excess Level

This policy carries a $1,000 excess on both building and contents. Opting for a higher excess (say, $2,000) can reduce your annual premium — a worthwhile trade-off if you have the financial buffer to cover a larger out-of-pocket cost in the event of a claim.

4. Maintain Your Stumps and Subfloor

Given the stump foundation, it's worth scheduling regular inspections for termite activity and stump condition. Some insurers may exclude or limit cover for damage that results from poor maintenance, so staying on top of this protects both your home and your claim eligibility.

---

Compare Your Options with CoverClub

Whether you're renewing soon or just curious about where your current premium sits, CoverClub makes it easy to see how your quote stacks up. Our data covers thousands of properties across Australia, giving you real benchmarks — not guesswork. Get a quote today and find out if you could be paying less for the same level of cover.