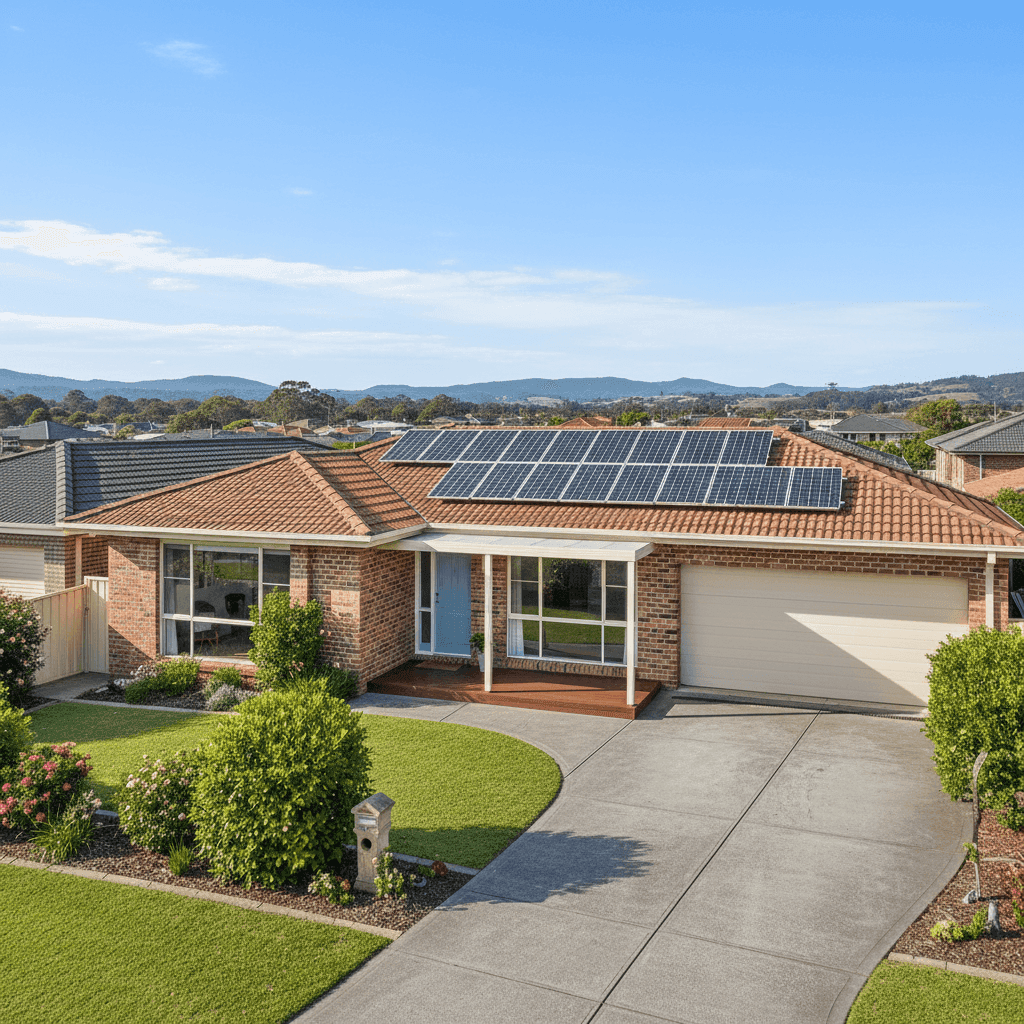

If you own a free standing home in Flinders, NSW 2529, you're likely already aware that the Illawarra coast is a beautiful — but weather-exposed — place to live. Getting the right home and contents insurance at a fair price is essential, especially when rebuild costs and contents values keep climbing. This article breaks down a real home insurance quote for a four-bedroom, two-bathroom brick veneer home in Flinders, comparing it against suburb, state, and national benchmarks so you can understand exactly where you stand.

---

Is This Quote Fair?

The quote in question comes in at $2,079 per year (or $199/month) for combined home and contents cover, with a building sum insured of $531,000 and contents cover of $41,000. Both the building and contents excess sit at $1,000 — a fairly standard arrangement.

Our price rating for this quote is FAIR — Around Average, and the data backs that up. Within the Flinders suburb (postcode 2529), the average annual premium across 31 quotes is $2,234, meaning this quote sits roughly $155 below the local average — a modest but meaningful saving. It also falls between the suburb's 25th percentile ($1,596/yr) and 75th percentile ($2,887/yr), placing it comfortably in the middle of the market.

In short: this isn't a bargain-basement price, but it's not an overpriced outlier either. For a well-appointed 235 sqm home with solar panels and ducted climate control, landing near the suburb average is a reasonable outcome.

---

How Flinders Compares to the Rest of NSW and Australia

One of the most striking takeaways from this data is just how dramatically home insurance costs vary across New South Wales — and the country as a whole.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Flinders (2529) | $2,234/yr | $1,956/yr |

| Shellharbour LGA | $1,744/yr | — |

| NSW State | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

The NSW state average of $9,528 looks alarming at first glance, but this figure is heavily skewed by high-risk postcodes — think flood-prone inland towns, cyclone-affected coastal areas in Far North Queensland (which pulls the national figure up too), and bushfire-prone regions. The median is a far more representative number, and at $3,770 for NSW, Flinders still comes in well below it.

Compared to the national median of $2,764, this Flinders quote of $2,079 is actually sitting below the midpoint — a positive sign for homeowners in the area. The Shellharbour LGA average of $1,744 is notably lower, which may reflect a mix of property types and ages across the broader local government area pulling that figure down.

You can explore more localised data on the Flinders suburb stats page, dive into NSW-wide insurance trends, or check out national home insurance benchmarks to put your own situation in context.

---

Property Features That Affect Your Premium

Insurers don't price every home the same way — they assess risk based on a combination of location, construction, and features. Here's how the characteristics of this particular property are likely influencing the premium:

Brick veneer construction is generally viewed favourably by insurers. It's more fire-resistant than timber-framed weatherboard homes and holds up well in storms. Compared to full-brick or double-brick, it's lighter and more common in post-2000 builds — and this home, constructed in 2006, fits squarely in that modern era.

Tiled roof is another tick in the right column. Tile roofs are durable, non-combustible, and less prone to wind damage than corrugated iron in moderate-wind zones. Combined with a concrete slab foundation, the structural profile of this home is solid.

Solar panels are increasingly common but do add a layer of complexity to home insurance. Panels are typically covered under the building policy (since they're fixed to the structure), and at $531,000 sum insured, there should be adequate cover — but it's worth confirming with your insurer that your solar system is explicitly included, particularly for damage from hail or storm.

Ducted climate control adds to the replacement value of the home. These systems can cost $10,000–$20,000 or more to replace, and they're a common source of underinsurance if homeowners forget to factor them into their building sum insured.

Tile flooring throughout is a low-maintenance, durable choice that generally doesn't add significant risk from an insurer's perspective, though it does contribute to the overall rebuild cost per square metre.

At 235 sqm, this is a generously sized home. Rebuild costs in coastal NSW have risen sharply in recent years due to labour shortages and material price increases — making it especially important to review your sum insured regularly.

---

Tips for Homeowners in Flinders

Whether you're reviewing an existing policy or shopping around for the first time, here are four practical steps to make sure you're getting the best value:

- Review your building sum insured annually. Construction costs in the Illawarra region have increased significantly post-pandemic. A sum insured that was adequate two years ago may leave you underinsured today. Use a reputable building cost calculator or speak with a local builder to get a realistic estimate.

- Confirm your solar panels are covered. Ask your insurer directly whether your solar system — including panels, inverter, and mounting hardware — is covered under the building section of your policy. Some policies exclude storm or hail damage to panels, or cap payouts separately.

- Consider your excess carefully. Both the building and contents excess on this quote are set at $1,000. Opting for a higher excess (say, $2,000) can meaningfully reduce your annual premium — but make sure you can comfortably afford to pay it in the event of a claim.

- Shop around at renewal time. Insurers don't always reward loyalty — in fact, many offer their best rates to new customers. Even if your current premium feels reasonable, running a comparison at renewal can reveal significant savings without any reduction in cover quality.

---

Compare Your Home Insurance with CoverClub

Whether the quote above looks like a good deal or prompts you to explore your options, CoverClub makes it easy to benchmark your premium against real data from your suburb. Get a quote today and see how your home insurance stacks up — you might be paying more than you need to, or you might get the peace of mind of knowing you're already well covered.