If you own a four-bedroom free standing home in Flinders View, QLD 4305, you're probably curious about whether you're paying a fair price for home and contents insurance — or leaving money on the table. Flinders View is a well-established outer suburb of Ipswich, characterised by family homes on generous blocks, and its insurance landscape reflects a mix of factors that are worth understanding before you renew or switch policies.

This article breaks down a recent home and contents insurance quote for a property in this suburb, compares it against local, state, and national benchmarks, and offers practical tips to help you get better value on your cover.

---

Is This Quote Fair?

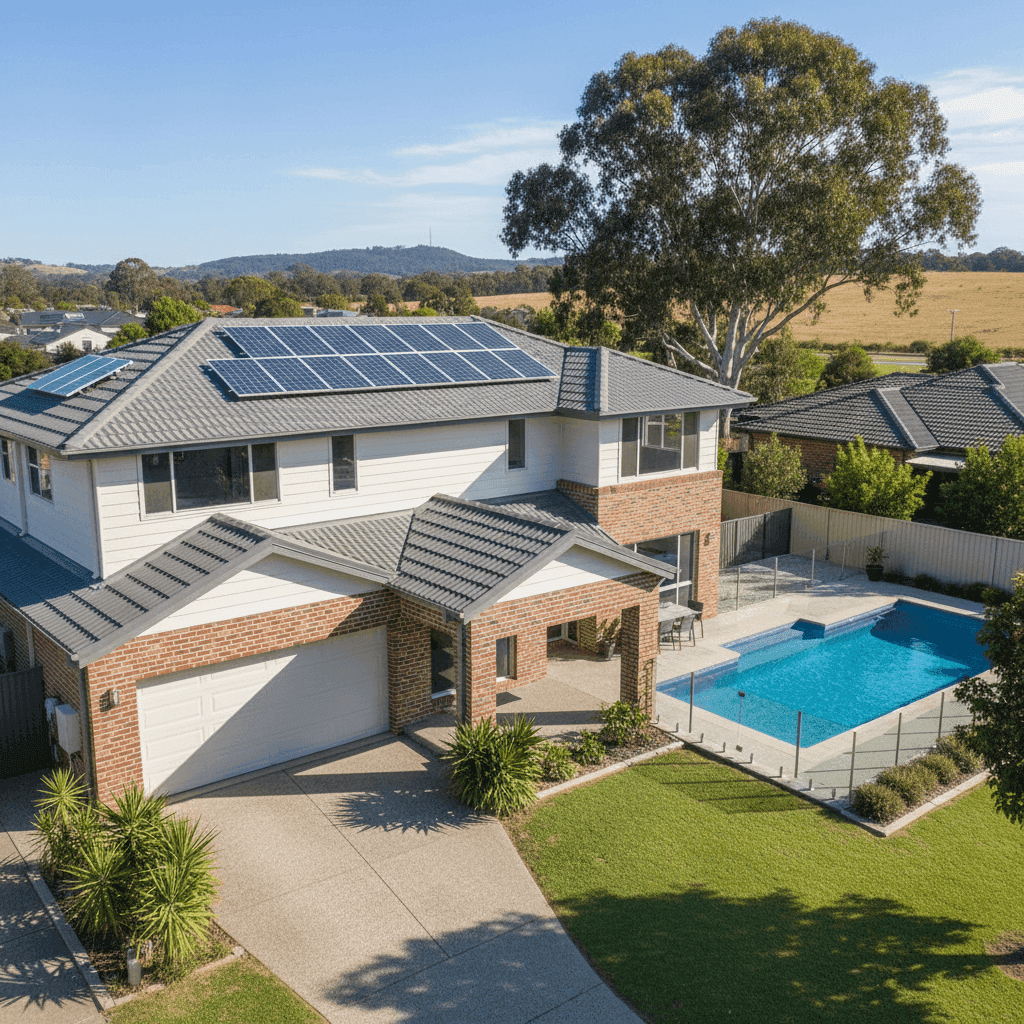

The quote in question comes in at $2,052 per year (or $201/month) for a combined home and contents policy, with a building sum insured of $700,000, contents cover of $50,000, and a $1,000 excess on both building and contents.

Our price rating for this quote is FAIR — Around Average, and the numbers back that up. Based on 37 quotes collected for Flinders View (4305), the suburb average sits at $2,114/year and the median at $2,268/year. This quote lands just below both of those figures, meaning the homeowner is paying slightly less than what most comparable properties in the area are quoted.

To put it in percentile terms: the suburb's 25th percentile is $1,303/year and the 75th percentile is $2,567/year. At $2,052, this quote sits comfortably in the middle range — not the cheapest available, but well within what you'd consider reasonable for a property of this size and specification.

It's worth noting that "fair" doesn't necessarily mean "the best deal possible." There may still be room to reduce your premium by adjusting your cover, comparing more insurers, or reviewing your sum insured.

---

How Flinders View Compares

One of the most striking things about this quote is how favourably Flinders View compares to broader Queensland insurance benchmarks.

| Benchmark | Average Premium |

|---|---|

| Flinders View (suburb) | $2,114/yr |

| Queensland (state) | $9,129/yr |

| National | $5,347/yr |

The Queensland state average of $9,129/year is extraordinarily high compared to the suburb figure — a difference largely driven by cyclone-prone coastal and far-north Queensland regions, where insurance premiums have surged dramatically in recent years. Flinders View, sitting inland near Ipswich, is not in a cyclone risk zone, which is a significant factor keeping local premiums far more manageable.

Even against the national average of $5,347/year and the national median of $2,764/year, this Flinders View quote looks competitive. The suburb average of $2,114 is well below the national median, suggesting homeowners in this area generally enjoy more affordable premiums than many Australians elsewhere.

For additional context, the LGA average for Scenic Rim sits at $8,744/year — again, heavily influenced by higher-risk rural and semi-rural properties in that broader local government area. Flinders View's suburban character and lower risk profile help it stand apart from that figure.

---

Property Features That Affect Your Premium

Insurance pricing isn't arbitrary — it's driven by specific characteristics of your property and location. Here's how the features of this particular home influence its premium:

Brick Veneer Walls Brick veneer is one of the more favourable external wall types from an insurer's perspective. It offers solid fire resistance and structural durability compared to timber or cladding, which can translate to lower building premiums.

Tiled Roof Terracotta or concrete tiles are considered a resilient roofing material. They hold up well in storms and hail events (common in southeast Queensland), though they can be more expensive to repair or replace than Colorbond. Overall, tiles are viewed positively by insurers.

Concrete Slab Foundation A slab foundation is standard for homes built in this era and region, and it's generally considered low-risk for subsidence or movement compared to older pier-and-beam or strip footing styles.

Built in 2005 At roughly 20 years old, this home is in a favourable age bracket for insurance. It's modern enough to comply with updated building codes but not so new that replacement costs are at a premium. Homes built post-2000 often benefit from improved construction standards, particularly around cyclone and flood resilience.

Swimming Pool A pool adds a modest amount to your premium due to the liability and structural risks associated with it — but it's a very common feature in Queensland homes and insurers price it routinely.

Solar Panels Solar panels are now factored into most home insurance policies, either as part of the building sum insured or as a separate item. It's worth confirming with your insurer that your panels are adequately covered under your current policy, particularly for damage from storms or hail.

Standard Fittings With standard-quality fittings throughout, this home avoids the premium uplift that comes with high-end or bespoke finishes. Homes with premium kitchens, imported tiles, or custom joinery typically cost more to rebuild and therefore attract higher premiums.

214 sqm Building Size At 214 square metres, this is a mid-to-large family home. The $700,000 building sum insured works out to roughly $3,271 per square metre — broadly in line with current Queensland construction costs, though it's always worth getting a professional rebuild cost assessment to ensure you're not under- or over-insured.

---

Tips for Homeowners in Flinders View

1. Check Your Building Sum Insured Annually Construction costs in southeast Queensland have risen significantly since 2020. If your sum insured hasn't been reviewed recently, you may be underinsured — meaning a total loss payout might not cover a full rebuild. Use an independent building cost calculator or speak to a quantity surveyor to validate your figure.

2. Confirm Solar Panel Coverage Solar systems can be worth $8,000–$20,000 or more. Ask your insurer specifically whether your panels are included in the building sum insured and what events are covered. Some policies exclude storm damage to panels unless you explicitly add it.

3. Compare at Renewal Time Loyalty doesn't always pay in insurance. Insurers frequently offer better rates to new customers than existing ones. Even if your current premium feels reasonable, running a comparison at renewal — particularly through a platform like CoverClub — can surface meaningfully cheaper options for the same level of cover.

4. Review Your Contents Estimate A $50,000 contents value is on the conservative side for a four-bedroom home. Take a room-by-room inventory to ensure your furniture, appliances, clothing, electronics, and valuables are adequately covered. Being underinsured on contents is one of the most common (and costly) mistakes homeowners make.

---

Ready to Compare?

Whether you're renewing soon or just benchmarking your current policy, it pays to see what else is available. CoverClub makes it easy to compare home and contents insurance quotes for properties across Queensland and Australia. Get a quote today and find out whether your premium is truly competitive — or whether there's a better deal waiting for you.