If you own a free standing home in Flowerdale, VIC 3717, you're likely well aware that finding competitive home and contents insurance in this part of Victoria takes a little research. Nestled in the Yea River valley north of Melbourne, Flowerdale sits in a semi-rural landscape that comes with its own unique set of insurance considerations — from bushfire exposure to the sheer cost of rebuilding in a regional setting. This article breaks down a real home insurance quote for a 2-bedroom free standing home in Flowerdale, puts the price in context, and offers practical tips to help you get the best value cover.

---

Is This Quote Fair?

The quote in question comes in at $1,957 per year (or $195/month) for combined home and contents insurance, covering a building sum insured of $819,000 and contents valued at $50,000. The building excess is $3,000 and the contents excess is $1,000.

Our pricing engine rates this quote as CHEAP — below average for the area. That's a strong result, and it's worth understanding just how significant the saving is.

Suburb-level data for Flowerdale shows an average annual premium of $14,493 and a median of $13,816. Even the cheapest quarter of quotes in the suburb (the 25th percentile) sits at $12,347/year. This quote, at $1,957, is dramatically below all of those benchmarks — coming in at roughly one-seventh of the suburb average. That's an extraordinary gap and suggests this particular insurer is pricing the risk of this property very favourably compared to others operating in the postcode.

For homeowners in Flowerdale who haven't reviewed their policy recently, this kind of comparison is a wake-up call. Paying close to $14,000 a year when comparable cover may be available for a fraction of that price is a costly oversight.

---

How Flowerdale Compares

To fully appreciate this quote, it helps to zoom out and look at the broader picture.

| Benchmark | Annual Premium |

|---|---|

| This Quote | $1,957 |

| Flowerdale Suburb Average | $14,493 |

| Flowerdale Suburb Median | $13,816 |

| Mitchell LGA Average | $2,743 |

| VIC State Average | $3,000 |

| VIC State Median | $2,718 |

| National Average | $5,347 |

| National Median | $2,764 |

A few things stand out here. First, Flowerdale's suburb average of $14,493 is nearly five times the Victorian state average of $3,000 — a clear reflection of the elevated bushfire risk in this region. It's also well above the national average of $5,347, underscoring just how exposed this postcode is considered to be by many insurers.

The Victorian state average of $3,000/year is itself a useful anchor. This quote sits comfortably below that figure, which is a meaningful achievement for a property in a high-risk bushfire zone. The Mitchell LGA average of $2,743 provides another useful local reference point — and again, this quote beats it.

It's worth noting that the suburb sample size for Flowerdale is relatively small (8 quotes), so the suburb averages should be interpreted with some caution. That said, the pattern is consistent: insurance in this postcode tends to be expensive, making a below-average quote all the more valuable.

---

Property Features That Affect Your Premium

Several characteristics of this property are likely contributing to the competitive premium.

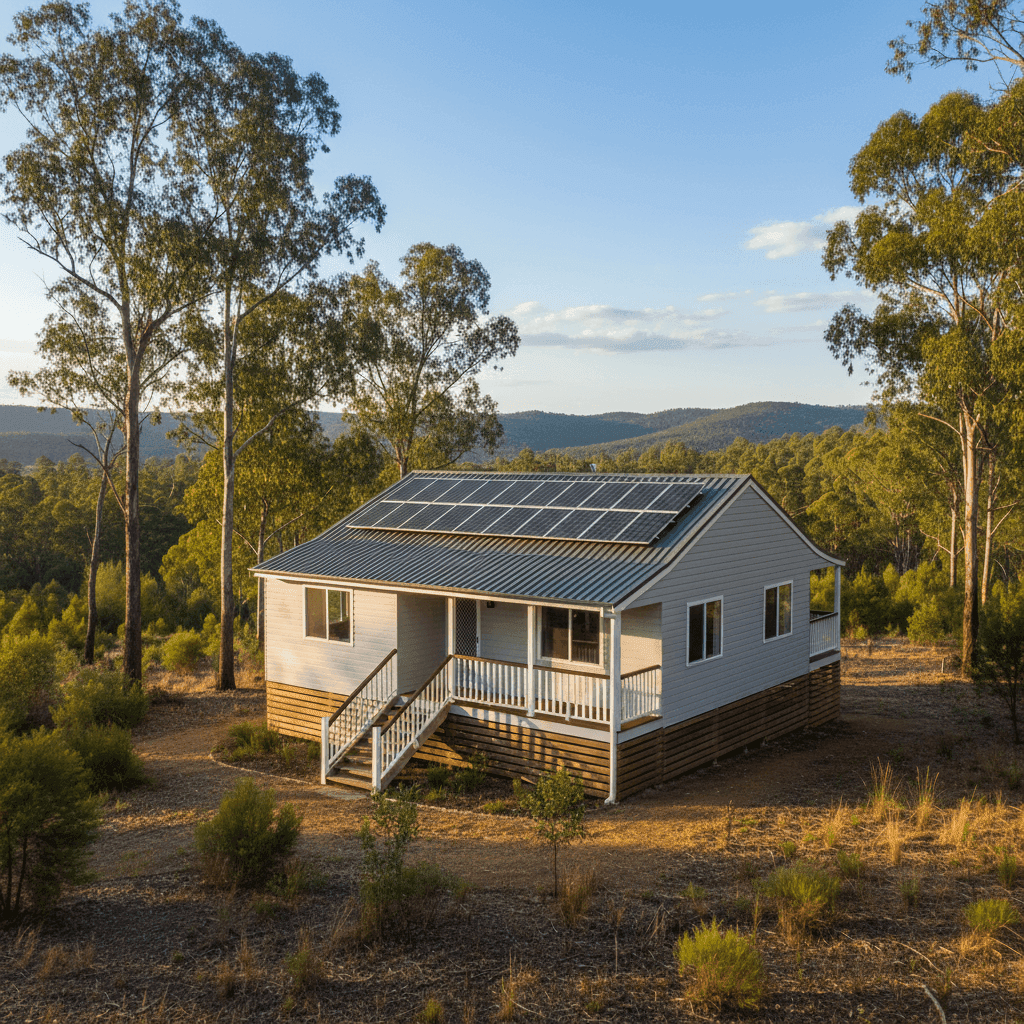

Construction materials: The home features Hardiplank/Hardiflex external walls and a steel/Colorbond roof. Both are considered fire-resistant and durable materials, which insurers typically view favourably — particularly in bushfire-prone areas like Flowerdale. Compared to timber weatherboard homes, fibre cement cladding like Hardieplank offers better resistance to ember attack and radiant heat, which can meaningfully reduce perceived risk.

Build year: Constructed in 2019, this is a relatively modern home. Newer builds are generally subject to current building codes, which include improved fire safety, structural integrity, and energy efficiency standards. This reduces the likelihood of claims related to aging infrastructure or substandard construction.

Foundation and elevation: The home sits on stumps and is elevated by less than 1 metre. A stumped foundation is common in regional Victoria and can be beneficial for airflow and some flood scenarios, though it may introduce additional considerations around subfloor maintenance. The modest elevation is unlikely to significantly affect the premium in either direction.

Solar panels: The property has solar panels, which are worth noting for insurance purposes. Solar panels add value to the home and should ideally be explicitly covered under the building sum insured. Confirm with your insurer that panels are included in your policy and that the $819,000 sum insured accounts for their replacement cost.

No pool, no ducted climate control: The absence of a pool and ducted air conditioning simplifies the risk profile slightly, removing two common sources of claims and maintenance issues.

Flooring: Tiled flooring throughout is practical and relatively low-risk from an insurance perspective, being resistant to water damage compared to carpet or timber.

---

Tips for Homeowners in Flowerdale

1. Don't set and forget your policy Given the wide spread of premiums in Flowerdale — from under $2,000 to over $15,000 — it's clear that insurers price this postcode very differently. Shopping around at renewal time can make an enormous difference. Use a comparison tool like CoverClub to benchmark your current policy against the market each year.

2. Review your sum insured carefully With a building sum insured of $819,000 for a 186 sqm home built in 2019, it's important to ensure this figure reflects the true cost of rebuilding — not the market value of the property. In regional Victoria, construction costs have risen sharply in recent years. Factor in site access costs, debris removal, and any premium associated with rebuilding in a bushfire-affected area.

3. Confirm your solar panels are covered Solar panels are a common exclusion or underinsured item in home policies. Check your product disclosure statement (PDS) to confirm they're included under your building cover, and that the sum insured is adequate to replace them alongside the rest of the structure.

4. Understand your bushfire preparedness obligations Many insurers in high-risk bushfire zones include conditions around property maintenance — such as keeping gutters clear, maintaining ember guards, and managing vegetation around the home. Failing to meet these conditions could affect a claim. Review your PDS and stay up to date with any Bushfire Attack Level (BAL) requirements relevant to your property.

---

Ready to Compare?

Whether you're renewing your policy or buying cover for the first time, it pays to know where your premium sits relative to the market. CoverClub makes it easy to compare home and contents insurance quotes for properties across Victoria and beyond. Get a quote today and see how much you could save — because in a suburb like Flowerdale, the difference between a good deal and an average one could be thousands of dollars a year.