Forest Lake is a well-established residential suburb in Brisbane's south-west, known for its leafy streets, family-friendly atmosphere, and the picturesque lake at its heart. It's also a suburb where home insurance premiums tend to sit at a more manageable level compared to many other parts of Queensland — something that will be welcome news for homeowners in the area.

This article takes a close look at a recent home and contents insurance quote for a four-bedroom, two-bathroom free-standing home in Forest Lake (postcode 4078). We'll unpack whether the quoted premium represents good value, how it stacks up against local and national benchmarks, and what steps you can take to make sure you're not paying more than you need to.

---

Is This Quote Fair?

The quoted annual premium for this property is $2,109 per year (or approximately $202 per month), covering both building and contents. Our analysis rates this as Fair — Around Average, which means it's broadly in line with what other Forest Lake homeowners are paying, without being a standout bargain or an obvious overpayment.

To put that in context:

- The suburb average for Forest Lake is $2,166/yr, and the median sits at $2,214/yr

- This quote comes in below both figures, which is a modest but meaningful saving

- It also sits comfortably within the middle band of the market — the 25th to 75th percentile range for the suburb spans $1,450/yr to $2,714/yr

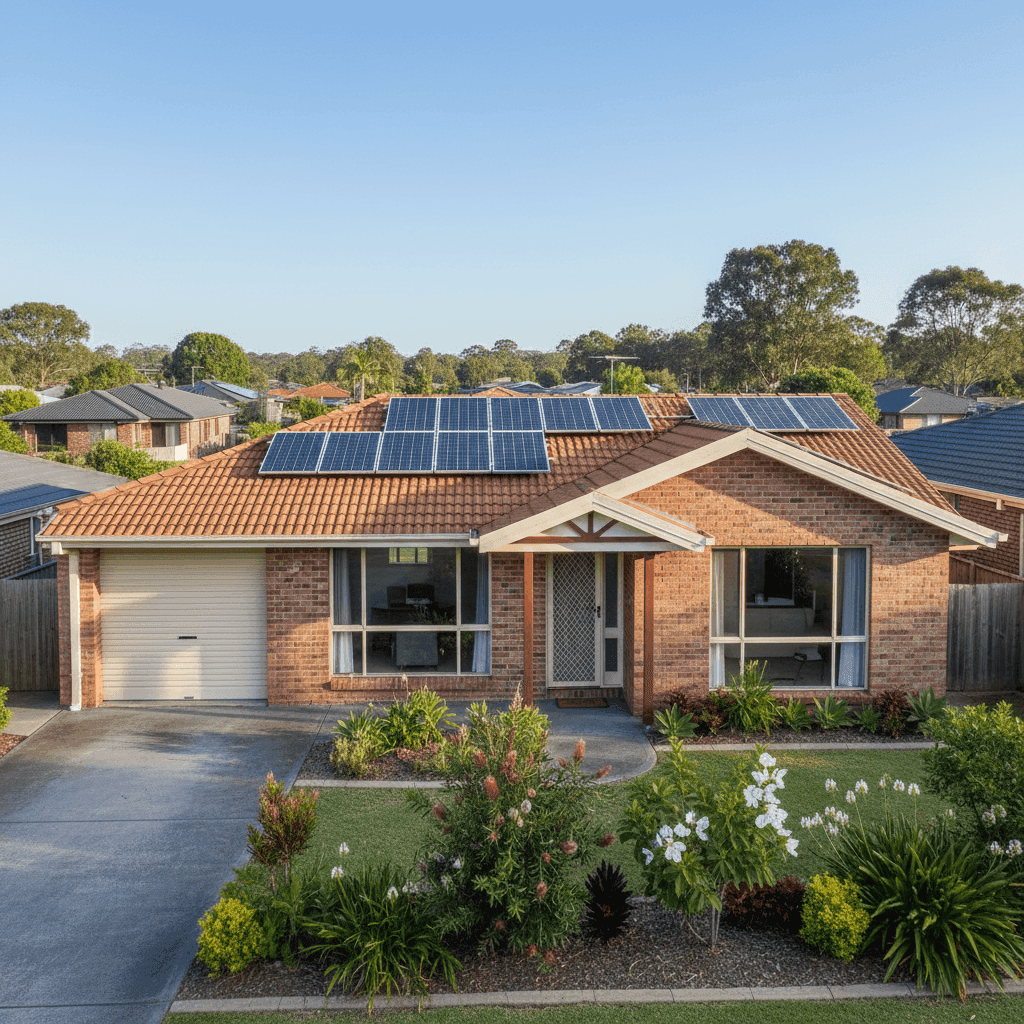

So while there's clearly room to find cheaper cover (the lower quartile suggests some homeowners are paying well under $1,500), this quote is far from the expensive end of the spectrum. For a property of this size and specification — 214 sqm, built in 1995, with solar panels and ducted climate control — landing close to the suburb median is a reasonable outcome.

The sum insured figures are also worth noting: $625,000 for the building and $239,000 for contents. These are substantial coverage amounts, and the premium relative to that level of protection is part of what makes this quote look reasonable on a value-per-dollar basis.

---

How Forest Lake Compares

One of the most striking things about this quote is how it compares to broader Queensland and national figures. You can explore the full data on our Forest Lake suburb stats page, but here's the headline picture:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Forest Lake (suburb) | $2,166/yr | $2,214/yr |

| Logan LGA | $4,617/yr | — |

| Queensland (state) | $9,129/yr | $3,903/yr |

| National | $5,347/yr | $2,764/yr |

The numbers tell a compelling story. Queensland's state average of $9,129/yr is dramatically higher than what Forest Lake homeowners typically pay — a difference driven largely by the high-risk cyclone and flood-prone regions in Far North Queensland and other parts of the state, which pull the average up significantly. You can see a full breakdown on our Queensland insurance stats page.

Even compared to the national average of $5,347/yr, Forest Lake sits in a very favourable position. The suburb's median of $2,214 is also well below the national median of $2,764, reinforcing that Forest Lake is a relatively affordable postcode for home insurance.

The Logan LGA average of $4,617/yr is notably higher than the Forest Lake suburb figures, suggesting that other parts of the Logan council area carry more risk — whether from flooding, storm damage, or other factors — than Forest Lake itself. This is a good reminder that insurance pricing is highly localised, and suburb-level data is far more meaningful than broad LGA or state averages when assessing your own quote.

---

Property Features That Affect Your Premium

Several characteristics of this property influence how insurers price the risk, for better or worse.

Brick veneer construction with a tiled roof is generally viewed favourably by insurers. Brick veneer offers solid fire resistance and structural durability, while tiles are considered a more resilient roofing material than corrugated iron or Colorbond in many contexts. Together, these features tend to attract lower premiums compared to timber-framed or clad homes.

Slab foundation is standard for homes built in Queensland during the 1990s and is generally unremarkable from an insurance perspective — neither a red flag nor a significant discount driver.

Solar panels are worth flagging. While they add value to a property, they also represent an additional asset that needs to be covered. Some policies include solar panels under the building sum insured automatically, while others treat them separately. It's worth confirming with your insurer exactly how your panels are covered and whether the $625,000 building sum insured accounts for their replacement cost.

Ducted climate control is another feature that adds to the rebuild cost and contents value of a home. Ducted systems can be expensive to replace, and ensuring your building and contents sums insured are sufficient to cover these is important.

Vinyl flooring throughout is a practical choice that's generally straightforward to replace, and won't significantly inflate your premium.

The property's 1995 construction year means it's now around 30 years old. Homes of this age can sometimes attract scrutiny around the condition of plumbing, electrical systems, and roofing — all of which can influence claims frequency. Keeping on top of maintenance is both good practice and good insurance hygiene.

---

Tips for Homeowners in Forest Lake

1. Review your building sum insured regularly Construction costs have risen sharply in recent years, and a sum insured that was adequate five years ago may no longer reflect the true cost of rebuilding your home. At 214 sqm with brick veneer construction, ducted air conditioning, and solar panels, your rebuild cost could be higher than you expect. Use an independent building cost calculator or speak with a quantity surveyor to sense-check your figure.

2. Confirm your solar panels are fully covered As mentioned above, solar panel coverage varies between policies. Check whether your panels are included in the building sum insured, whether there are any sub-limits, and whether the policy covers both damage to the panels themselves and any liability arising from them (such as a fire caused by a faulty inverter).

3. Shop around at renewal time A "Fair" rating means this quote is competitive, but it doesn't mean it's the best available. Insurers reprice risk differently, and even for the same property, premiums can vary by hundreds of dollars between providers. Comparing quotes through CoverClub takes only a few minutes and could reveal a meaningfully cheaper option without sacrificing cover quality.

4. Consider your excess settings Both the building and contents excess on this policy are set at $1,000. Opting for a higher voluntary excess — say, $2,000 or $2,500 — can reduce your annual premium noticeably. Just make sure the excess level you choose is an amount you could comfortably pay out of pocket in the event of a claim.

---

Compare Your Options with CoverClub

Whether you're reviewing an existing policy or shopping for cover for the first time, CoverClub makes it easy to see how your premium stacks up and find competitive quotes from a range of insurers. Get a home insurance quote today and see what Forest Lake homeowners are paying — you might be pleasantly surprised.