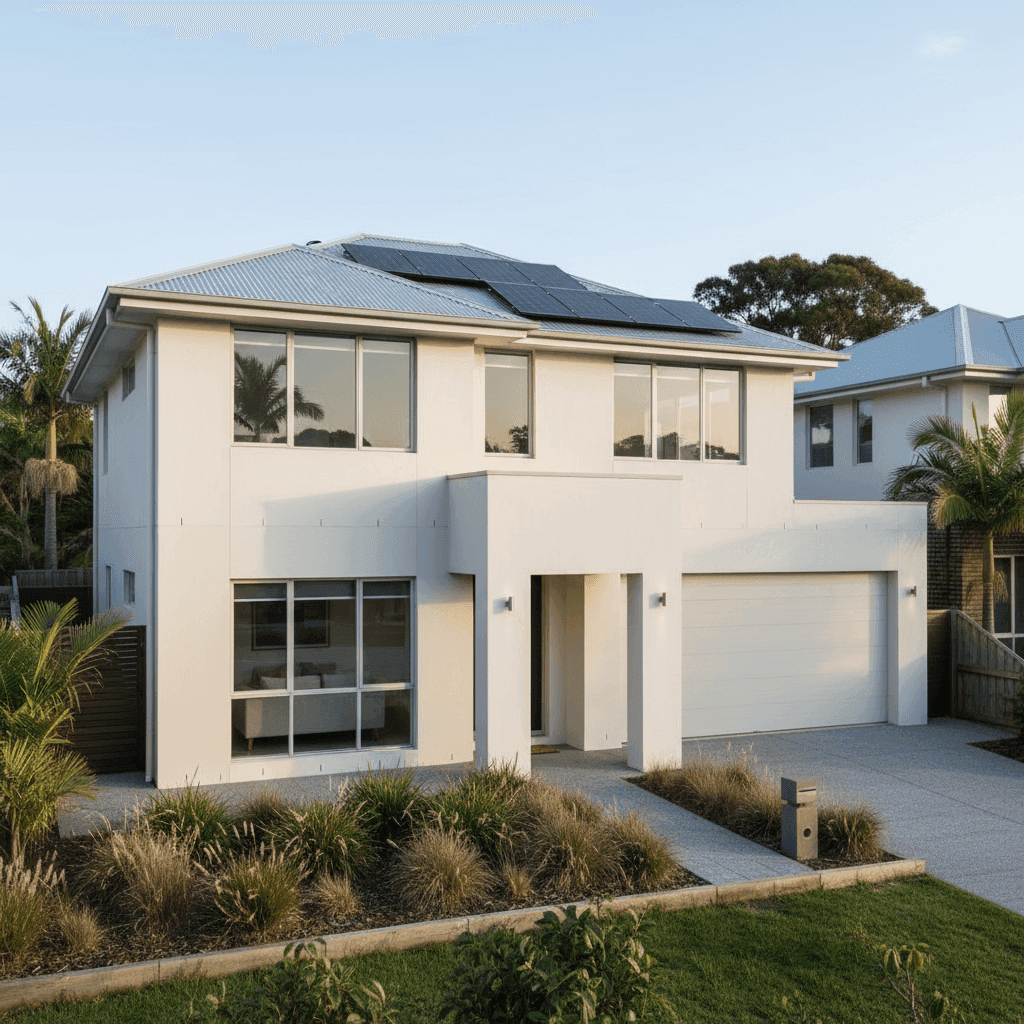

Forresters Beach, nestled on the Central Coast of New South Wales, is a sought-after coastal suburb known for its relaxed lifestyle and proximity to beautiful beaches. It's also the kind of location where getting your home insurance right really matters. This article breaks down a real home and contents insurance quote for a four-bedroom, free-standing home in the area — examining whether the price stacks up, how local premiums compare to broader benchmarks, and what property features are likely driving the cost.

---

Is This Quote Fair?

The quote in question comes in at $2,447 per year (or $242/month) for combined home and contents cover, with a building sum insured of $1,364,000 and contents valued at $125,000. The building excess is set at $3,000, while the contents excess sits at a more modest $500.

Our pricing analysis rates this quote as Fair — Around Average, which is actually a solid outcome for a property of this size and specification. Here's why that matters: "average" in insurance doesn't mean mediocre — it means the premium is sitting in a competitive band relative to comparable properties in the area, without being suspiciously cheap (which can signal inadequate cover) or unnecessarily expensive.

Given the high building sum insured of $1,364,000 — reflective of a modern, top-of-the-range home — a premium under $2,500 per year represents reasonable value. Homeowners should be cautious of quotes that appear dramatically lower, as they may involve underinsurance or significant coverage gaps.

---

How Forresters Beach Compares

To put this quote in proper context, it helps to look at how premiums in Forresters Beach sit relative to state and national figures. You can explore the full data on the Forresters Beach insurance stats page.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Forresters Beach (2260) | $3,245/yr | $3,101/yr |

| NSW | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

| Central Coast LGA | $8,387/yr | — |

A few things stand out here. First, this quote at $2,447 comes in below the suburb average of $3,245 and below the suburb median of $3,101 — placing it closer to the 25th percentile of $2,166 than the 75th percentile of $4,174. That's a genuinely competitive result based on 29 quotes sampled in the area.

Second, the NSW state average of $9,528 looks alarmingly high — but this is heavily skewed by high-value and high-risk properties across the state, which is why the median of $3,770 is a more useful reference point. Even against that median, this quote performs well. You can dig deeper into NSW home insurance benchmarks to understand the full picture.

At the national level, the average Australian home insurance premium sits at $5,347, with a median of $2,764. This quote is broadly in line with the national median, which reinforces the "Fair" rating — it's neither a bargain nor a rip-off, but a reasonable market price for the coverage on offer.

---

Property Features That Affect Your Premium

Several characteristics of this property are worth examining, as they each play a role in how insurers price the risk.

Hebel external walls are a popular choice in modern construction and are generally viewed favourably by insurers. Hebel (autoclaved aerated concrete) is fire-resistant and durable, which can help moderate premiums compared to older or more combustible wall materials.

Steel/Colorbond roofing is another feature that tends to attract competitive pricing. Colorbond is highly durable, weather-resistant, and performs well in storms — a key consideration on the Central Coast, where coastal weather can be unpredictable.

Slab foundation is the standard for modern builds and presents minimal additional risk from an underwriting perspective, unlike older stumped or pier foundations that can be more susceptible to movement and moisture.

Construction year of 2019 is a significant positive. Newer homes are built to current Australian Standards, including updated bushfire and wind-load requirements, which generally translates to lower risk profiles and more competitive premiums.

Top-of-the-range fittings do push the sum insured higher — and at $1,364,000 for a 244 sqm home, that's reflected in the rebuild cost estimate. However, it's critical that this figure accurately represents what it would cost to fully rebuild the home to the same standard. Underinsuring a premium-finish property is a common and costly mistake.

Solar panels are present on this property. While solar systems add value, they can also add a small amount to premiums as they represent an additional asset to insure and can complicate roof-related claims. It's worth confirming with your insurer exactly how solar panels are covered under your policy.

Ducted climate control is another high-value fixture that contributes to the contents and building sum insured. Ensuring this system is captured correctly in your policy — whether as a building fixture or a contents item — is an important detail to clarify.

---

Tips for Homeowners in Forresters Beach

1. Review your sum insured annually. Building costs in NSW have risen significantly in recent years. A home built in 2019 with top-of-the-range finishes should have its rebuild cost reassessed each year to avoid underinsurance. Many insurers offer a calculator, or you can consult a quantity surveyor for a professional estimate.

2. Confirm your solar panels are covered. Not all policies automatically cover solar panel systems under the building section, and some may treat them as an exclusion or a separate item. Read your Product Disclosure Statement (PDS) carefully and ask your insurer directly how solar is handled.

3. Consider your excess strategy carefully. This quote carries a $3,000 building excess — which is on the higher end. A higher excess typically lowers your premium, but it also means more out-of-pocket cost when you do make a claim. Make sure the excess level is something you could comfortably cover in an emergency.

4. Compare quotes before renewing. Even a "Fair" rated quote can be bettered at renewal time. Insurers regularly adjust their pricing models, and loyalty doesn't always pay. Shopping around — especially through a comparison platform — can surface better value without sacrificing cover quality.

---

Ready to Compare?

Whether you're a first-time buyer or a long-time Forresters Beach resident, it pays to know what the market looks like before committing to a policy. CoverClub makes it easy to compare home insurance quotes tailored to your property, so you can make a confident, informed decision. Enter your address and see how your current premium stacks up in minutes.