Home insurance costs in coastal New South Wales can vary enormously depending on where you live, what your home is built from, and how much cover you actually need. This article breaks down a real home and contents insurance quote for a free standing home in Forster, NSW 2428 — a popular coastal town on the Mid North Coast — and puts the numbers in context so you can make a more informed decision about your own cover.

---

Is This Quote Fair?

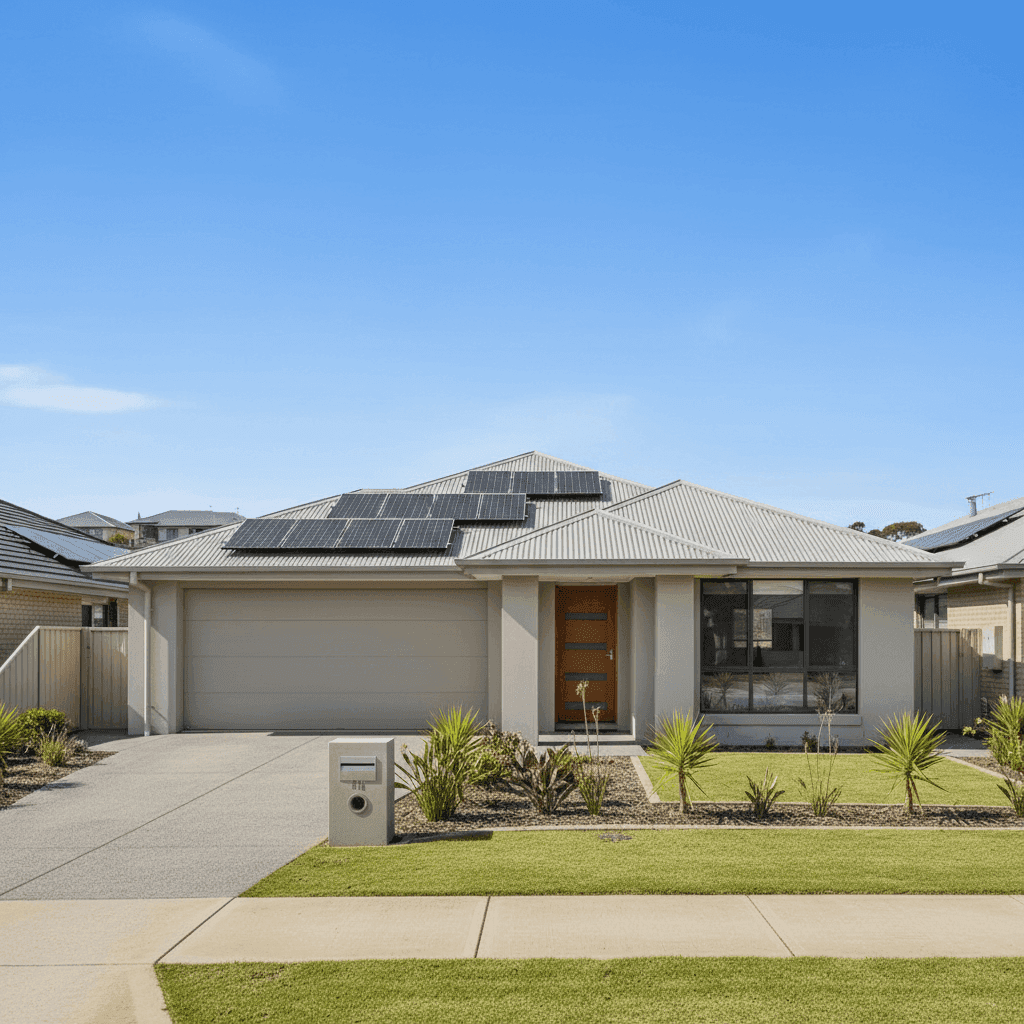

The quote in question sits at $3,275 per year (or $321 per month) for combined home and contents cover, with a building sum insured of $1,300,000 and contents valued at $221,000. The building excess is $2,000 and the contents excess is $1,000.

Our price rating for this quote is FAIR — Around Average, and the data backs that up. Compared to the suburb average for Forster of $4,460/yr, this quote is meaningfully cheaper — sitting roughly 27% below what other Forster homeowners are typically paying. However, it's worth noting that the suburb median is $2,725/yr, which means roughly half of Forster quotes come in below this figure. The quote lands in the upper half of the distribution — between the 50th and 75th percentile (the 75th percentile sits at $4,440/yr) — which is consistent with the "around average" rating.

The elevated sum insured of $1.3 million for the building is a significant driver here. For a newly built 139 sqm home with above-average fittings, that figure is ambitious but not unreasonable — especially given current construction costs in regional NSW. A higher replacement value will always push premiums upward, so the fact that this quote still lands near the middle of the market is a reasonable outcome.

---

How Forster Compares

Putting this quote into a broader geographic context helps illustrate just how much location influences what you pay.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Forster (2428) | $4,460/yr | $2,725/yr |

| Mid-Coast LGA | $4,463/yr | — |

| NSW State | $3,801/yr | $3,410/yr |

| National | $2,965/yr | $2,716/yr |

A few things stand out here. First, Forster and the broader Mid-Coast LGA are both notably more expensive than the national average, with averages running roughly 50% higher than what Australians pay across the country. This reflects the elevated risk profile of coastal NSW properties — flood exposure, storm activity, and proximity to water all contribute to higher base rates from insurers.

Second, the wide spread between Forster's 25th percentile ($1,509/yr) and 75th percentile ($4,440/yr) — based on a sample of 76 quotes — tells you that there's significant variation in what people are paying locally. Your specific property features, sum insured, and chosen insurer can all move your premium dramatically within that range.

---

Property Features That Affect Your Premium

This particular property has a number of characteristics that insurers weigh carefully when calculating risk and replacement cost.

Hebel external walls are a relatively modern construction choice — lightweight autoclaved aerated concrete panels that offer good thermal performance and fire resistance. Insurers generally view Hebel favourably from a fire risk perspective, though it can be more expensive to repair or replace than brick veneer, which may nudge the premium slightly higher.

Steel/Colorbond roofing is one of the most insurer-friendly roof types in Australia. It's durable, resistant to ember attack, and has a long service life. Compared to older tile roofs or heritage materials, Colorbond typically attracts lower premiums and is well-regarded across the industry.

Slab foundation and tile flooring are both low-risk features from an underwriting standpoint. Slabs are structurally sound and don't carry the subfloor moisture or pest risks associated with suspended timber floors. Tile flooring is similarly durable and easy to replace.

Solar panels are worth flagging specifically. While they're a great sustainability investment, solar panels do add to the replacement cost of your home and can complicate roof-related claims. It's important to confirm with your insurer that your solar system is explicitly covered under your building policy — some policies include it automatically, others require it to be listed.

Above-average fittings quality is another premium driver. Kitchens and bathrooms with premium fixtures, stone benchtops, or high-spec appliances cost significantly more to reinstate, and insurers price accordingly. Combined with the $1.3M building sum insured, this suggests the home is well-appointed — and the premium reflects that.

Being a 2023 build, the home benefits from modern construction standards, which typically means better structural integrity and compliance with current building codes. Newer homes often attract slightly more competitive rates than older stock, all else being equal.

---

Tips for Homeowners in Forster

1. Review your building sum insured annually. Construction costs in regional NSW have risen sharply in recent years. If your sum insured hasn't kept pace with current rebuild costs — including labour, materials, and professional fees — you could find yourself underinsured when it matters most. Use a quantity surveyor or your insurer's calculator to sense-check the figure each year.

2. Confirm solar panel coverage in writing. Don't assume your solar system is automatically covered. Ask your insurer directly whether panels, inverters, and mounting hardware are included under the building definition, and get it confirmed in your policy schedule. This is especially relevant for a newer home where the solar system may represent a significant portion of the overall installation cost.

3. Shop around — the spread in Forster is wide. With a 25th-to-75th percentile range of nearly $3,000 per year locally, there's real money to be saved by comparing multiple quotes. Even a "fair" quote can be beaten. Compare home insurance quotes for Forster at CoverClub to see what other insurers are offering for your specific property profile.

4. Consider your excess settings carefully. This policy carries a $2,000 building excess and $1,000 contents excess. Opting for a higher excess is a legitimate way to reduce your annual premium — but only if you're confident you could comfortably cover that amount out of pocket in the event of a claim. For a property of this value, it's worth modelling a few scenarios to find the right balance.

---

Compare Your Options with CoverClub

Whether you're reviewing an existing policy or shopping for the first time, comparing quotes is the single most effective way to make sure you're not overpaying. CoverClub makes it easy to benchmark your premium against real data from your suburb, your state, and across Australia. Get a home insurance quote today and see how your current cover stacks up.