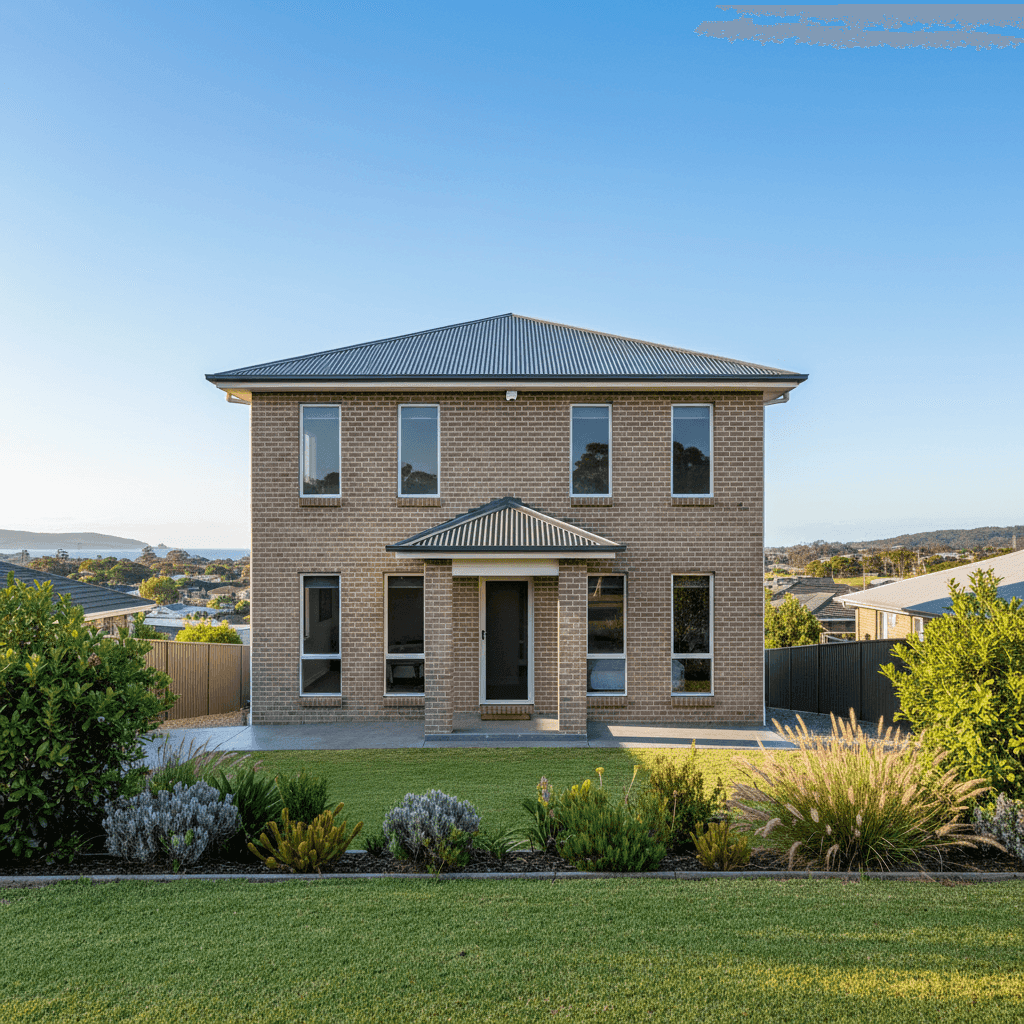

Forster is one of the Mid-North Coast's most popular coastal towns — a relaxed holiday destination that many Australians now call home permanently. If you own a free standing home in the area, understanding what you should be paying for home and contents insurance is just as important as choosing the right policy. This article breaks down a real quote for a four-bedroom, two-bathroom brick veneer home in Forster NSW 2428, and puts the numbers into context so you can make a more informed decision.

---

Is This Quote Fair?

The quote in question comes in at $2,552 per year (or $245 per month) for combined home and contents cover, with a building sum insured of $609,000 and contents valued at $50,000. Both the building and contents carry a $2,000 excess.

Our price rating for this quote is FAIR — Around Average, which is a solid outcome for a coastal property in NSW. Here's why that matters: coastal locations across Australia are frequently exposed to elevated weather risks — storm surge, high winds, and flooding — all of which push premiums up significantly. The fact that this quote sits in the "fair" range, rather than "expensive," suggests the property's characteristics are working in its favour.

To put it plainly, paying $2,552 annually for a well-sized coastal home with $609,000 in building cover is not a bad result. But context is everything — let's dig into the comparisons.

---

How Forster Compares

When you stack this quote against the broader market, the picture becomes clearer. Based on data from 105 quotes collected for the Forster 2428 area:

| Benchmark | Premium |

|---|---|

| This Quote | $2,552/yr |

| Suburb 25th Percentile | $1,649/yr |

| Suburb Median | $3,604/yr |

| Suburb Average | $4,910/yr |

| Suburb 75th Percentile | $7,006/yr |

| LGA (Mid-Coast) Average | $5,840/yr |

| NSW State Median | $3,770/yr |

| NSW State Average | $9,528/yr |

| National Median | $2,764/yr |

| National Average | $5,347/yr |

This quote sits below both the suburb median ($3,604) and the suburb average ($4,910), which is encouraging. It also comes in under the NSW state median of $3,770 and is remarkably close to the national median of $2,764.

The wide spread of premiums in Forster — from $1,649 at the 25th percentile all the way to $7,006 at the 75th — highlights just how variable home insurance pricing can be in coastal areas. Individual risk factors like flood zone classification, proximity to water, and property construction all play a significant role in where any given quote lands within that range.

The LGA average for Mid-Coast ($5,840) is notably higher than this quote, reinforcing that the property's specific features are helping keep costs down.

---

Property Features That Affect Your Premium

Several characteristics of this home are worth discussing in the context of insurance pricing.

Brick Veneer Walls & Colorbond Roof

Brick veneer construction is generally viewed favourably by insurers. It offers good resistance to fire and wind compared to lightweight cladding materials, which can translate to lower premiums. The steel Colorbond roof is similarly well-regarded — it's durable, resistant to ember attack, and holds up well in coastal conditions where salt air can corrode lesser materials over time.

Slab Foundation

A concrete slab foundation is one of the more straightforward foundations for insurers to assess. Unlike elevated stumped homes, slab homes have no underfloor cavity that can trap moisture or be damaged in flood events. That said, slabs can be more vulnerable to certain types of subsidence, so it's worth ensuring your policy covers gradual movement where relevant.

Slightly Elevated (Less Than 1m)

The property is noted as being elevated by less than one metre. While this is a modest elevation, it can still provide a small degree of protection against surface water intrusion during heavy rain events — a meaningful consideration in a coastal town like Forster that can experience intense summer storms.

Timber & Laminate Flooring

Timber and laminate flooring is a common feature in Australian homes and is generally straightforward to replace under a contents or building claim. However, it's worth noting that these materials can be susceptible to water damage, so ensuring your policy covers escape of liquid and storm-related water ingress is important.

Ducted Climate Control

The presence of ducted air conditioning adds to the rebuild value of the home and is correctly factored into the building sum insured. These systems can be costly to replace, so it's important they're accounted for in your coverage — and it appears they are here.

No Pool or Solar Panels

The absence of a pool and solar panels simplifies the risk profile slightly. Both additions can increase premiums — pools due to liability considerations, and solar panels because of the cost to repair or replace rooftop systems after storm or hail damage.

---

Tips for Homeowners in Forster

1. Review Your Building Sum Insured Regularly

Construction costs have risen sharply across Australia in recent years. A sum insured of $609,000 for a 214 sqm home works out to roughly $2,845 per square metre — which is within a reasonable range, but worth revisiting annually. Being underinsured at claim time can leave you significantly out of pocket.

2. Understand Your Flood and Storm Cover

Forster sits on the Mid-North Coast and is no stranger to heavy rainfall and coastal storms. Make sure your policy explicitly covers flood (not just storm), as these are often defined differently by insurers. Some policies exclude riverine flooding entirely, so read the Product Disclosure Statement (PDS) carefully.

3. Consider Your Excess Strategically

Both the building and contents excess on this policy are set at $2,000. A higher excess generally means a lower premium, but you need to be comfortable covering that amount out of pocket in the event of a claim. If cash flow is a concern, it may be worth comparing quotes with a $1,000 excess to see how much the premium difference actually is.

4. Don't Set and Forget

The wide premium range in Forster (from under $1,700 to over $7,000) means there's real value in shopping around at renewal time. Insurers reprice risk regularly, and the market is competitive. Even if your current quote seems fair, comparing alternatives every year or two is a smart habit.

---

Ready to Compare?

Whether you're a long-time Forster local or you've recently made the move to the Mid-North Coast, getting the right home insurance at the right price matters. At CoverClub, we make it easy to see how your quote stacks up against real market data — not just generic estimates.

Get a home insurance quote today at CoverClub and find out where you sit in the market. You might be surprised at what you find.