If you own a free standing home in Frankston South, VIC 3199, you're sitting in one of Melbourne's more desirable coastal-fringe suburbs — and your home insurance premium likely reflects that. This article breaks down a real building insurance quote for a five-bedroom, three-bathroom home in the area, comparing it against local, state, and national benchmarks to help you understand whether you're paying a fair price.

---

Is This Quote Fair?

The quote in question comes in at $4,475 per year (or $436/month) for building-only cover, with a $1,000 building excess and a sum insured of $1,687,000.

Our assessment: this premium is rated Expensive — above average for the area.

To put that in perspective, the suburb average for Frankston South sits at just $2,305/year, and the median is even lower at $2,084/year. This quote is nearly double the suburb median, which is a significant gap worth understanding before you simply accept the renewal.

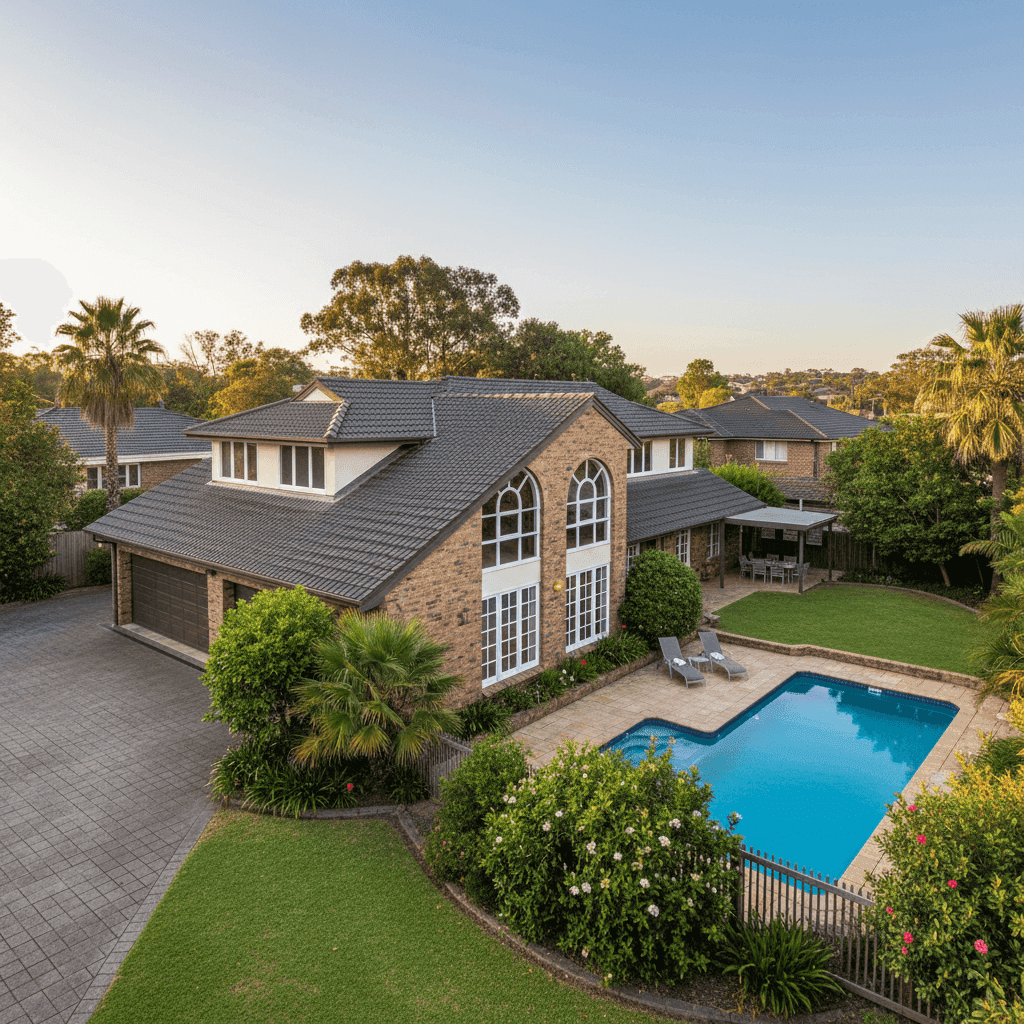

That said, context matters. The property is a large, 334 sqm home built in 1954 with above-average fittings, a swimming pool, and a high sum insured of $1.687 million. Each of these factors individually pushes premiums upward — together, they can compound substantially. Insurers aren't just pricing the suburb; they're pricing the specific risk profile of your home.

Still, even accounting for these features, a premium nearly double the local average warrants scrutiny. It's worth shopping around.

---

How Frankston South Compares

Understanding where Frankston South sits in the broader insurance landscape helps you gauge whether a quote is reasonable or inflated.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Frankston South (3199) | $2,305/yr | $2,084/yr |

| Frankston LGA | $3,283/yr | — |

| Victoria (VIC) | $3,000/yr | $2,718/yr |

| National (Australia) | $5,347/yr | $2,764/yr |

(Based on 103 quotes sampled for the Frankston South suburb. [View full suburb stats](https://coverclub.com.au/stats/VIC/3199/frankston-south) | [VIC stats](https://coverclub.com.au/stats/VIC) | [National stats](https://coverclub.com.au/stats/national))

A few things stand out here:

- Frankston South premiums are notably lower than the VIC average, suggesting the suburb is considered relatively low-risk compared to many other Victorian postcodes.

- The national average of $5,347/year is heavily skewed by high-risk areas such as flood-prone regions in Queensland and cyclone-exposed parts of northern Australia. The national median of $2,764/year is a far more representative figure for most homeowners.

- The quote of $4,475/year sits above the VIC average but below the national average — placing it in a somewhat elevated but not extraordinary range when considered nationally.

- The 75th percentile for Frankston South is $2,656/year, meaning this quote is well above what even the most expensive quarter of local properties typically pay.

---

Property Features That Affect Your Premium

Several characteristics of this particular home help explain why the premium sits above the suburb norm.

Size and Sum Insured At 334 sqm, this is a large home by any measure. The sum insured of $1,687,000 reflects the cost to fully rebuild a property of this scale with above-average fittings — and insurers price directly against that rebuild cost. A higher sum insured means a higher premium, full stop.

Age of Construction (1954) Homes built in the 1950s often carry higher premiums due to the increased likelihood of ageing infrastructure — older wiring, outdated plumbing, and materials that may no longer meet modern building codes. Brick veneer construction from this era can also be more susceptible to certain types of structural movement, particularly on stump foundations.

Stump Foundation The property sits on stumps, which is common for older homes in Victoria. While stumps are a well-understood building method, they can be more vulnerable to subsidence and movement over time, especially as timber stumps age or if soil conditions shift. This adds a layer of risk that insurers factor into their pricing.

Swimming Pool A pool increases the insurable value of the property and adds liability considerations. Pool surrounds, pumping equipment, and associated structures all contribute to the overall rebuild cost — and therefore the premium.

Above-Average Fittings High-quality fixtures, finishes, and fittings cost more to repair or replace. Insurers adjust premiums accordingly when the internal specification of a home is above standard.

Timber and Laminate Flooring While attractive and durable, timber flooring can be costly to repair or replace following water damage or fire. This is a modest but real factor in premium calculations.

Ducted Climate Control Ducted systems are expensive assets — installation and replacement costs can run into the tens of thousands. Their inclusion in the insured value contributes to the overall sum insured and premium.

---

Tips for Homeowners in Frankston South

If your premium feels high, here are some practical steps to consider:

1. Compare at least three quotes The single most effective way to reduce your premium is to shop around. Use a comparison platform like CoverClub to see multiple quotes side by side without having to contact each insurer individually. Given this quote is nearly double the suburb median, there's real potential for savings.

2. Review your sum insured carefully Make sure your sum insured reflects the actual rebuild cost — not the market value of your property. Overinsuring is a common and costly mistake. Consider using a professional building cost estimator or the calculator tools provided by insurers to arrive at an accurate figure.

3. Ask about excess trade-offs Increasing your excess from $1,000 to $2,500 or even $5,000 can meaningfully reduce your annual premium. If you're financially comfortable covering a higher out-of-pocket cost in the event of a claim, this is often a smart trade-off.

4. Highlight any upgrades or risk mitigations If you've had the home's electrical or plumbing systems updated since purchase, make sure your insurer knows. Modernised infrastructure reduces risk and some insurers will adjust your premium accordingly. Similarly, security upgrades such as monitored alarms or deadbolts can attract discounts with certain providers.

---

Compare Your Options with CoverClub

Whether you're renewing your policy or shopping for the first time, it pays to compare. CoverClub makes it easy to benchmark your quote against real data from your suburb and see what other insurers are offering for a home like yours. Get a building insurance quote now and find out if you could be paying less — without sacrificing cover.