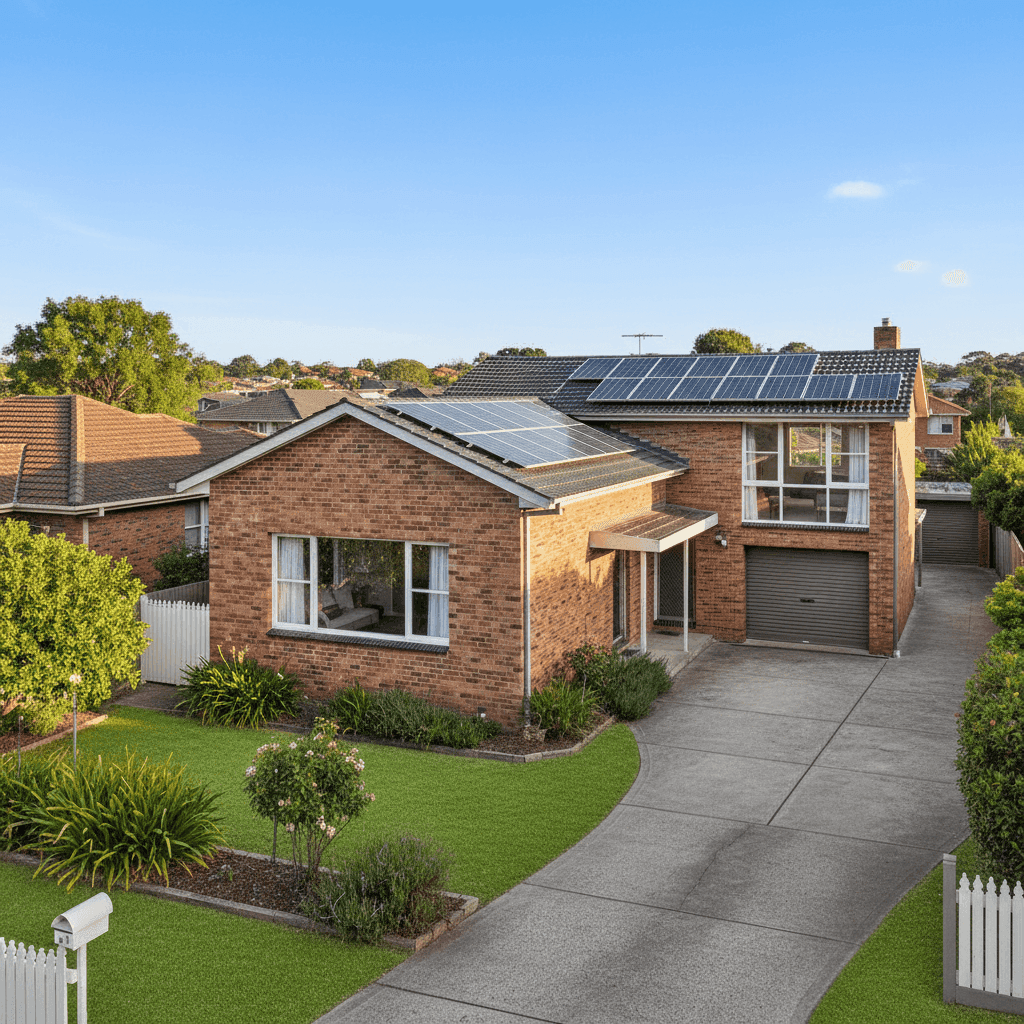

If you own a free standing home in Frankston, VIC 3199, you've probably wondered whether you're paying too much — or too little — for home and contents insurance. With premiums varying widely depending on property features, location risk, and the insurer you choose, it can be hard to know where you stand. This article breaks down a real quote for a 3-bedroom, 2-bathroom brick veneer home in Frankston, compares it against local and national benchmarks, and offers practical tips to help you get better value from your cover.

---

Is This Quote Fair?

The quote in question comes in at $1,811 per year (or $174/month) for combined home and contents insurance, covering a building sum insured of $640,000 and contents valued at $120,000. Both the building and contents excess sit at $1,000.

Our price rating for this quote is Expensive — above average for the Frankston area.

To put that in context: the suburb average premium across 59 quotes collected for Frankston (3199) is $1,355 per year, with a median of $1,288. This quote sits roughly $456 above the suburb average — a meaningful gap of around 34%.

That said, "expensive" doesn't automatically mean "wrong." A higher-than-average premium can reflect legitimate factors: a larger-than-typical building size (169 sqm is comfortably above the entry-level range), a higher sum insured, the presence of solar panels, ducted climate control, and the age of the home (built in 1962). Insurers price older homes at a premium because they can carry greater replacement cost risk, particularly when it comes to materials and compliance with modern building codes.

Still, if you're paying above the suburb average, it's worth shopping around to confirm you're not simply overpaying for equivalent cover.

---

How Frankston Compares

One of the more reassuring findings here is how affordable Frankston is relative to the broader insurance market.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Frankston (3199) | $1,355/yr | $1,288/yr |

| Victoria (VIC) | $3,000/yr | $2,718/yr |

| National | $5,347/yr | $2,764/yr |

Even at $1,811, this quote sits well below the Victorian state average of $3,000 and is a fraction of the national average of $5,347 — a figure heavily influenced by high-risk regions in Queensland, Western Australia, and the Northern Territory where cyclone, flood, and storm exposure drives premiums skyward.

Interestingly, the LGA-level data for Frankston shows a local government area average of $3,283/yr — higher than both the suburb figure and the state average. This suggests there may be pockets within the broader Frankston LGA that carry elevated risk, which can sometimes pull the LGA average up even when a specific postcode like 3199 sits lower.

For a broader picture of how Victorian premiums stack up, visit our VIC insurance statistics page, or explore national home insurance data to see where your postcode lands on the spectrum.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on what insurers charge. Here's how each one plays out:

Brick Veneer Walls & Tiled Roof Brick veneer is one of the most common external wall types in Australian suburbia, and insurers generally view it favourably. It's durable, fire-resistant, and relatively straightforward to repair or replace. Similarly, a tiled roof is considered a standard, low-risk choice. Together, these features help keep the premium from climbing higher than it might for, say, a weatherboard home with a metal or older Colorbond roof.

Stump Foundation The home sits on stumps — a common foundation type for homes built in the mid-twentieth century, particularly in Victoria. While stumps are entirely normal for the era, they can attract slightly higher premiums than slab-on-ground construction because of the potential for movement, rot (in the case of timber stumps), or pest damage over time. Insurers may factor this in when assessing structural risk.

Construction Year: 1962 At over 60 years old, this home pre-dates many modern building standards. Older homes can be more expensive to rebuild to current code requirements, which is one reason the $640,000 building sum insured is appropriate — and why the premium reflects that rebuilding cost rather than market value.

Solar Panels The presence of rooftop solar adds modest complexity to a home insurance policy. Panels represent an additional asset to insure, and their installation introduces some risk considerations (e.g., roof penetrations, electrical systems). Most insurers cover solar panels under the building policy, but it's worth confirming the sum insured accounts for their replacement value.

Ducted Climate Control Ducted heating and cooling systems are a fixed part of the building and are typically covered under building insurance. Like solar panels, they add to the overall replacement cost, which is reflected in the sum insured and, consequently, the premium.

No Pool, No Cyclone Risk The absence of a swimming pool removes a common liability and maintenance risk factor. And being located in metropolitan Melbourne, Frankston sits well outside any designated cyclone risk zone — a significant premium advantage compared to properties in northern Australia.

---

Tips for Homeowners in Frankston

1. Review your sum insured annually Building costs have risen sharply in recent years. Make sure your $640,000 sum insured still reflects the true cost of rebuilding your home — not its market value, but what it would actually cost to demolish, clear, and reconstruct to current standards. Underinsurance is one of the most common and costly mistakes homeowners make.

2. Ask about stump inspection discounts If your stumps have been professionally inspected or recently replaced with concrete equivalents, let your insurer know. Some will adjust your premium or risk assessment accordingly, particularly if you can provide documentation.

3. Compare at least three quotes Given this quote is rated above the suburb average, it's well worth running a comparison. Premiums for the same property can vary by hundreds of dollars between insurers. Get a quote through CoverClub to see what other providers would charge for equivalent cover.

4. Consider your excess strategically Both the building and contents excess are set at $1,000. Opting for a higher voluntary excess — say, $2,000 — can reduce your annual premium meaningfully. Just make sure the saving is worth the out-of-pocket cost if you ever do need to claim.

---

Compare Your Options with CoverClub

Whether you're reviewing an existing policy or shopping for cover on a new property, CoverClub makes it easy to see how your premium stacks up. Our suburb and state-level data gives you a real-world benchmark, so you're never left guessing. Start a quote today at CoverClub and find out if there's a better deal waiting for your Frankston home.