If you own a free standing home in Frederickton, NSW 2440, you're likely curious about what a fair home insurance premium looks like — and whether you're paying too much. This article breaks down a real home and contents insurance quote for a two-bedroom weatherboard property in Frederickton, comparing it against local, state, and national benchmarks to help you understand where you stand.

---

Is This Quote Fair?

The short answer: yes — and then some. This quote comes in at $2,665 per year (or $249/month), which our pricing data rates as CHEAP — meaning it sits well below average for the area.

To put that in context, the average premium across sampled quotes in the Frederickton suburb sits at $5,170 per year, with a median of $5,006. That means this quote is roughly half the local average — a significant saving for a homeowner who's done their research or landed with a competitive insurer.

Even at the 25th percentile (i.e., the cheapest quarter of quotes in the suburb), premiums are still running at $4,852/yr — nearly double this quote. That's a strong signal that this is genuinely competitive pricing, not just marginally below par.

Of course, it's worth noting that the suburb sample size here is 7 quotes, so the local data is directionally useful but not statistically definitive. Still, combined with state and national comparisons, the picture is consistent: this is a well-priced policy.

---

How Frederickton Compares

Understanding how Frederickton sits within the broader insurance landscape helps frame what's driving premiums in the area.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Frederickton (suburb) | $5,170/yr | $5,006/yr |

| Port Macquarie-Hastings LGA | $7,001/yr | — |

| NSW (state) | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out here. The NSW state average of $9,528/yr is exceptionally high — but the state median of $3,770/yr tells a more nuanced story. NSW contains some of Australia's most flood- and bushfire-prone regions, and a handful of very high-risk properties can drag the average up significantly. The median is a better reflection of what a typical NSW homeowner pays.

Frederickton's suburb average of $5,170/yr sits above both the NSW median and the national median ($2,764/yr), suggesting the area carries moderate-to-elevated risk in the eyes of insurers — likely driven by factors like flood risk near the Macleay River, regional location, and the age and construction style of local homes.

The Port Macquarie-Hastings LGA average of $7,001/yr is notably higher than the Frederickton suburb average, which may reflect the diversity of risk profiles across this large coastal LGA — including beachside and flood-prone properties that push premiums higher.

For localised data, you can explore Frederickton suburb insurance stats, NSW state insurance data, and national home insurance benchmarks.

---

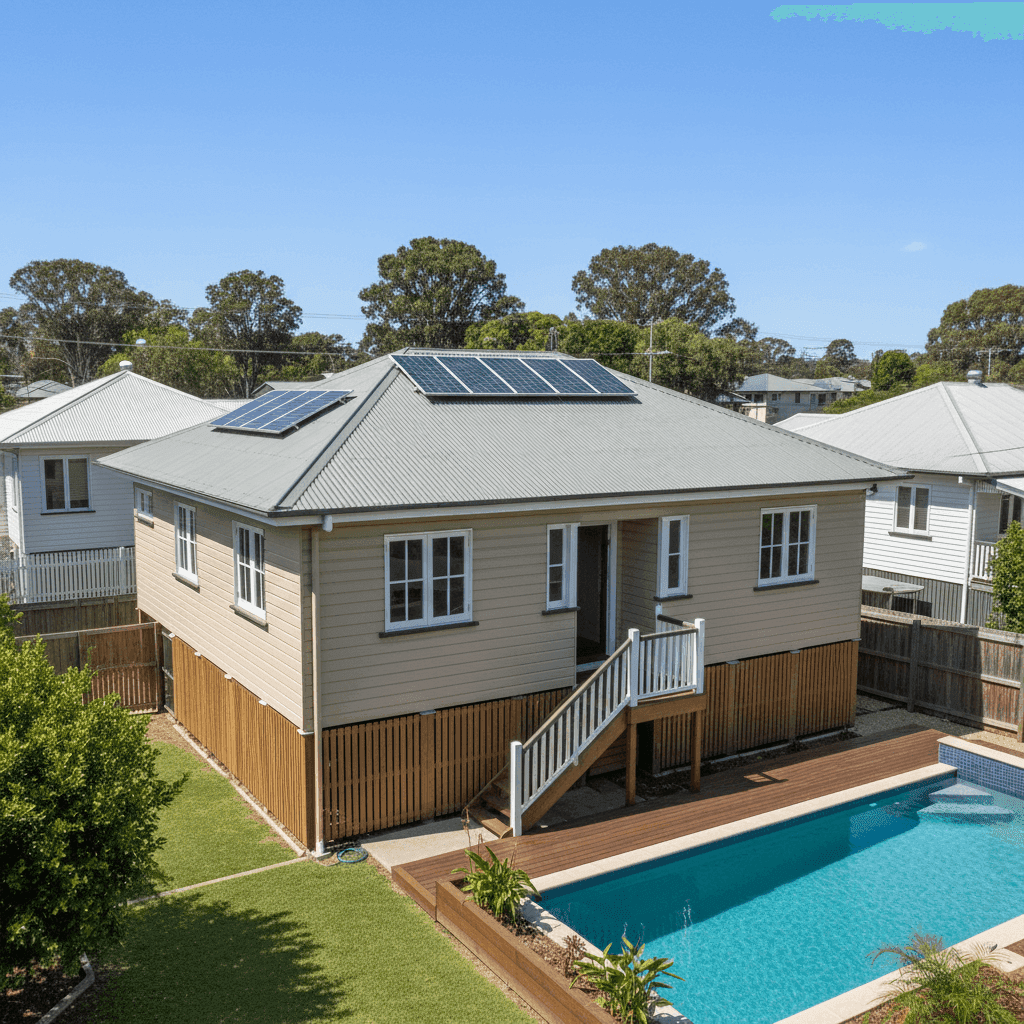

Property Features That Affect Your Premium

Several characteristics of this particular property influence how insurers price the risk. Here's what's at play:

Weatherboard timber construction is one of the most significant factors. Timber-framed homes with weatherboard cladding are considered higher risk than brick veneer or double-brick homes due to their susceptibility to fire, rot, and pest damage. Insurers typically price this in — so getting a competitive rate on a weatherboard home is a genuine win.

Steel/Colorbond roofing is actually a positive factor. Colorbond is durable, low-maintenance, and performs well in both high-wind and fire-prone conditions. It's generally viewed more favourably by insurers than older tile roofs, which can crack or dislodge.

Stump foundations (stumps) mean the home is elevated, which can be a double-edged sword. On one hand, being elevated by less than 1 metre can provide some protection from minor flooding and ground moisture. On the other, stump homes can be more vulnerable to underfloor damage and may require more maintenance over time.

Timber/laminate flooring is noted by insurers largely in the context of contents and water damage claims. Timber floors can be costly to repair or replace following water ingress, which may factor into the contents and building sum insured.

A swimming pool adds liability exposure and can slightly increase premiums — not dramatically, but insurers do account for the risk of injury on the property.

Solar panels are increasingly common and generally don't spike premiums significantly, but they do add to the replacement cost of the building. At a $392,000 sum insured, it's worth confirming your policy explicitly covers solar panel damage (including storm and hail events).

Ducted climate control is a relatively high-value fixed installation. Ensure it's captured within your building sum insured, as ducted systems can cost $10,000–$20,000+ to replace.

Standard fittings quality keeps the rebuild cost estimate grounded — premium fittings like stone benchtops or custom joinery would push the sum insured higher.

---

Tips for Homeowners in Frederickton

1. Double-check your sum insured reflects current rebuild costs Construction costs have risen sharply across regional NSW in recent years. A $392,000 sum insured for a 130 sqm weatherboard home is worth validating against a current building cost calculator — underinsurance is one of the most common and costly mistakes homeowners make.

2. Review your contents cover carefully At $20,000, the contents sum insured is on the lower end. Consider whether this covers your appliances, furniture, electronics, and personal belongings at today's replacement cost — not what you paid for them years ago.

3. Understand your flood risk Frederickton sits near the Macleay River, and flooding is a genuine risk in parts of the 2440 postcode. Check whether your policy includes flood cover as standard or as an optional add-on — and if it's excluded, consider whether that's a gap you can afford.

4. Compare quotes at renewal time This quote is priced well below the suburb average, but insurance markets shift. Set a reminder to compare quotes before your renewal date each year — loyalty doesn't always pay in the insurance world, and switching can save hundreds.

---

Compare Your Own Quote

Whether you're a Frederickton local or researching home insurance across regional NSW, CoverClub makes it easy to see how your premium stacks up. Get a quote today at CoverClub and find out if you're paying a fair price — or if there's a better deal waiting for you.