If you own a free standing home in Gaven, QLD 4211, you've probably wondered whether you're paying too much — or too little — for home and contents insurance. This article breaks down a real quote for a four-bedroom property in the suburb, benchmarks it against local, state, and national figures, and offers practical advice for getting the best value cover.

---

Is This Quote Fair?

The quote in question sits at $3,083 per year (or roughly $289 per month) for combined home and contents insurance, covering a building sum insured of $400,000 and contents valued at $75,000. Both the building and contents excess are set at $1,000.

Our pricing analysis rates this quote as CHEAP — below the suburb average. That's genuinely good news for the homeowner. In a market where insurance premiums have climbed sharply across Queensland over the past few years, landing below the local average is a meaningful win.

To put it in perspective: the suburb average for Gaven sits at $4,159 per year, and the suburb median is even higher at $4,304 per year. This quote comes in roughly $1,076 below the suburb average — a saving of about 26%. It also sits comfortably below the suburb's 25th percentile of $3,264, meaning it's cheaper than at least three-quarters of comparable quotes in the area. That's a strong result.

Of course, a low premium only represents value if the cover is adequate. With $400,000 in building cover and $75,000 for contents, this policy appears well-calibrated for a four-bedroom, three-bathroom home of this size and age.

---

How Gaven Compares

Understanding how Gaven fits into the broader insurance landscape helps put any individual quote into context. You can explore the full data on our Gaven suburb stats page.

| Benchmark | Annual Premium |

|---|---|

| This Quote | $3,083 |

| Gaven Suburb Average | $4,159 |

| Gaven Suburb Median | $4,304 |

| QLD State Average | $9,129 |

| QLD State Median | $3,903 |

| National Average | $5,347 |

| National Median | $2,764 |

| Scenic Rim LGA Average | $8,744 |

A few things stand out here. Queensland's state average of $9,129 is dramatically higher than both the national average and the Gaven suburb average — a reflection of the significant insurance risk posed by cyclones, floods, and severe weather events across much of the state. However, it's worth noting that the QLD median of $3,903 is far more modest, suggesting that extreme premiums in high-risk postcodes (think Far North Queensland and flood-prone inland areas) are pulling the state average upward considerably.

Gaven, located in the Gold Coast hinterland fringe, benefits from a relatively favourable risk profile compared to many other Queensland postcodes. The suburb is not classified as a cyclone risk area, which is a significant factor keeping premiums lower than the state norm.

Interestingly, the Scenic Rim LGA average of $8,744 is much higher than Gaven's suburb average, which suggests that neighbouring areas within the same local government region carry substantially more risk — likely due to flood exposure and bushfire-prone terrain further inland.

For a broader picture of how Queensland compares to the rest of the country, visit our QLD insurance stats page or the national overview.

---

Property Features That Affect Your Premium

Every home is different, and insurers weigh up a range of property characteristics when calculating your premium. Here's how the features of this particular property are likely influencing the cost:

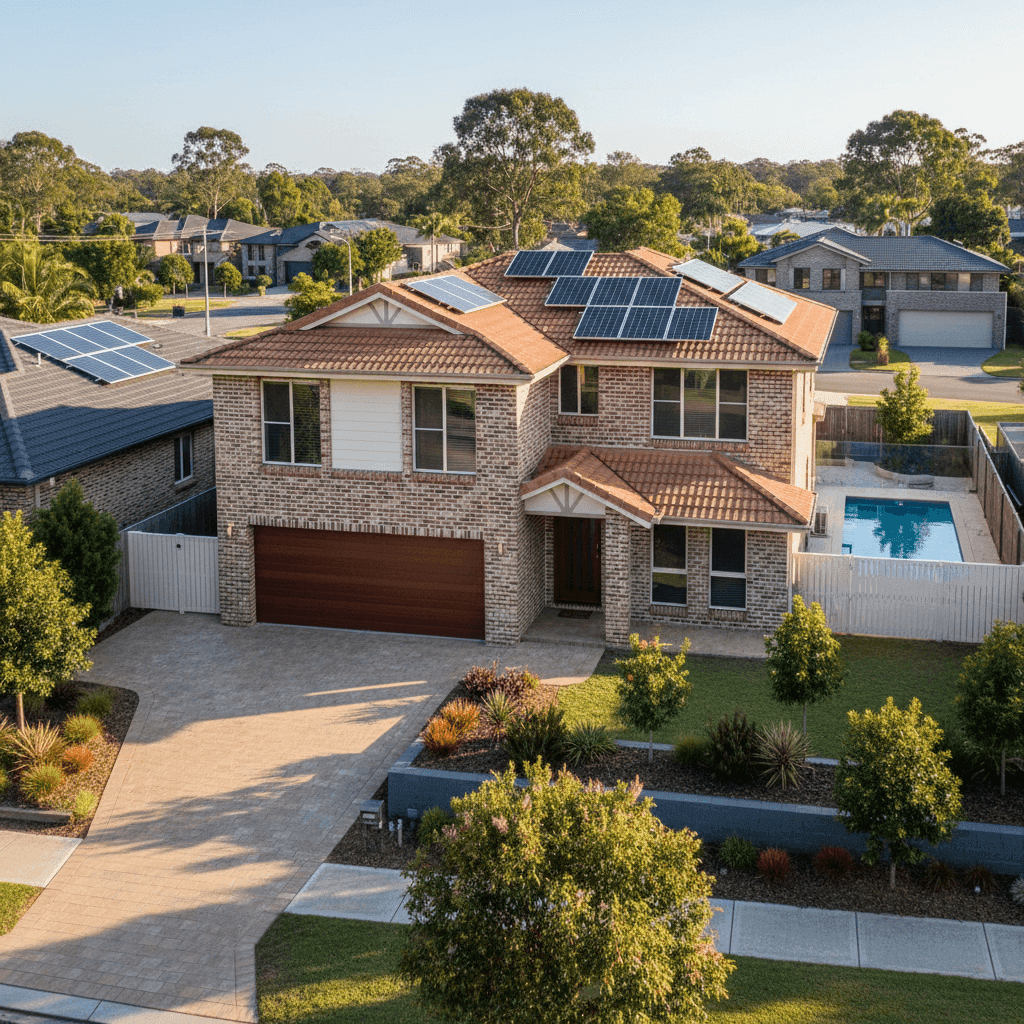

Brick Veneer Walls & Tiled Roof Brick veneer construction with a tiled roof is generally viewed favourably by insurers. These materials offer solid fire resistance and structural durability compared to weatherboard or Colorbond alternatives. This combination likely contributes to a more competitive premium.

Slab Foundation, Slightly Elevated The home sits on a concrete slab and is elevated by less than one metre. While a full Queenslander-style elevation (typically 1.8m+) can sometimes reduce flood risk ratings, a modest elevation still provides a small degree of protection against surface water intrusion — a factor worth noting given Queensland's storm season.

Construction Year: 1985 Homes built in the mid-1980s are a mixed bag for insurers. They're old enough that some systems (plumbing, wiring, roofing) may be approaching the end of their serviceable life, but they're also generally well past the early-build quality issues sometimes seen in newer construction. Keeping on top of maintenance is key for homes of this vintage.

Swimming Pool A pool adds value to the property but also introduces liability considerations. Most insurers factor pool liability into their home policies, and it's worth confirming your policy covers pool-related incidents, including third-party injury.

Solar Panels Solar panels are increasingly common in Queensland, and most modern home insurance policies cover them as a fixed fixture of the building. Confirm your building sum insured is sufficient to cover replacement costs, as a quality solar system can represent a significant portion of rebuild value.

Ducted Climate Control Ducted air conditioning is treated as a fixed building fixture and should be included in your building sum insured. At $400,000, the cover here appears to account for this feature appropriately.

Vinyl Flooring & Standard Fittings Vinyl flooring and standard-grade fittings keep the overall rebuild cost estimate reasonable. High-end finishes such as marble benchtops or imported hardwood floors would push the required sum insured — and therefore the premium — noticeably higher.

---

Tips for Homeowners in Gaven

1. Review your sum insured regularly Building costs have risen sharply in recent years due to labour shortages and material price increases. A sum insured of $400,000 may be appropriate today, but it's worth recalculating your estimated rebuild cost annually to avoid being underinsured. Many insurers offer free online calculators to help.

2. Don't overlook your pool and solar in your building cover Both your swimming pool and solar panel system should be explicitly included in your building sum insured. Check your policy schedule to confirm they're listed and that the total insured amount reflects their replacement value.

3. Maintain your property to protect your claim eligibility For a home built in 1985, routine maintenance is especially important. Insurers can — and do — decline claims where damage is attributed to gradual deterioration or lack of upkeep. Keep records of roof inspections, plumbing checks, and any repairs carried out.

4. Compare quotes at renewal time Even if your current premium looks competitive, the insurance market shifts constantly. Insurers reprice risk regularly, and a policy that was great value last year may not be the best option at renewal. Shopping around takes only a few minutes and can result in meaningful savings.

---

Find a Better Deal with CoverClub

Whether you're renewing your existing policy or taking out cover for the first time, comparing quotes is the single most effective way to make sure you're not overpaying. CoverClub makes it easy to benchmark your premium against real data from your suburb and beyond. Get a home insurance quote today and see how your current cover stacks up.