If you own a free standing home in Gelliondale, VIC 3971, you're likely no stranger to the challenge of finding affordable, reliable home insurance. Nestled in the South Gippsland region of Victoria, Gelliondale is a small rural locality surrounded by farmland and bushland — a setting that comes with its own unique insurance considerations. This article breaks down a real home and contents insurance quote for a 3-bedroom property in the area, examines how it stacks up against Victorian and national benchmarks, and offers practical advice for keeping your premiums in check.

---

Is This Quote Fair?

The quote in question comes in at $3,822 per year (or $375 per month) for combined home and contents cover — a building sum insured of $847,000 and contents valued at $50,000. Based on our pricing analysis, this quote is rated Expensive, sitting noticeably above both the Victorian and national averages.

To put that into perspective:

- The VIC state average premium is $2,921/yr, and the median is $2,694/yr

- The national average is $2,965/yr, with a national median of $2,716/yr

At $3,822, this quote is roughly 31% above the Victorian average and about 29% above the national average. That's a significant gap, and it's worth understanding what's driving the cost before simply accepting the figure.

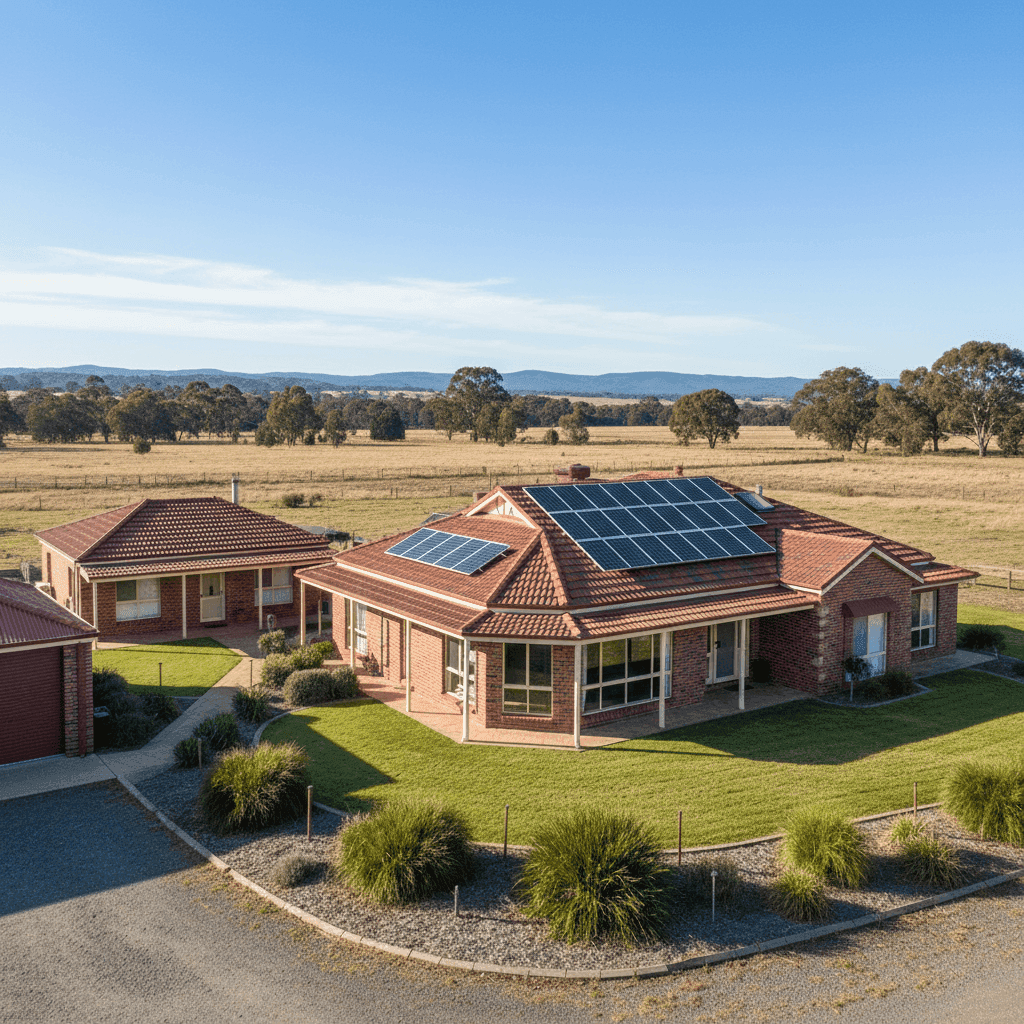

That said, "expensive" doesn't necessarily mean "wrong." A high building sum insured ($847,000 for a 139 sqm double brick home), the presence of a granny flat, and the property's rural location all contribute to a more complex risk profile. Still, the size of the premium gap suggests there may be room to shop around.

---

How Gelliondale Compares

Unfortunately, there isn't enough localised data available to provide a suburb-level average for Gelliondale specifically — which isn't unusual for smaller rural localities. You can check the Gelliondale insurance stats page for the latest figures as more data becomes available.

What we can say with confidence is that this quote sits well above both Victorian averages and national benchmarks. Here's a quick snapshot:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| This Quote | $3,822 | — |

| VIC State | $2,921 | $2,694 |

| National | $2,965 | $2,716 |

The gap between this quote and the state median ($2,694) is over $1,100 per year — enough to make a meaningful difference to a household budget. Whether that premium is justified depends heavily on the specific property characteristics, which we explore below.

---

Property Features That Affect Your Premium

Several features of this property have a direct bearing on what insurers charge. Here's how each one plays into the equation:

Double Brick Construction

Double brick walls are generally viewed favourably by insurers — they're durable, fire-resistant, and less susceptible to wind damage than timber-framed homes. This typically works in your favour when it comes to premiums.

Tiled Roof

A tiled roof is considered a moderate-risk roofing material. Tiles are durable and long-lasting, though they can be more expensive to repair or replace than Colorbond steel. Insurers generally treat tiled roofs as standard.

Slab Foundation

A concrete slab foundation is one of the more stable options available and is unlikely to attract a loading on your premium. It's a neutral-to-positive factor for most insurers.

Solar Panels

This property has solar panels, which adds some complexity to the insurance picture. Solar systems can be expensive to replace and may or may not be covered under a standard building policy — it's worth confirming with your insurer exactly what's included and whether you need additional coverage for the panels and inverter.

Granny Flat

The presence of a granny flat is a notable factor. A secondary dwelling increases the overall rebuild cost and liability exposure, which will push the premium higher. It's important to ensure your sum insured accurately reflects the cost of rebuilding both the main home and the granny flat.

High Building Sum Insured

At $847,000, the building sum insured is the single largest driver of the premium. For a 139 sqm home built in 1985, it's worth periodically reviewing whether this figure is accurate — both underinsurance and overinsurance carry risks. Consider using a professional quantity surveyor or an online building calculator to validate the figure.

Rural Location

Gelliondale's rural setting introduces specific risks, particularly bushfire exposure given its proximity to Gippsland's vegetation. Insurers typically apply loadings for properties in higher bushfire risk zones, which can significantly lift premiums compared to metropolitan averages.

---

Tips for Homeowners in Gelliondale

1. Review Your Sum Insured Carefully

With a building sum insured of $847,000, it's worth confirming this figure is accurate. Overestimating can mean you're paying more in premiums than necessary, while underestimating leaves you exposed in the event of a total loss. Factor in the granny flat when calculating your rebuild cost.

2. Confirm Solar Panel Coverage

Check whether your solar panels are covered under your building policy and to what limit. Some policies include them automatically; others require an endorsement or have sub-limits. Given the cost of solar systems, this is a detail worth clarifying before you need to make a claim.

3. Ask About Bushfire Preparedness Discounts

Some insurers offer reduced premiums for homes with active bushfire mitigation measures — things like cleared vegetation zones, metal mesh on gutters, and ember-proof vents. Given Gelliondale's location in Gippsland, these steps are good practice regardless, but they may also help lower your premium.

4. Compare Multiple Quotes

The most effective way to reduce an above-average premium is simply to compare. Insurers price risk differently, and the gap between the cheapest and most expensive quotes for the same property can be substantial. Don't assume your renewal quote is the best available.

---

Ready to Compare?

If your current premium feels steep, you don't have to accept it. CoverClub makes it easy to compare home and contents insurance quotes from a range of Australian insurers — all in one place. Whether you're insuring a rural property, a home with a granny flat, or simply want to know you're getting a fair deal, get a quote at CoverClub and see how much you could save.