If you own a free standing home in Gheerulla, QLD 4574, you're in one of the Sunshine Coast hinterland's most scenic pockets — but that doesn't mean your home insurance should be anything less than carefully considered. This article breaks down a real home and contents insurance quote for a four-bedroom, four-bathroom property in Gheerulla, compares it against state and national benchmarks, and offers practical tips to help you get the best value cover.

---

Is This Quote Fair?

The annual premium for this property came in at $5,027 per year (or $475/month), covering a building sum insured of $1,594,000 and contents valued at $170,000. Our price rating for this quote is CHEAP — meaning it sits below average for comparable cover.

To put that in perspective:

- The Queensland state average premium is $9,129/yr — this quote is 45% below that figure.

- The national average sits at $5,347/yr — still above this quote by around $320.

- The Gympie LGA average (which covers Gheerulla) is $5,581/yr — again, higher than what's been quoted here.

Given the high sum insured on the building ($1,594,000 is a substantial rebuild value), landing a premium below the state average is a genuinely strong result. Homeowners in Queensland often face elevated premiums due to storm, flood, and cyclone exposure, so a below-average figure here is worth noting.

For a deeper look at how premiums track across the state, visit our Queensland home insurance stats page, or explore national home insurance benchmarks for a broader comparison.

---

How Gheerulla Compares

Suburb-level data for Gheerulla is limited given its small population, but we can draw meaningful context from the Gympie LGA and Queensland state figures.

| Benchmark | Annual Premium |

|---|---|

| This Quote | $5,027 |

| Gympie LGA Average | $5,581 |

| QLD State Average | $9,129 |

| QLD State Median | $3,903 |

| National Average | $5,347 |

| National Median | $2,764 |

A few things stand out here. The QLD state average is dramatically higher than the median ($9,129 vs $3,903), which tells us that a relatively small number of very high-risk or high-value properties are pulling the average upward. This quote, at $5,027, sits comfortably between the state median and average — a reasonable position for a well-built, high-value property in the hinterland.

Compared to the Gympie LGA average of $5,581, this quote is about 10% cheaper, which is a meaningful saving on an ongoing annual cost.

Curious how your suburb stacks up? Check out the Gheerulla insurance stats page for localised data as it becomes available.

---

Property Features That Affect Your Premium

This isn't a standard cookie-cutter home — several features of this property have a direct bearing on the premium quoted.

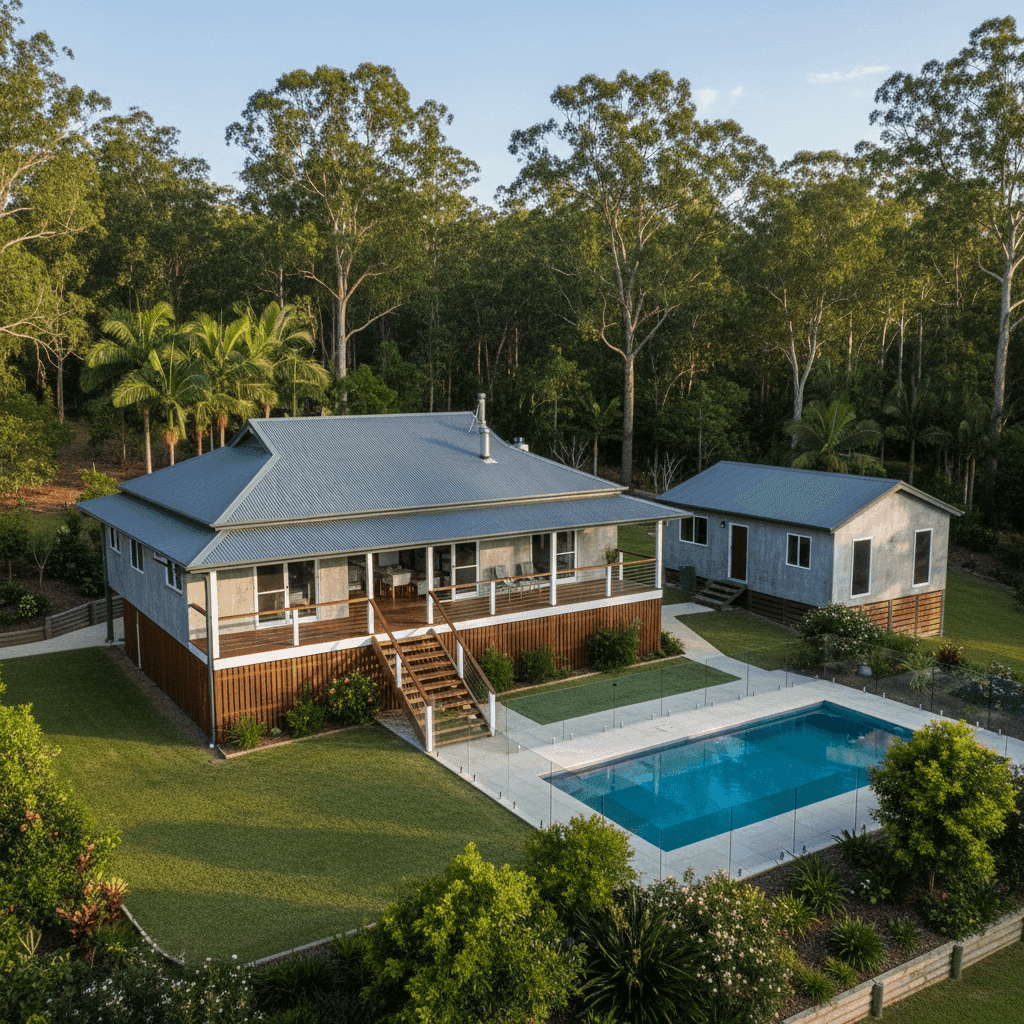

Elevated Construction

The home is elevated by at least one metre, which is a significant positive from an insurer's perspective. Elevated homes are far less susceptible to flood and stormwater inundation, reducing the likelihood of a major claim. In a region like the Sunshine Coast hinterland, where heavy rainfall events are not uncommon, this design feature likely contributes meaningfully to a lower premium.

Concrete Walls and Colorbond Roof

Concrete external walls are among the most resilient construction materials available — they resist fire, wind, and impact damage far better than timber weatherboard. Paired with a steel Colorbond roof (another highly durable material), this home presents a low-risk profile to insurers. These materials are associated with lower rebuild costs relative to their actual strength, which can keep premiums in check.

Slab Foundation

A concrete slab foundation is standard for modern construction and is generally viewed favourably by insurers. It reduces the risk of subsidence or pest-related structural damage that can affect older homes on timber stumps.

Top-of-the-Range Fittings

The property's fittings are rated as top of the range — think high-end kitchen appliances, premium bathroom fixtures, and quality flooring. This does push the rebuild and replacement cost higher, which is reflected in the $1,594,000 sum insured. It's important that this figure accurately reflects what it would cost to fully rebuild the home to the same standard; being underinsured on a premium property is a costly mistake.

Swimming Pool

A pool adds to both the property's value and its insurance complexity. Most policies cover the pool structure under the building component, but it's worth confirming that your policy explicitly includes pool equipment, fencing, and associated structures.

Granny Flat

The presence of a granny flat is an important consideration. Depending on the insurer and policy, a granny flat may or may not be automatically covered under the main home policy. If the flat is rented out — even casually — this can affect your cover, and a separate landlord or contents policy for the occupant may be worth exploring.

Timber and Laminate Flooring

While aesthetically appealing, timber and laminate flooring can be more susceptible to water damage than tiled surfaces. This is worth keeping in mind for both claims awareness and preventative maintenance.

---

Tips for Homeowners in Gheerulla

1. Verify your granny flat is explicitly covered Don't assume your granny flat is included in your standard home policy. Contact your insurer directly and ask for written confirmation of what's covered — including any outbuildings, fencing, and separate structures on the property.

2. Review your sum insured annually With top-of-the-range fittings and a large home, construction costs can shift significantly year to year. Use a building cost calculator or speak with a quantity surveyor to ensure your $1,594,000 sum insured keeps pace with current rebuild costs in the region.

3. Document your contents thoroughly With $170,000 in contents cover, it's worth maintaining a detailed home inventory — photos, receipts, and serial numbers for valuable items. Store this documentation securely off-site or in the cloud so it's accessible if you ever need to make a claim.

4. Ask about discounts for your construction quality Concrete walls and a Colorbond roof are premium risk-reduction features. Some insurers offer explicit discounts for superior construction materials — if yours doesn't proactively apply these, it's worth asking.

---

Ready to Compare?

A below-average premium is a great start, but it's always worth checking whether a better deal exists. Insurance pricing varies significantly between providers, and the right policy isn't just about cost — it's about making sure your cover actually matches your property's unique features.

Get a home insurance quote at CoverClub and see how multiple insurers price your Gheerulla property side by side. It takes just a few minutes and could save you hundreds every year.