If you own a free standing home in Gillieston, VIC 3616, you're likely wondering whether you're paying a fair price for home and contents insurance — or leaving money on the table. This article breaks down a real quote for a four-bedroom, two-bathroom home in Gillieston, compares it against Victorian and national benchmarks, and offers practical tips to help you get the best value cover.

---

Is This Quote Fair?

The annual premium for this property came in at $2,540 per year (or $248/month), covering both building (sum insured: $605,000) and contents ($100,000), each with a $2,000 excess. Our price rating for this quote is CHEAP — below average — which is genuinely good news for the homeowner.

To put that in context: the average home and contents premium across Victoria sits at around $3,000 per year, with a state median of $2,718. This quote beats both figures comfortably. Nationally, the picture is even starker — the Australian average home insurance premium is $5,347 per year, with a national median of $2,764. At $2,540, this Gillieston property is well below both national benchmarks.

For homeowners in regional Victoria, a sub-$2,600 annual premium for a 205 sqm home with a $605,000 building sum insured represents solid value. That said, "cheap" doesn't always mean "right" — it's still worth reviewing what's actually covered and whether the sum insured adequately reflects rebuilding costs in today's market.

---

How Gillieston Compares

Gillieston (VIC 3616) sits within the Greater Shepparton LGA, where the average home insurance premium is $3,296 per year — noticeably higher than both the Victorian state average and this individual quote. That LGA average suggests that some properties in the region attract elevated premiums, potentially due to flood risk, older housing stock, or other local risk factors.

Here's a quick snapshot of how this quote stacks up:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $2,540 |

| VIC State Average | $3,000 |

| VIC State Median | $2,718 |

| Greater Shepparton LGA Average | $3,296 |

| National Average | $5,347 |

| National Median | $2,764 |

This property is tracking $756 below the LGA average and $460 below the Victorian state average. For a more detailed look at how premiums vary across the state, the Victoria insurance stats page is a useful reference point.

---

Property Features That Affect Your Premium

Several characteristics of this particular home play a meaningful role in how insurers price the risk — for better or worse.

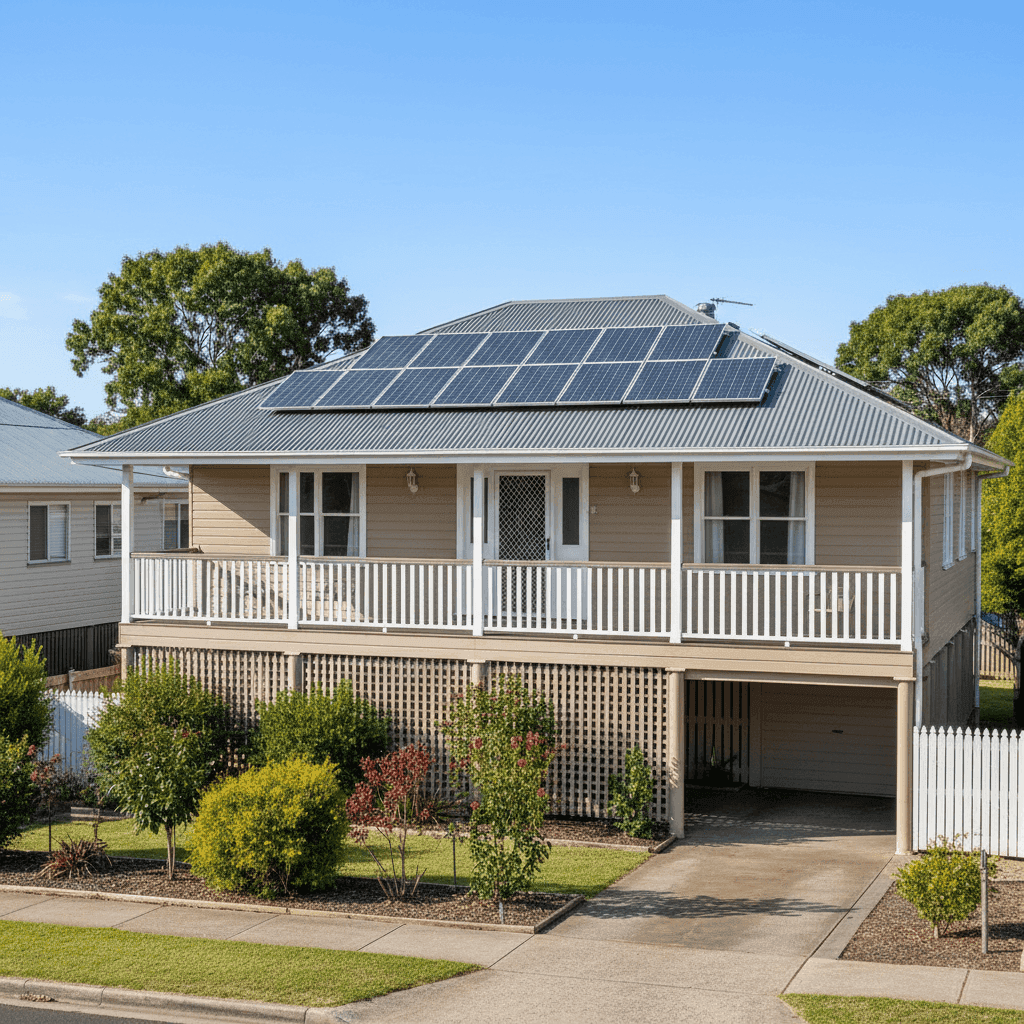

Elevated on Stumps

The home is elevated by at least one metre on a stump foundation. While this style of construction — common in older Victorian homes built in the mid-twentieth century — can actually reduce flood and moisture risk by keeping the floor structure above ground level, it also introduces some complexity around underfloor maintenance and potential storm exposure. On balance, the elevated design may be contributing to a slightly more favourable flood risk assessment.

Hardiplank/Hardiflex Walls with Colorbond Roof

The external walls are Hardiplank Hardiflex, a fibre cement cladding known for its durability and resistance to rot, fire, and moisture. Paired with a steel Colorbond roof, this combination is generally well-regarded by insurers. Colorbond roofing in particular is durable and low-maintenance, which can positively influence premiums compared to older roofing materials like terracotta or ageing iron.

Built in 1956

At nearly 70 years old, this home is considered older stock. Older properties can attract higher premiums due to the likelihood of dated wiring, plumbing, and structural elements that may be more expensive to repair or replace. However, if the home has been well-maintained or renovated, this risk is often mitigated.

Solar Panels

The presence of solar panels adds a modest layer of complexity to a home insurance policy. Panels are typically covered under building insurance, but it's worth confirming with your insurer that they're explicitly included — and at what value. Given rising replacement costs for solar systems, ensuring your sum insured accounts for this is important.

Ducted Climate Control

Ducted climate control is a fixed installation and is generally covered under building insurance. It's a higher-value fitting that contributes to the overall rebuild cost, so it should be factored into your sum insured calculation.

Timber and Laminate Flooring

With timber and laminate flooring throughout, water damage claims can be more costly than with tile floors. This is worth keeping in mind when assessing your contents and building cover limits.

---

Tips for Homeowners in Gillieston

1. Review Your Sum Insured Annually

Building costs have risen sharply across Australia in recent years. A $605,000 sum insured may be appropriate today, but it's worth reassessing each year — particularly for an older home that may require specialist trades for like-for-like repairs. Underinsurance remains one of the most common issues at claim time.

2. Confirm Solar Panel Coverage

Don't assume your solar system is automatically covered. Contact your insurer to confirm panels are listed under your building policy, understand the covered value, and check whether accidental damage to panels is included. With a full rooftop system, replacement costs can easily reach $8,000–$15,000 or more.

3. Check for Flood and Water Damage Cover

Given the Greater Shepparton LGA's higher-than-average premiums — which may partly reflect flood exposure in the broader region — it's worth reviewing whether your policy includes flood cover as standard or as an optional extra. Not all policies treat flood and storm surge the same way.

4. Consider Your Excess Strategy

Both the building and contents excess on this policy sit at $2,000. A higher excess typically lowers your premium, but make sure you can comfortably cover that amount out of pocket in the event of a claim. If cash flow is a concern, a lower excess with a slightly higher premium may offer better peace of mind.

---

Compare and Save with CoverClub

Whether you're renewing your existing policy or shopping around for the first time, comparing quotes is the single most effective way to ensure you're not overpaying. Get a home insurance quote through CoverClub to see how multiple insurers price your specific property — and find out if there's an even better deal available for your Gillieston home.