If you own a free standing home in Gloucester, NSW 2422, you've probably wondered whether you're paying a fair price for home and contents insurance — or whether there's a better deal out there. This article breaks down a real insurance quote for a five-bedroom property in Gloucester, benchmarks it against local, state, and national data, and offers practical tips to help you get the most out of your cover.

---

Is This Quote Fair?

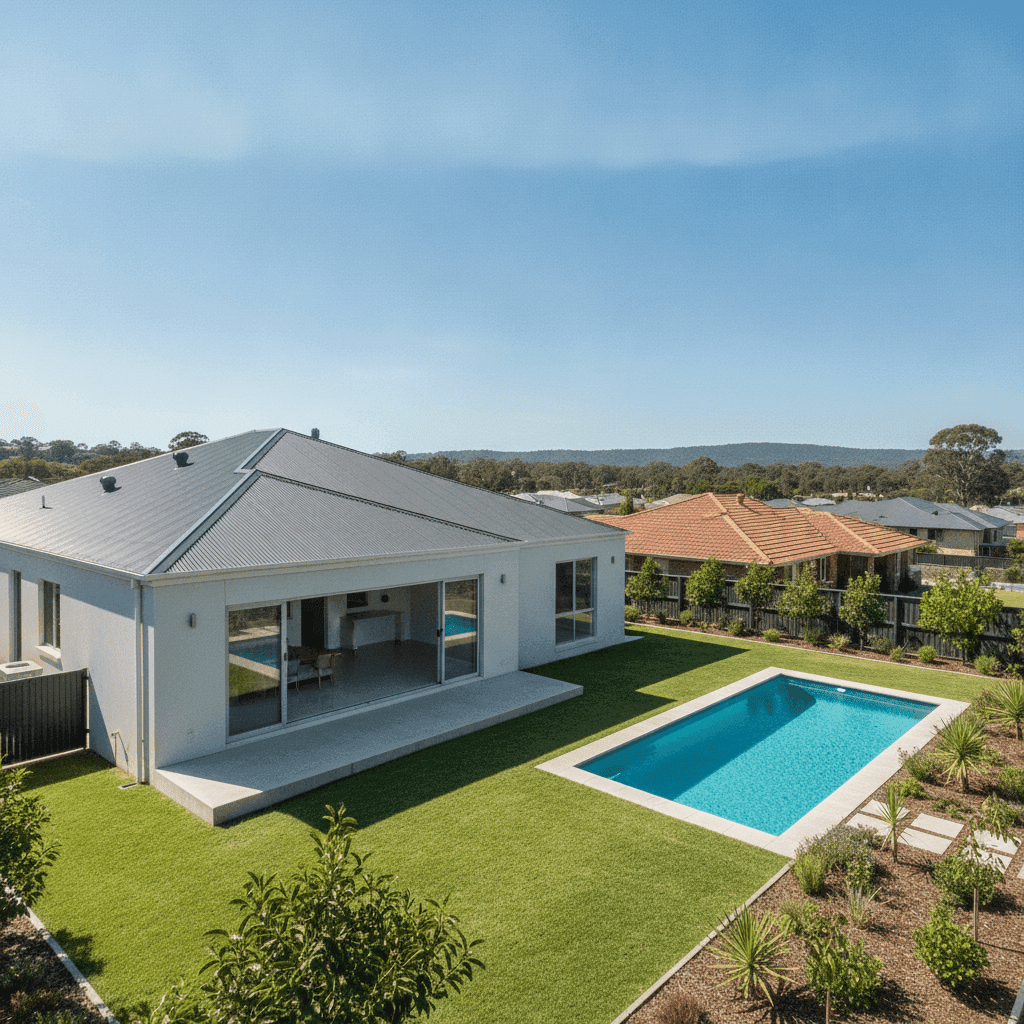

The annual premium for this quote comes in at $3,097 per year (or $311 per month), covering both building and contents. The building is insured for $1,302,000, with contents valued at $50,000. Both the building and contents excess are set at $5,000.

Our pricing engine rates this quote as CHEAP — below average for the area. That's a meaningful finding. Based on Gloucester suburb insurance data, the average premium in this postcode sits at $5,398 per year, with a median of $5,447. That means this homeowner is paying roughly 43% less than the typical Gloucester property owner — a substantial saving of over $2,300 annually.

Even at the lower end of the local market (the 25th percentile sits at $5,031/yr), this quote still comes in well below what most residents in the area are paying. For a five-bedroom home with a pool and ducted climate control, that's genuinely competitive pricing.

---

How Gloucester Compares

To put this quote in proper context, it helps to look beyond the suburb and examine how Gloucester stacks up against the rest of New South Wales and the country.

| Benchmark | Premium |

|---|---|

| This Quote | $3,097/yr |

| Gloucester Suburb Average | $5,398/yr |

| Gloucester Suburb Median | $5,447/yr |

| LGA (Walcha) Average | $2,935/yr |

| NSW Average | $9,528/yr |

| NSW Median | $3,770/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

A few things stand out here. First, the NSW state average of $9,528 is extraordinarily high — this is heavily skewed by expensive metropolitan and coastal markets where flood, storm, and bushfire risk drive premiums up significantly. The NSW median of $3,770 is a far more representative figure for typical homeowners across the state, and this quote sits only slightly above that.

At the national level, the average premium of $5,347 is again pulled upward by high-risk and high-value properties. The national median of $2,764 gives a better sense of what most Australians pay — and at $3,097, this Gloucester quote is in a very reasonable range by that standard.

It's also worth noting that the LGA average (Walcha) is $2,935 — very close to this quote — which suggests the pricing is well-aligned with the broader regional area, even if it sits below the Gloucester suburb average specifically. The suburb sample size of 13 quotes is relatively small, so local averages can shift with a handful of high-value or high-risk properties.

---

Property Features That Affect Your Premium

Several characteristics of this particular home play a role in shaping the premium:

Hebel external walls — Autoclaved aerated concrete (AAC) panels like Hebel are increasingly popular in Australian construction. They're fire-resistant, thermally efficient, and durable, which insurers generally view favourably. This material can contribute to a lower risk profile compared to timber weatherboard.

Steel/Colorbond roof — A Colorbond roof is one of the most insurer-friendly roofing materials available. It's resistant to fire, corrosion, and high winds, and requires minimal maintenance. This is a meaningful positive factor in regional NSW where storm activity can be a concern.

Concrete slab foundation — Slab foundations are considered low-risk by most insurers. They're stable, resistant to termite damage, and don't carry the same vulnerability as elevated timber subfloors.

Tile flooring — Tiles are durable and straightforward to replace after a claim, which can keep replacement cost estimates manageable.

Swimming pool — A pool adds to the overall replacement value of the property and introduces some liability considerations. Homeowners should ensure their policy explicitly covers the pool structure and associated equipment.

Ducted climate control — Ducted systems are expensive to replace if damaged. It's worth confirming this is captured in the building sum insured, as it's typically considered a fixed building fixture.

Elevated less than 1 metre — A slight elevation can assist with drainage and reduce the risk of water ingress during heavy rain events, which is a minor positive from an underwriting perspective.

Construction year: 2003 — At just over two decades old, this home is in a relatively modern bracket. It would have been built to updated building codes, which generally means better structural standards than older homes.

Building size: 214 sqm — At a sum insured of $1,302,000, the implied rebuild cost per square metre is approximately $6,084. This is on the higher end and likely reflects the quality of materials (Hebel, Colorbond) and inclusions like the pool and ducted system. It's worth reviewing this figure periodically to ensure it remains accurate as construction costs fluctuate.

---

Tips for Homeowners in Gloucester

1. Review your sum insured annually Construction costs in regional NSW have risen considerably in recent years. The cost to rebuild your home — including materials, labour, and site preparation — may have changed since your policy was last updated. Underinsurance is one of the most common and costly mistakes homeowners make. Use a building cost calculator or speak to a local builder to sense-check your figure.

2. Check your pool is properly covered If you have a swimming pool, confirm with your insurer that the pool shell, filtration equipment, and any associated structures (like a pool fence or pump housing) are included in your building cover. Some policies treat these as separate items or have specific exclusions.

3. Consider your excess carefully Both the building and contents excess on this policy are set at $5,000. A higher excess typically lowers your premium, but it means you'll need to cover the first $5,000 of any claim yourself. Make sure this amount is genuinely affordable in the event of a sudden loss.

4. Compare quotes before renewal Even if your current premium is competitive, it's worth comparing quotes at renewal time. Insurers adjust their pricing models regularly, and what's cheap today may not be the best value next year. Get a fresh quote at CoverClub to see how your current policy stacks up.

---

Compare Your Home Insurance Today

Whether you're a Gloucester local or simply researching home insurance in regional NSW, CoverClub makes it easy to benchmark your premium against real market data. Start comparing quotes now and find out whether you're getting a fair deal — or leaving money on the table. You can also explore detailed Gloucester suburb insurance statistics to see how your property compares to others in the area.