If you own a free standing home in Goondiwindi, QLD 4390, you've probably noticed that home insurance doesn't come cheap in this part of regional Queensland. This article breaks down a real home and contents insurance quote for a three-bedroom, two-bathroom weatherboard home in the area — and puts the numbers into context so you can judge whether you're getting a fair deal.

---

Is This Quote Fair?

The quote in question comes in at $9,019 per year (or $880/month), covering both building (sum insured: $790,000) and contents ($150,000). The building excess is $3,000 and the contents excess is $600.

Our price rating for this quote is Expensive (Above Average) — and the data backs that up.

Compared to the suburb average for Goondiwindi of $7,052/yr, this quote sits roughly 28% above what most locals are paying. It also clears the suburb's 75th percentile benchmark of $8,342/yr, meaning it's more expensive than at least three-quarters of quotes we've seen for this postcode. That's a meaningful gap — and worth investigating before you simply accept the renewal figure.

That said, context matters. The suburb median sits at $5,730/yr, which suggests a wide spread of premiums across Goondiwindi. Some homeowners are paying as little as $3,522/yr (the 25th percentile), while others at the top end are paying well above $8,000. This quote falls firmly in that upper tier.

---

How Goondiwindi Compares

To understand why premiums in Goondiwindi are elevated, it helps to zoom out and look at the broader picture.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Goondiwindi (LGA) | $6,634/yr | — |

| Goondiwindi (suburb) | $7,052/yr | $5,730/yr |

| Queensland | $4,547/yr | $3,931/yr |

| National | $2,965/yr | $2,716/yr |

The Queensland state average of $4,547/yr is already well above the national average of $2,965/yr — a reflection of the elevated weather and climate risks that affect much of the Sunshine State. Goondiwindi's suburb average of $7,052/yr sits 55% above the Queensland average, which tells you that local risk factors are pushing premiums significantly higher than the state norm.

Much of this comes down to geography. Goondiwindi sits on the Macintyre River near the NSW border, and the region has a well-documented history of flooding. Flood risk is one of the most significant premium drivers in Australia, and insurers price it accordingly. Even without cyclone risk (this property is outside cyclone-affected zones), flood and storm exposure in inland Queensland can push premiums into the same territory as coastal properties.

---

Property Features That Affect Your Premium

Several characteristics of this particular home contribute to its insurance cost — some upward, some potentially downward.

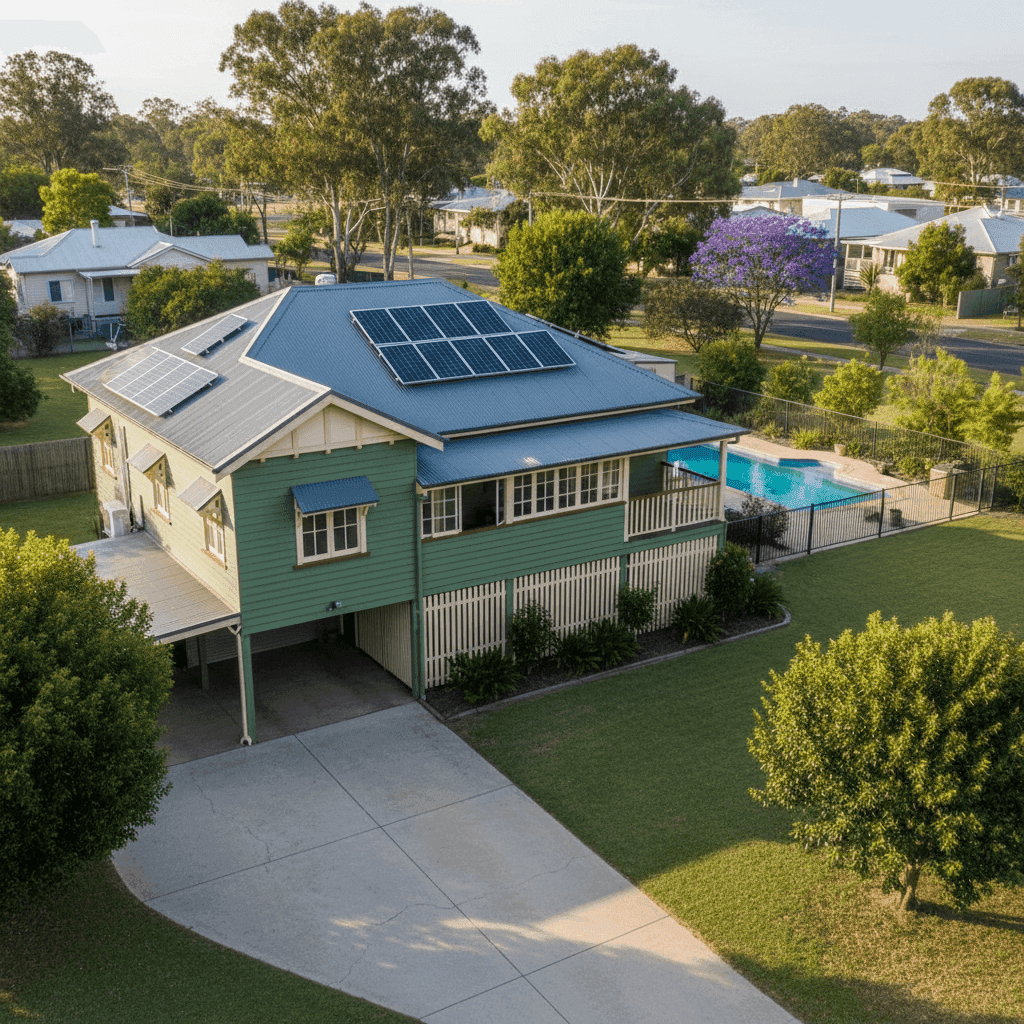

Weatherboard timber construction is one of the most influential factors. Older timber-framed homes are considered higher risk by insurers due to their susceptibility to fire, termite damage, and general wear over time. This home was built in 1953, making it over 70 years old — a factor that insurers weigh carefully when calculating rebuild risk and the likelihood of claims.

Stumped foundations are common in older Queensland homes and, while they allow for airflow and can reduce flood damage compared to slab-on-ground, they also introduce structural considerations that some insurers factor into their pricing.

Timber and laminate flooring can be more vulnerable to water damage than tiled alternatives, which may influence contents and building assessments alike.

On the other hand, a Colorbond steel roof is generally viewed favourably by insurers. It's durable, fire-resistant, and performs well in high-wind and hail events — which are not uncommon in southern Queensland. This could be moderating the premium to some degree.

The above-average fittings quality is reflected in the relatively high building sum insured of $790,000 for a 139 sqm home. Quality fixtures, joinery, and finishes cost more to replace, and insurers price accordingly. It's worth ensuring your sum insured accurately reflects current rebuild costs — neither over- nor under-insured.

Solar panels add replacement value to the property and are typically covered under the building policy, but they do represent an additional asset that contributes to the overall insured value. Similarly, a swimming pool adds liability and replacement cost considerations to the policy.

---

Tips for Homeowners in Goondiwindi

1. Shop around — seriously. With a sample of 57 quotes in this postcode showing a spread from $3,522 to well above $8,000, there is clearly significant variation between insurers. The same property can attract very different premiums depending on how each insurer models local flood risk, construction type, and age. Comparing multiple quotes through a platform like CoverClub takes minutes and could save you thousands annually.

2. Review your sum insured carefully. A building sum insured of $790,000 for a 139 sqm weatherboard home is substantial. Make sure this figure reflects a genuine current rebuild cost — factoring in demolition, materials, labour, and professional fees — rather than the market value of the land and property combined. Overinsuring inflates your premium without adding real benefit; underinsuring can leave you exposed at claim time.

3. Ask about flood cover inclusions and exclusions. In a region like Goondiwindi with documented flood history, understanding exactly what your policy covers is critical. Some policies include flood as standard; others offer it as an optional add-on or exclude it entirely. Read the Product Disclosure Statement (PDS) carefully and confirm whether riverine flooding, flash flooding, and storm surge are all covered.

4. Consider your excess settings. This quote carries a $3,000 building excess, which is on the higher side. Accepting a higher excess is one way to reduce your annual premium, but make sure the excess level is something you could genuinely afford to pay in the event of a claim. If $3,000 would be a financial stretch, it may be worth paying a slightly higher premium for a lower excess.

---

Compare Home Insurance Quotes in Goondiwindi

Whether this quote is right for your situation depends on your property, your risk tolerance, and what's available in the market right now. The best way to find out is to compare. At CoverClub, we make it easy to see how multiple insurers price your specific home — so you're not just accepting the first number you're given.

Get a home insurance quote for your Goondiwindi property →

You can also explore detailed suburb-level insurance statistics for Goondiwindi (QLD 4390) to see how your premium stacks up against your neighbours.