If you own a free standing home in Goonellabah, NSW 2480, you're probably no stranger to the sting of insurance renewal time. Goonellabah sits in the hinterland behind Lismore in the Northern Rivers region — a lush, leafy suburb that comes with its own set of risk considerations for insurers. This article breaks down a real home and contents insurance quote for a five-bedroom property in the area, puts the price in context, and gives you practical tips to make sure you're not paying more than you should.

---

Is This Quote Fair?

The quote in question comes in at $3,802 per year (or $358/month) for a combined home and contents policy. The building is insured for $1,410,000 with contents valued at $151,000, and both the building and contents excesses are set at $5,000.

Our price rating for this quote is Expensive (Above Average) — and the data backs that up.

When we compare this premium against the 73 quotes we've collected for the Goonellabah area, this policy sits well above the suburb average of $2,173/yr and the median of $2,124/yr. In fact, it's even above the 75th percentile of $2,628/yr, meaning it's pricier than at least three-quarters of comparable quotes in the suburb.

That said, context matters. The $1,410,000 building sum insured is a significant figure — larger homes with higher replacement values will always attract higher premiums. A 367 sqm five-bedroom, three-bathroom property with above-average fittings is not a standard suburban home, and the insured amount reflects that. Still, even accounting for the size and value, it's worth shopping around to ensure the rate itself is competitive.

---

How Goonellabah Compares

Understanding where your suburb sits within the broader insurance landscape is one of the most useful tools a homeowner has. Here's how Goonellabah stacks up:

| Benchmark | Premium |

|---|---|

| Goonellabah suburb average | $2,173/yr |

| Goonellabah suburb median | $2,124/yr |

| NSW state average | $9,528/yr |

| NSW state median | $3,770/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

| Ballina LGA average | $23,241/yr |

A few things stand out here. The NSW state average of $9,528/yr is dramatically higher than Goonellabah's suburb average — largely because NSW includes coastal and flood-prone areas that push premiums sky-high. The Ballina LGA average of $23,241/yr is a striking example of this: properties closer to the coast and flood plains in the Ballina council area carry enormous risk loadings.

Goonellabah, by comparison, benefits from its elevated hinterland position, which generally reduces flood risk relative to low-lying parts of the region. Compared to the national average of $5,347/yr, this suburb is actually quite affordable on a per-policy basis — though the quote in question, at $3,802, still sits above the suburb norm.

---

Property Features That Affect Your Premium

Several characteristics of this property will be influencing the final premium figure. Here's what insurers are likely factoring in:

Size and Sum Insured

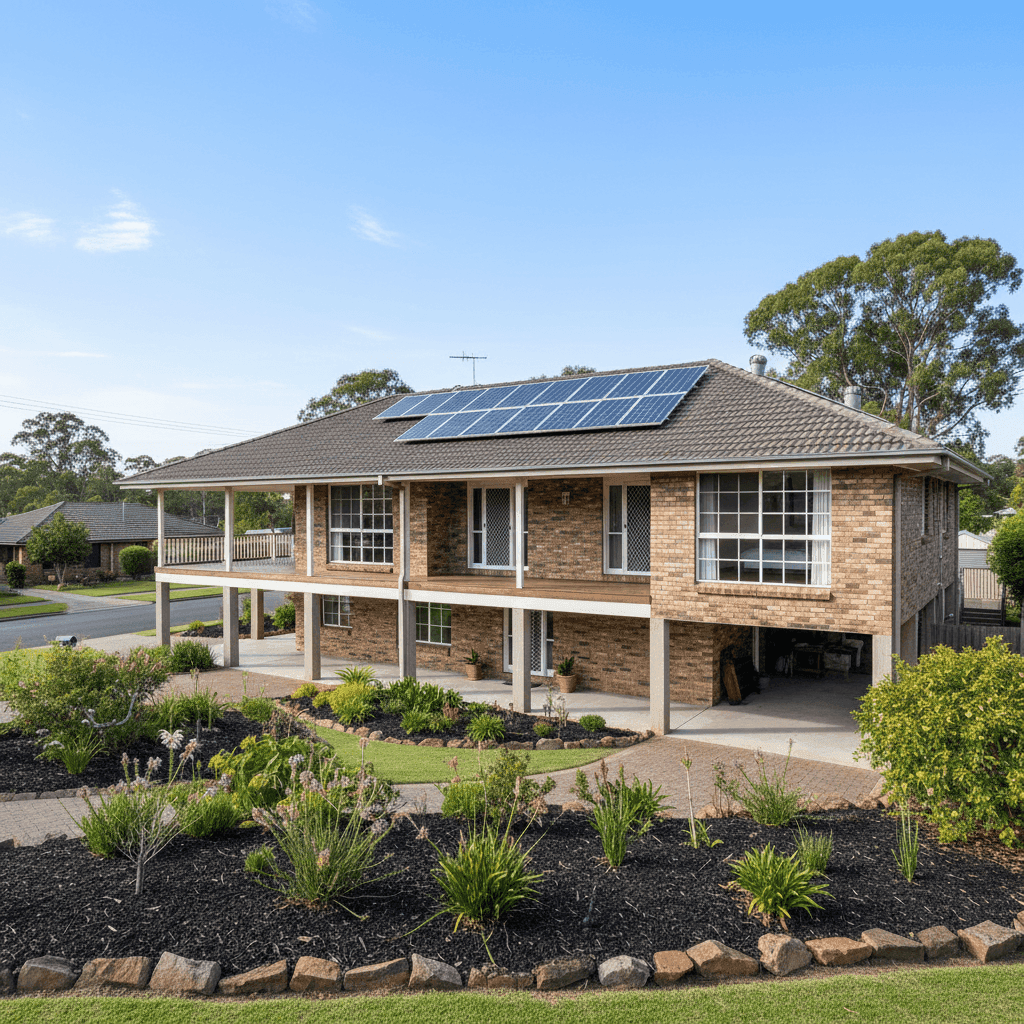

At 367 sqm with a $1,410,000 building sum insured, this is a large home with a high replacement cost. Rebuild costs in regional NSW have climbed significantly in recent years due to labour shortages and material price increases — so a high sum insured is prudent, but it does mean a higher base premium.

Brick Veneer Walls and Tiled Roof

Brick veneer construction is generally viewed favourably by insurers. It offers solid fire resistance and structural durability compared to weatherboard or fibre cement. Combined with a tiled roof, this property presents a relatively low-risk profile from a construction standpoint.

Stump Foundation and Elevation

The home sits on stumps, elevated by less than one metre. Stump foundations are common in the Northern Rivers region and can actually be beneficial — they allow airflow beneath the home and provide some buffer against minor surface water. However, insurers may view them with slightly more scrutiny depending on their flood and storm modelling for the area.

Solar Panels

The presence of solar panels is worth noting. Some insurers include solar systems under building cover automatically, while others treat them as a separate item or require explicit inclusion. It's important to confirm with your insurer that your solar installation is fully covered under the building sum insured.

Above-Average Fittings

Above-average fittings — think stone benchtops, quality appliances, premium fixtures — increase the cost to rebuild or repair, and insurers price accordingly. This is a legitimate driver of a higher premium and one that should be reflected in an accurate sum insured.

Contents Value

A $151,000 contents value is reasonable for a five-bedroom home with quality fittings. Underinsuring contents is a common mistake — make sure your estimate includes furniture, electronics, clothing, white goods, and any high-value items like jewellery or artwork that may need to be separately listed.

---

Tips for Homeowners in Goonellabah

1. Review your sum insured regularly Building costs in regional NSW have risen sharply. Use an independent building cost calculator to check whether your sum insured still reflects the true cost to rebuild — not just the market value of your home. Underinsurance is one of the most common and costly mistakes homeowners make.

2. Confirm solar panel coverage With solar panels on the roof, check the fine print of any policy you consider. Ask specifically: are the panels covered under the building sum insured? What about damage from storms or hail? Some policies exclude inverters or limit coverage — know what you're signing up for.

3. Shop around — especially given the suburb's price spread The gap between the 25th percentile ($1,526/yr) and the 75th percentile ($2,628/yr) in Goonellabah is significant. That range shows that different insurers price this suburb very differently. A quote that's above the 75th percentile is a clear signal to compare alternatives.

4. Consider your excess strategically Both the building and contents excesses on this quote are set at $5,000. Higher excesses typically reduce your premium — but make sure you could comfortably cover that amount out of pocket in the event of a claim. If $5,000 feels too high, explore what a lower excess would cost in premium terms.

---

Compare Your Options with CoverClub

Whether this quote is your first or your fifth, the best way to know if you're getting a fair deal is to compare. CoverClub aggregates real insurance data from across Australia to help homeowners in suburbs like Goonellabah make informed decisions — not just go with the first renewal notice that lands in their inbox.

Get a home insurance quote today and see how your premium stacks up against your neighbours. You might be surprised at what you could save.