If you own a free standing home in Gormandale, VIC 3873, you're likely no stranger to the realities of insuring a regional Victorian property. Gormandale is a small town in the Wellington local government area of Gippsland — a region with its own unique mix of environmental and structural risk factors that insurers pay close attention to. This article breaks down a recent home and contents insurance quote for a six-bedroom weatherboard home in the area, compares it against local, state, and national benchmarks, and offers practical advice for homeowners looking to get better value on their cover.

---

Is This Quote Fair?

The quote in question came in at $7,832 per year (or $770/month) for combined home and contents insurance, covering a building sum insured of $678,000 and contents valued at $50,000. The building excess is set at $3,000, with a $1,000 excess on contents.

Our price rating for this quote is Expensive — Above Average.

To put that in perspective, the suburb average premium in Gormandale sits at just $2,806 per year, and the median is $2,803. That means this particular quote is nearly 2.8 times the local average — a significant gap that warrants a closer look.

Even allowing for the upper end of the local price range (the 75th percentile sits at $3,449/yr), this quote still exceeds that figure by more than $4,300 annually. For a homeowner on a budget, that's a meaningful difference.

It's worth noting that the suburb sample size used in this comparison is six quotes, which is a relatively small dataset. Results may shift as more data comes in — but the gap here is large enough to be considered genuinely significant regardless.

---

How Gormandale Compares

Here's how this quote stacks up against broader benchmarks:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Gormandale (suburb) | $2,806/yr | $2,803/yr |

| Wellington LGA | $2,836/yr | — |

| Victoria (state) | $2,921/yr | $2,694/yr |

| National | $2,965/yr | $2,716/yr |

| This quote | $7,832/yr | — |

Across every benchmark — suburb, state, and national — this quote lands well above average. Interestingly, Gormandale's average premium is actually slightly below the Victorian and national averages, suggesting the area itself isn't considered especially high-risk by most insurers. That makes the elevated cost of this particular quote even more notable, and points to property-specific factors driving the price up rather than location alone.

---

Property Features That Affect Your Premium

Several characteristics of this property are likely contributing to the higher-than-average premium. Here's what insurers typically flag:

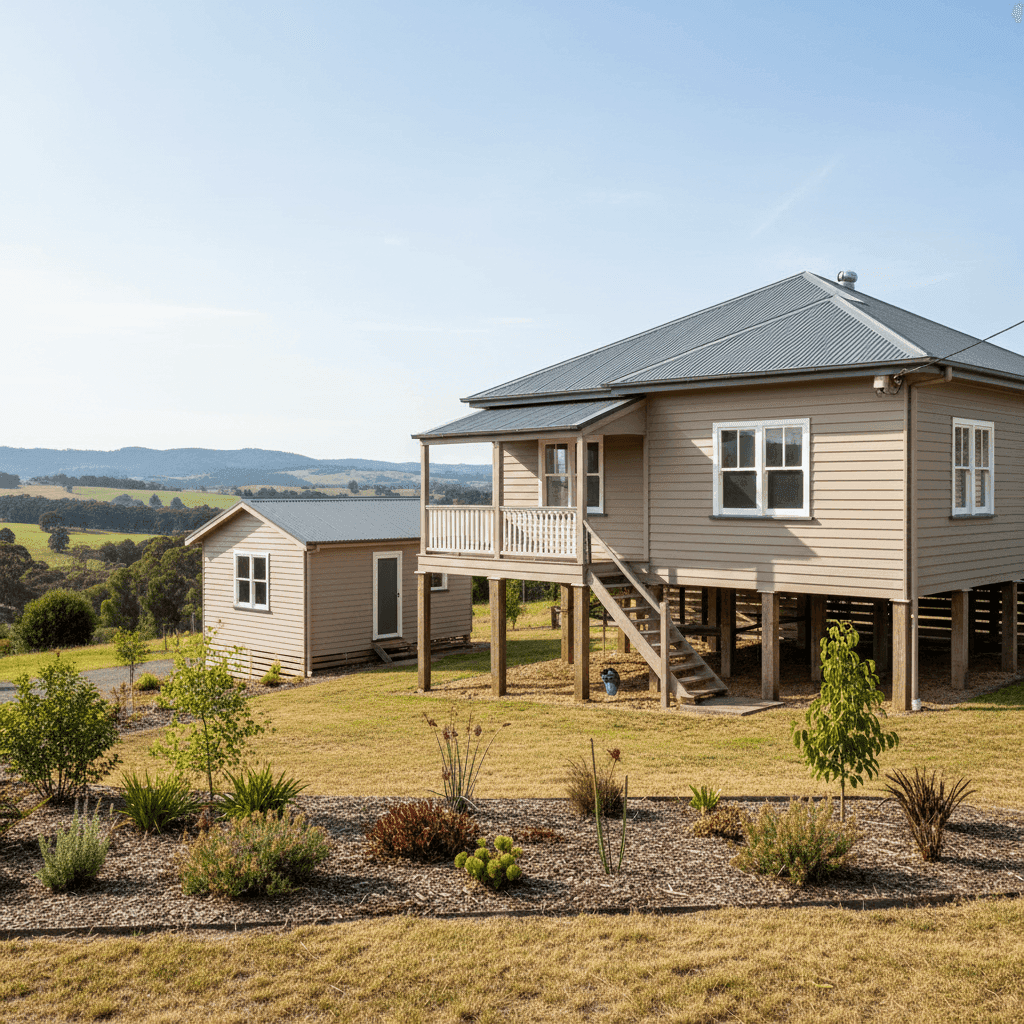

Weatherboard Timber Construction

Weatherboard wood external walls are one of the most significant cost drivers in home insurance. Timber homes are considered higher risk than brick veneer or full brick constructions — they're more susceptible to fire damage, pest ingress, and general wear over time. Rebuilding costs for weatherboard homes can also be higher per square metre, which directly influences the sum insured calculation.

Stump Foundation

Homes built on stumps (also known as pier foundations) are elevated off the ground, which can be both a benefit and a risk factor. While elevation can reduce flood exposure in some scenarios, stump foundations require ongoing maintenance and can be more costly to repair or replace. Insurers may price this in accordingly.

Timber and Laminate Flooring

Combined with the stump foundation, timber and laminate flooring adds to the overall rebuild cost estimate. These materials are more expensive to replace than concrete slab floors, and their presence throughout a 130 sqm home adds up quickly.

Granny Flat on the Property

The inclusion of a granny flat is a notable factor. Additional structures on the property increase the total replacement value and can complicate claims assessments. Depending on the insurer, a granny flat may be covered under the main building policy or require separate endorsement — either way, it typically adds to the overall premium.

Building Age and Size

Constructed in 1993, this home is over 30 years old. Older properties often carry higher premiums due to the potential for outdated wiring, plumbing, and structural components that may be more expensive or complex to repair. At 130 sqm with six bedrooms and two bathrooms, the layout is relatively compact for its bedroom count, but the sum insured of $678,000 reflects the full cost of rebuilding — not just the market value.

Ducted Climate Control

Ducted systems are a significant fixed asset within the home. Their inclusion in the building sum insured increases the overall replacement cost and is a legitimate driver of a higher premium.

---

Tips for Homeowners in Gormandale

If you're looking to reduce your premium or ensure you're getting fair value, here are four practical steps worth taking:

- Shop around and compare multiple quotes. This is the single most effective way to reduce your insurance costs. Premiums for the same property can vary enormously between insurers — sometimes by thousands of dollars. Use a comparison platform like CoverClub to see multiple options side by side.

- Review your sum insured carefully. Over-insuring is a common and costly mistake. Make sure your building sum insured reflects the actual cost to rebuild — not the market value of your property. A quantity surveyor or online rebuild calculator can help you arrive at a more accurate figure.

- Consider a higher excess to lower your premium. The building excess on this quote is already set at $3,000, which is on the higher side. However, if you're comfortable taking on more risk in the event of a claim, some insurers will offer meaningful discounts for even higher excess levels.

- Ask about bundling and loyalty discounts. Some insurers offer discounts when you combine home and contents cover, or when you've been a customer for a number of years. It's always worth asking — but don't let a loyalty discount stop you from switching if a competitor is offering significantly better value.

---

Ready to Find a Better Deal?

If this quote doesn't feel right for your situation, you're not stuck with it. At CoverClub, we make it easy to compare home and contents insurance quotes from a range of Australian insurers — so you can see exactly where your money is going and whether you're paying a fair price.