If you own a free standing home in Gorokan, NSW 2263, on the Central Coast, you're likely paying close attention to rising insurance costs. This article breaks down a real home and contents insurance quote for a 3-bedroom, 3-bathroom brick veneer property in the suburb — and puts it into context against local, state, and national benchmarks. Whether you're shopping around or reviewing your existing policy, understanding what's driving your premium is the first step to making a smarter decision.

---

Is This Quote Fair?

The quote in question comes in at $2,869 per year (or $275/month) for combined home and contents cover, with a building sum insured of $594,000 and contents valued at $104,000. Both the building and contents excess are set at $1,000.

Our analysis rates this quote as Expensive — above average for the Gorokan area.

To put that in perspective, the suburb average premium sits at $1,903/yr, and the median is even lower at $1,556/yr. This quote lands well above the 75th percentile for the suburb ($2,538/yr), meaning it's pricier than roughly three-quarters of comparable quotes we've seen in the area. That's a meaningful gap — and one worth investigating before simply renewing.

That said, it's important to note that this quote covers a relatively high building sum insured ($594,000), which will naturally push the premium upward compared to properties insured for less. The inclusion of contents cover ($104,000) also adds to the total cost. These factors alone won't fully explain the premium, but they're part of the picture.

---

How Gorokan Compares

Zooming out beyond the suburb gives a broader sense of where Gorokan sits in the wider insurance landscape. You can explore the full Gorokan suburb insurance stats or browse NSW state-wide data for more context.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Gorokan (NSW 2263) | $1,903/yr | $1,556/yr |

| Central Coast LGA | $8,387/yr | — |

| NSW State-wide | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

At first glance, the Central Coast LGA and NSW state averages look alarmingly high — but these figures are heavily skewed by high-value properties and extreme weather-affected areas across the state. The median is usually a more reliable comparison point for typical homeowners. Against the national median of $2,764/yr, this quote of $2,869/yr is only modestly above average — which is a more reassuring picture.

You can explore national home insurance benchmarks to see how your postcode stacks up across Australia.

---

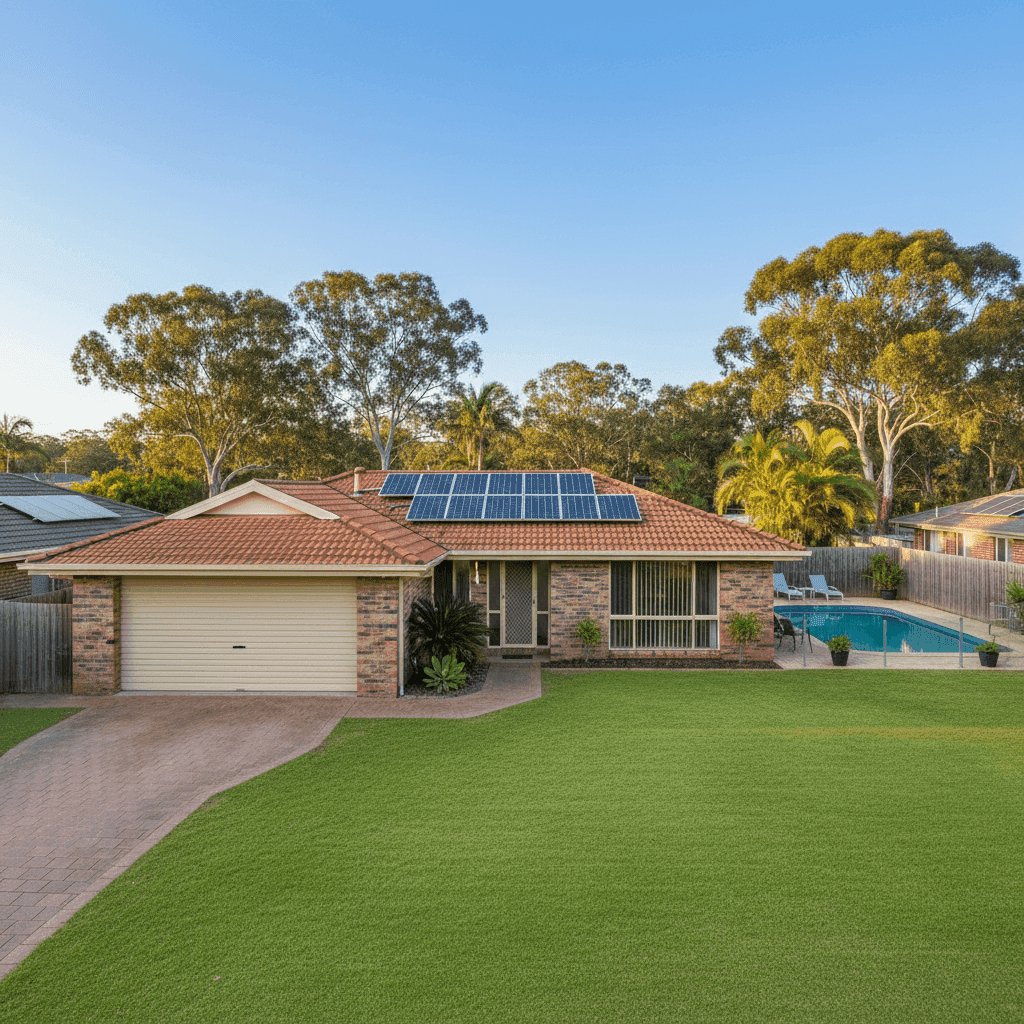

Property Features That Affect Your Premium

Several characteristics of this property are likely influencing the premium — some favourably, others less so.

Brick Veneer Walls & Tiled Roof

Brick veneer construction with a tiled roof is generally viewed positively by insurers. These materials are durable, fire-resistant, and relatively cost-effective to repair compared to weatherboard or Colorbond alternatives. This combination typically attracts more competitive premiums.

Slab Foundation

A concrete slab foundation is standard for homes of this era and construction type on the Central Coast. It's generally considered lower risk than pier-and-beam foundations, which can be more susceptible to movement and water ingress.

Construction Year: 1985

Homes built in the mid-1980s are well past the point of early construction defects but may be approaching the age where electrical wiring, plumbing, and roofing materials start to require attention. Insurers may factor in this age when pricing the risk of claims related to wear and tear or building services failure.

Swimming Pool

The presence of a pool adds liability exposure to your policy. Pools increase the risk of personal injury claims, and insurers factor this into their pricing. Ensuring your pool complies with NSW fencing and safety regulations is essential — both legally and for your insurance standing.

Solar Panels

Solar panels are increasingly common on Australian homes, but they do add complexity to a claim. Panels can be damaged by hail, storms, or fire, and replacing them can be costly. Make sure your policy explicitly covers solar panels as part of the building sum insured.

Ducted Climate Control

Ducted air conditioning systems are expensive to repair or replace, and their presence can contribute to a higher building sum insured — which is likely a factor in the $594,000 valuation here. Ensuring this is accurately reflected in your cover is important to avoid being underinsured.

Building Size: 139 sqm

At 139 sqm, this is a modest-sized home for a 3-bedroom, 3-bathroom layout. The relatively high sum insured ($594,000) compared to the floor area may reflect the cost of quality fittings, inclusions like the pool and solar system, and current construction costs in the Central Coast region.

---

Tips for Homeowners in Gorokan

1. Shop Around — Seriously

With this quote sitting above the suburb's 75th percentile, there's a real chance a comparable policy is available at a lower price. Use a comparison tool like CoverClub to see multiple quotes side by side without the legwork.

2. Review Your Sum Insured Carefully

A building sum insured of $594,000 is substantial. Make sure it reflects the actual cost to rebuild your home from scratch — not its market value. Overinsuring inflates your premium without added benefit, while underinsuring leaves you exposed. Consider using a building cost calculator or speaking with a quantity surveyor if you're unsure.

3. Consider a Higher Excess

Both the building and contents excess are set at $1,000. Opting for a higher voluntary excess — say $2,000 or $2,500 — can meaningfully reduce your annual premium. This strategy works well if you have the financial buffer to cover a larger out-of-pocket cost in the event of a claim.

4. Check Your Pool and Solar Are Properly Covered

Don't assume these features are automatically included under your building cover. Review your policy's Product Disclosure Statement (PDS) to confirm that your pool, pool equipment, and solar panel system are explicitly listed as covered items. Gaps here can be costly at claim time.

---

Ready to Compare?

If this quote has you wondering whether you're getting value for money, it's worth taking a few minutes to explore your options. At CoverClub, we make it easy to compare home and contents insurance quotes for Gorokan and across Australia — so you can find cover that fits both your property and your budget.

Get a home insurance quote today and see how much you could save.