Grasmere is a semi-rural suburb tucked into the Wollondilly local government area on Sydney's south-western fringe — the kind of place where generous land parcels, established gardens, and spacious family homes are the norm rather than the exception. If you own a five-bedroom free-standing home here, you're sitting on a substantial asset, and making sure it's properly protected is no small matter. This article unpacks a recent building insurance quote of $2,495 per year (or $232/month) for exactly that type of property, and explains what's driving the price — and whether it's a good deal.

---

Is This Quote Fair?

The short answer: yes, and then some. Our pricing model rates this quote as CHEAP — below the suburb average — and the numbers back that up convincingly.

At $2,495 annually, this premium sits well below the Grasmere suburb average of $5,452/yr and even further beneath the suburb median of $6,321/yr. To put it in sharper relief, the 25th percentile of quotes in the area — meaning only a quarter of homeowners are paying less — sits at $3,389/yr. This quote beats even that benchmark by nearly $900.

That's a meaningful saving. Over five years, paying $2,495 instead of the suburb average of $5,452 would keep roughly $14,785 in your pocket, assuming premiums held steady.

The building excess is set at $5,000, which is on the higher side and is likely one of the levers pulling the premium down. A higher excess means you absorb more of the cost in a small-to-medium claim, so insurers reward that risk-sharing with a lower annual cost. It's a trade-off worth understanding before you commit.

---

How Grasmere Compares

To get a full picture of where this quote lands, it helps to zoom out and look at the broader market. Here's a snapshot:

| Benchmark | Premium |

|---|---|

| This quote | $2,495/yr |

| Grasmere suburb average | $5,452/yr |

| Grasmere suburb median | $6,321/yr |

| Grasmere 25th percentile | $3,389/yr |

| LGA (Wollondilly) average | $2,297/yr |

| NSW state average | $9,528/yr |

| NSW state median | $3,770/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

(Based on 25 quotes collected for the Grasmere area. [View full suburb stats →](https://coverclub.com.au/stats/NSW/2570/grasmere))

A few things stand out here. The NSW state average of $9,528/yr is extraordinarily high compared to the median of $3,770/yr — a classic sign that a relatively small number of very expensive properties (or high-risk locations) are skewing the mean upward. Grasmere's suburb average of $5,452/yr is similarly elevated compared to its median, suggesting the same dynamic is at play locally.

The national median of $2,764/yr is the most useful national reference point for a typical home, and this quote at $2,495/yr sits just beneath it — a solid result for a large, five-bedroom property with a pool, solar panels, and a granny flat.

The Wollondilly LGA average of $2,297/yr is the closest comparator geographically, and this quote tracks closely to that figure, suggesting local risk factors are being priced appropriately.

---

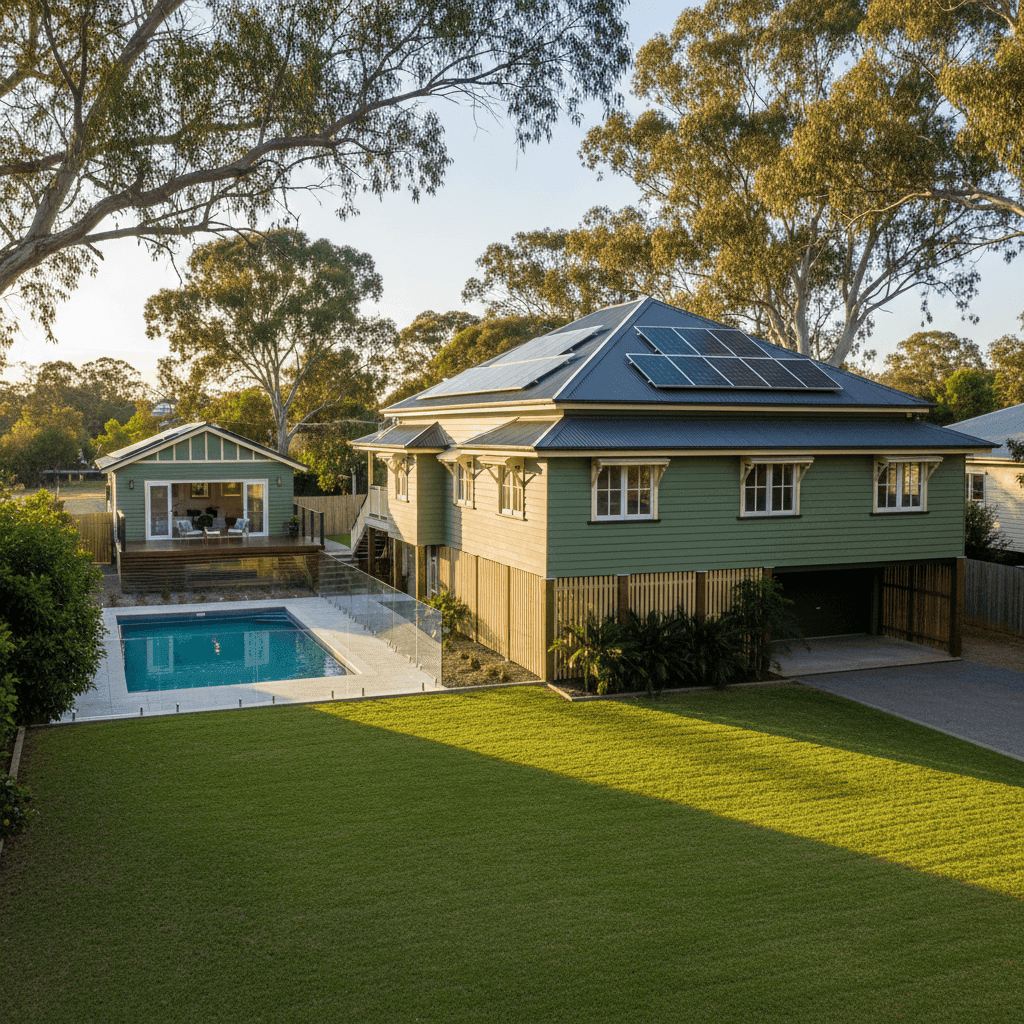

Property Features That Affect Your Premium

Every home tells its own story to an insurer's risk model. Here's how the specific features of this property likely influence the premium:

Weatherboard timber walls are one of the most significant rating factors. Timber is more susceptible to fire and pest damage than brick veneer or double brick, which typically pushes premiums higher. The fact this quote remains competitive despite weatherboard construction is notable.

Steel/Colorbond roof is generally viewed favourably by insurers. Colorbond is durable, fire-resistant, and performs well in high-wind events — a meaningful contrast to older terracotta or asbestos-cement roofing materials that can be costly to replace.

Stump foundations with elevation under 1 metre introduce some complexity. Elevated homes on stumps can be more vulnerable to subfloor damage from moisture, pests, and wind uplift. However, the sub-1m elevation means it doesn't attract the steeper loadings sometimes applied to fully elevated Queenslander-style homes.

The swimming pool adds replacement cost to the sum insured and may attract a small loading for liability considerations, though its impact on a building-only policy is primarily about the rebuild cost.

Solar panels are increasingly common in Grasmere and across greater Sydney. They add to the sum insured — panels, inverters, and mounting hardware can cost $8,000–$20,000 to replace — and insurers factor this into the building calculation.

The granny flat is a significant inclusion. A secondary dwelling adds considerable rebuild cost, and ensuring it's captured within the $750,000 sum insured is essential. Underinsurance is a genuine risk when ancillary structures aren't properly accounted for.

Ducted climate control is another high-value fixed asset. Ducted systems can cost $10,000–$25,000 to replace and are typically covered under building insurance as a permanently installed fixture.

The property was built in 1979, which means it predates several modern building codes. This can affect the cost of reinstatement if a claim requires bringing the home up to current standards — something worth discussing with your insurer.

---

Tips for Homeowners in Grasmere

1. Review your sum insured carefully — especially with a granny flat A $750,000 sum insured for a 286 sqm home plus a granny flat, pool, solar system, and ducted air conditioning is worth scrutinising. Use a building cost calculator or speak to a quantity surveyor to make sure you're not underinsured. The cost to rebuild (not the market value) is what matters here.

2. Understand the impact of your $5,000 excess A high excess is a legitimate way to reduce your premium, but make sure you could comfortably cover that amount out of pocket if you needed to make a claim. If $5,000 would be a stretch, consider whether a lower excess — and slightly higher premium — is the more prudent choice.

3. Maintain your weatherboard cladding proactively Timber weatherboard requires regular painting, sealing, and inspection for rot or termite activity. Insurers can deny or reduce claims where damage is attributable to poor maintenance rather than a sudden insured event. Staying on top of upkeep protects both your home and your claim entitlements.

4. Shop the market at renewal time Even a competitive premium like this one should be tested at renewal. Insurers often apply "loyalty loading" to long-standing customers, and the market moves. Comparing quotes annually through a platform like CoverClub takes minutes and could surface a materially better deal — or simply confirm you're already well-placed.

---

Compare Your Own Quote

Whether you're renewing your existing policy or insuring a Grasmere property for the first time, it pays to see the full picture. CoverClub aggregates real quote data from across Australia so you can benchmark your premium against what your neighbours are actually paying — not just advertised rates.