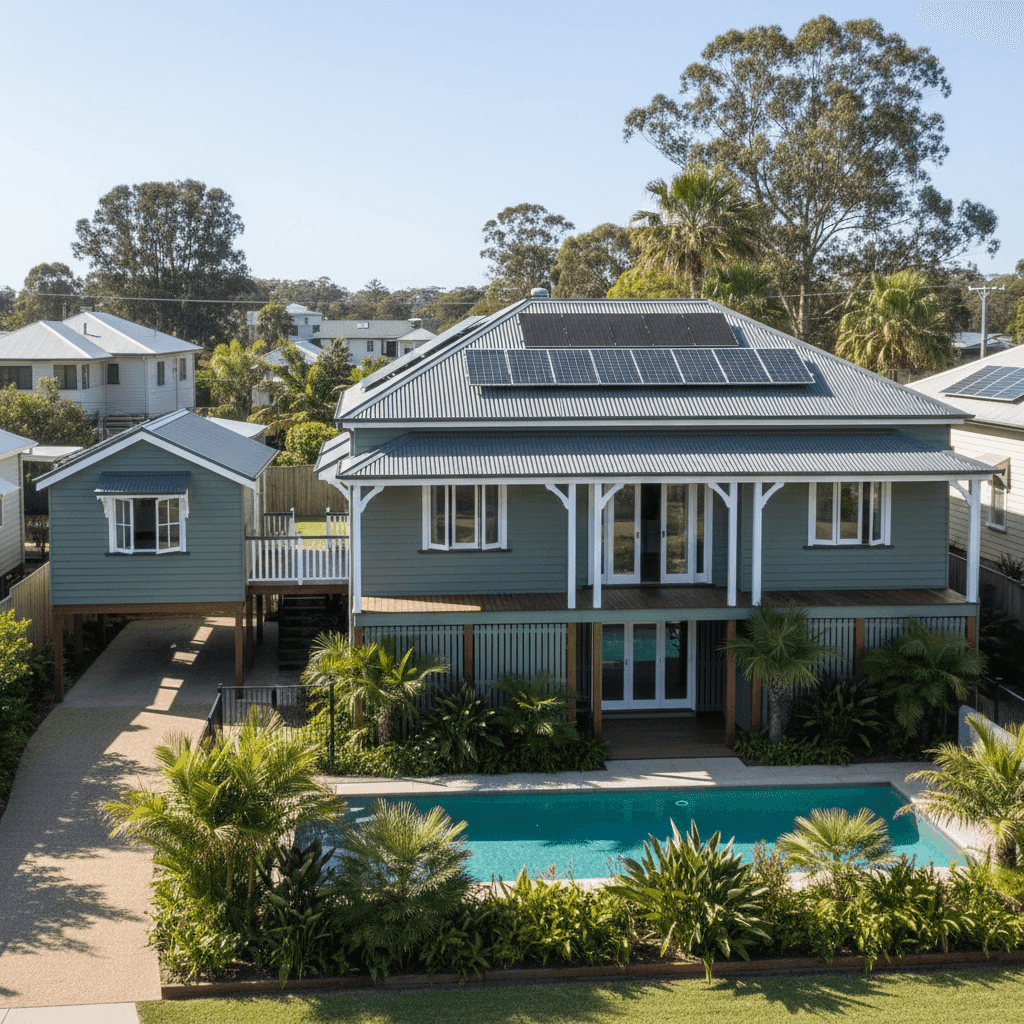

Grasmere is a semi-rural suburb tucked within the Wollondilly local government area on the southern fringe of Greater Sydney. Known for its spacious blocks and leafy character, it attracts families looking for room to breathe without straying too far from the city. If you own a free standing home here — particularly a larger weatherboard property with extras like a pool, solar panels, and a granny flat — understanding what you should be paying for building insurance is genuinely worthwhile. This article breaks down a recent quote for a 5-bedroom, 3-bathroom home in Grasmere, compares it against local and national benchmarks, and offers practical guidance for homeowners in the area.

---

Is This Quote Fair?

The quote in question comes in at $3,385 per year (or $317/month) for building-only cover on a 286 sqm weatherboard home with a $1,400,000 sum insured and a $5,000 building excess. Our analysis rates this as CHEAP — below average for the area.

That's a meaningful finding. With a suburb average of $5,452/yr and a suburb median of $6,321/yr, this quote sits well below what most Grasmere homeowners are paying. In fact, it lands almost exactly at the 25th percentile of local quotes ($3,389/yr), meaning roughly 75% of comparable properties in the postcode are attracting higher premiums.

For a home of this size and specification — elevated on stumps, clad in weatherboard, with a pool, solar array, and a granny flat — securing cover at this price point represents genuine value. That said, it's always worth scrutinising what's included in the policy, not just the sticker price. A lower premium can sometimes reflect narrower coverage, higher excesses, or exclusions that matter. Here, the $5,000 building excess is on the higher side, which partly explains the competitive premium — you're effectively self-insuring the first $5,000 of any building claim.

---

How Grasmere Compares

Context is everything when evaluating an insurance quote. Here's how this property's premium stacks up across different geographic benchmarks:

| Benchmark | Premium |

|---|---|

| This Quote | $3,385/yr |

| Grasmere (2570) Suburb Average | $5,452/yr |

| Grasmere (2570) Suburb Median | $6,321/yr |

| Wollondilly LGA Average | $2,297/yr |

| NSW State Average | $9,528/yr |

| NSW State Median | $3,770/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

A few things stand out here. First, the NSW state average of $9,528/yr is extraordinarily high relative to both the suburb and national figures — this is likely skewed upward by high-risk coastal and flood-prone postcodes across the state, as well as the significant variation in property values in Sydney's premium suburbs. The state median of $3,770/yr is a far more representative figure for typical NSW homeowners, and this quote sits comfortably below even that.

Second, the Wollondilly LGA average of $2,297/yr is notably lower than the Grasmere suburb average, suggesting that some properties within the broader LGA attract very competitive pricing — possibly smaller homes or those with lower sum insured values. This quote, with its $1.4 million sum insured, is priced reasonably given the coverage level.

For a deeper look at how premiums track across the postcode, visit the Grasmere suburb insurance stats page. You can also explore NSW-wide home insurance data or the national home insurance benchmarks for broader context.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct influence on what insurers charge. Understanding them helps you anticipate how your own quote might be shaped.

Weatherboard Timber Walls

Weatherboard construction is one of the most significant premium drivers for Australian homes. Timber is more susceptible to fire, rot, and termite damage than brick or rendered masonry, and it's generally more expensive to repair or replace. Insurers price this risk accordingly, so weatherboard homes typically attract higher premiums than comparable brick-veneer properties.

Elevated on Stumps

Being raised less than 1 metre off the ground on stumps is common in older Australian homes and can actually work in your favour from a flood-risk perspective — water is less likely to enter the living areas during a minor inundation event. However, the subfloor space also introduces risks around maintenance, pest access, and structural integrity that insurers factor into their assessments.

Steel/Colorbond Roof

Colorbond roofing is generally viewed favourably by insurers. It's durable, fire-resistant, and low-maintenance compared to terracotta tiles or older corrugated iron. This is a positive factor in premium calculations.

Swimming Pool

A pool adds to the replacement cost of the property and introduces liability considerations, both of which can nudge premiums upward. Ensuring your sum insured accounts for the full cost of pool reinstatement is important.

Solar Panels

Solar systems are now a standard inclusion in building cover for most insurers, but they do add to the overall replacement value of the home. At $1.4 million sum insured, this property appears to have factored in the solar installation appropriately.

Granny Flat

A secondary dwelling on the property increases the total insurable value and the complexity of any claim. It's essential to confirm with your insurer that the granny flat is explicitly covered under your building policy — some policies require separate disclosure or even a separate policy for secondary structures.

---

Tips for Homeowners in Grasmere

1. Review your sum insured annually With 286 sqm of living space, a pool, solar panels, and a granny flat, the cost to rebuild this property from scratch could shift significantly with changes in construction costs. Building costs in NSW have risen sharply in recent years. Make it a habit to reassess your sum insured each renewal — underinsurance is one of the most common and costly mistakes Australian homeowners make.

2. Understand your excess trade-off This quote carries a $5,000 building excess. While that's contributed to a lower annual premium, it means you'll be out of pocket for the first $5,000 of any claim. If your emergency fund is comfortable covering that amount, the trade-off makes sense. If not, it may be worth requesting a quote with a lower excess to compare the overall cost difference.

3. Maintain your weatherboard cladding Insurers can decline or reduce claims if damage is linked to poor maintenance. Weatherboard homes require regular painting and inspection for rot, warping, or pest damage. Staying on top of this not only protects your home but keeps your policy on solid footing.

4. Compare quotes at renewal — every year The insurance market shifts constantly, and loyalty doesn't always pay. With suburb premiums ranging from $3,389/yr at the 25th percentile all the way to $7,482/yr at the 75th percentile, there's clearly enormous variation in what Grasmere homeowners are being charged. Shopping around at each renewal is the single most effective way to avoid overpaying.

---

Find a Better Deal with CoverClub

Whether you're reviewing your current policy or insuring a new home in Grasmere, CoverClub makes it easy to compare building insurance quotes from multiple providers in one place. Our free comparison tool is designed for Australian homeowners and takes into account the specific features of your property. Get a quote today and see how your current premium stacks up.