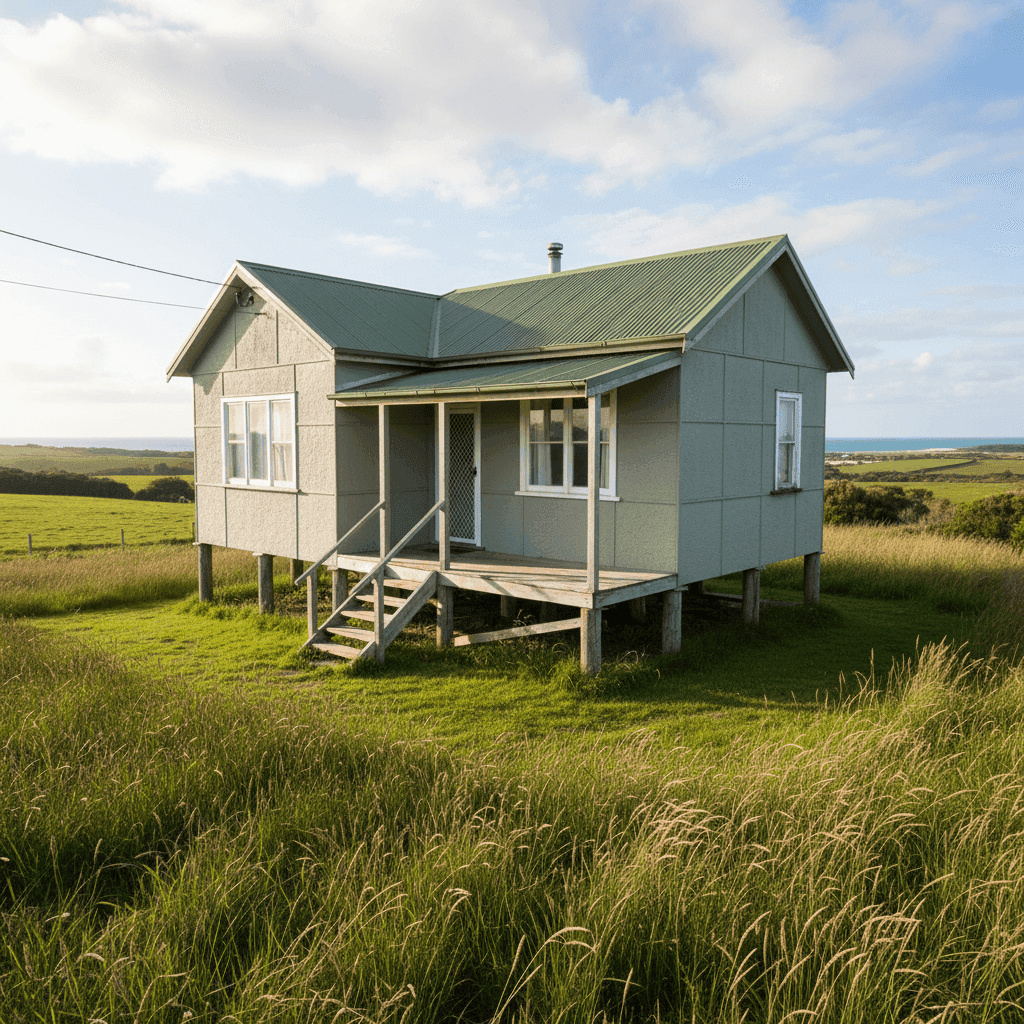

If you own a free standing home in Grassy, TAS 7256, you'll know that insuring a property on King Island comes with its own unique set of considerations. Remote location, island logistics, older building stock, and the particular construction methods common to the region all play a role in how insurers price your risk. In this article, we break down a real home and contents insurance quote for a 3-bedroom, 1-bathroom free standing home in Grassy — and help you understand whether the premium stacks up.

---

Is This Quote Fair?

The quote in question comes in at $3,883 per year (or $372/month) for combined home and contents cover, with a building sum insured of $702,000 and contents valued at $80,000. Both the building and contents excess are set at $1,000.

Our price rating for this quote is EXPENSIVE — above average for the area.

To put that in context: the suburb average for Grassy sits at $2,881/yr, and the median is $2,705/yr. This quote is roughly 35% above the suburb average and about 43% above the median. That's a meaningful gap, and it's worth understanding what's driving it before simply accepting the price.

That said, "expensive" doesn't automatically mean "wrong." A number of property-specific factors — which we'll explore below — can legitimately push a premium above the local norm. The key question is whether you're getting value for that extra spend, or whether shopping around could bring the cost down closer to the suburb benchmark.

---

How Grassy Compares

Here's how this quote sits relative to broader benchmarks:

| Benchmark | Premium |

|---|---|

| This Quote | $3,883/yr |

| Grassy (suburb average) | $2,881/yr |

| Grassy (suburb median) | $2,705/yr |

| Grassy (25th percentile) | $1,984/yr |

| Grassy (75th percentile) | $3,622/yr |

| Tasmania (state average) | $2,814/yr |

| Tasmania (state median) | $2,326/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

(Suburb data based on a sample of 19 quotes in the Grassy area.)

A few things stand out here. First, this quote exceeds even the 75th percentile for the suburb ($3,622/yr), meaning it's more expensive than at least three-quarters of comparable quotes in Grassy. That's a signal worth taking seriously.

Second, while the national average of $5,347/yr makes this quote look relatively modest on a broad scale, the national figure is heavily skewed by high-risk postcodes — particularly in Queensland and northern Australia. The more relevant comparison is the Tasmanian state average of $2,814/yr, against which this quote is about 38% higher.

You can explore detailed premium data for Grassy and the surrounding King Island area on the Grassy suburb stats page, or compare how Tasmania sits against the rest of the country on the national stats page.

---

Property Features That Affect Your Premium

Several characteristics of this particular property are likely contributing to the above-average premium. Understanding these can help you have a more informed conversation with insurers.

Fibro Asbestos External Walls

This is arguably the most significant premium driver. Homes built with fibro asbestos cladding — common in Australian construction from the 1940s through to the late 1980s — are more expensive to insure because repairs or rebuilds require specialised asbestos removal and disposal. Insurers factor in the additional cost and liability associated with disturbing asbestos-containing materials during a claim. With a construction year of 1975, this property sits squarely in the era when fibro was widely used.

Elevated on Stumps

The home is elevated by at least one metre on stump foundations. While elevation can offer some protection against minor flooding and ground moisture, it also introduces structural complexity. Stumps — particularly older timber ones — can deteriorate over time and may require inspection or replacement as part of a claim. Insurers often apply a loading to elevated homes for this reason.

Age of Construction (1975)

At around 50 years old, this home is considered mature by insurance standards. Older properties are more likely to have ageing electrical wiring, plumbing, and structural elements that increase the probability and cost of a claim. Combined with the fibro construction, the age of the home is a compounding risk factor.

Timber and Laminate Flooring

Timber flooring, particularly in an elevated home, can be susceptible to moisture ingress and warping. It's also more costly to repair or replace than concrete or tile alternatives, which can nudge building replacement costs — and therefore premiums — upward.

Ducted Climate Control

The presence of ducted climate control adds to the insured value of the home's fixtures and fittings. While not a major premium driver on its own, it does contribute to the overall replacement cost of the building.

Remote Island Location

Grassy is located on King Island, accessible only by air or sea. This geographic isolation means that in the event of a significant claim, trades, materials, and equipment all need to be transported to the island — adding substantially to rebuild costs. This is likely baked into the $702,000 building sum insured and will influence how insurers price the risk overall.

---

Tips for Homeowners in Grassy

If you're looking to manage your home insurance costs without compromising on cover, here are four practical steps worth considering.

1. Get multiple quotes before renewing With only 19 quotes in our Grassy sample, the local market is relatively thin — but the spread between the 25th percentile ($1,984/yr) and this quote ($3,883/yr) is enormous. Not all insurers price island properties or fibro homes the same way. Comparing quotes through CoverClub takes minutes and could reveal significantly cheaper options for equivalent cover.

2. Review your building sum insured carefully At $702,000 for a 130 sqm home in a remote location, the building sum insured reflects realistic rebuild costs including island logistics. However, it's worth getting a professional building valuation periodically to ensure you're neither over-insured (paying more than necessary) nor under-insured (exposed in a total loss scenario). Many Australians are unknowingly under-insured, which can be devastating at claim time.

3. Enquire about asbestos-specific policy terms Not all insurers handle asbestos the same way. Some policies exclude or limit cover for asbestos-related damage or removal costs. Before committing to a policy, ask specifically how asbestos is treated in the event of a claim — particularly for partial damage scenarios where fibro sheeting may need to be disturbed.

4. Consider increasing your excess to reduce your premium Both the building and contents excess on this quote are set at $1,000. Opting for a higher excess — say $2,000 or $2,500 — can meaningfully reduce your annual premium. This strategy works best if you have the financial buffer to cover a higher out-of-pocket cost in the event of a claim, and if you're unlikely to make small or frequent claims.

---

Compare Your Options with CoverClub

Whether you're reviewing an existing policy or shopping for the first time, CoverClub makes it easy to see how your home insurance quote stacks up. Our platform aggregates real quote data so you can benchmark your premium against your suburb, your state, and the national picture — all in one place.

Get a home insurance quote for your Grassy property today and find out if you could be paying less for the same level of cover.