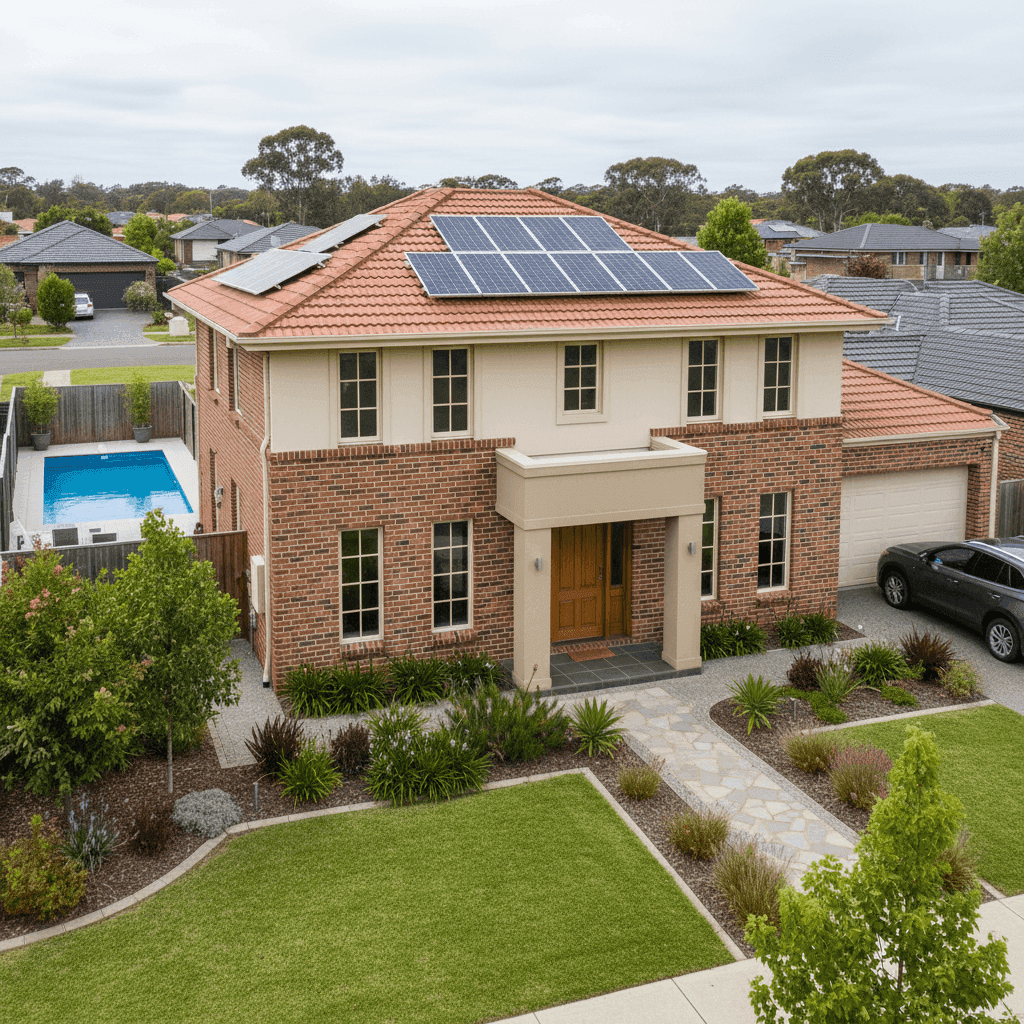

Greenvale is a well-established suburb in Melbourne's northern growth corridor, sitting within the City of Hume. Known for its family-friendly streets, parklands, and predominantly brick homes built from the late 1980s through the 2000s, it's a suburb where home insurance is a genuine consideration for most owners. This article breaks down a real home and contents insurance quote for a four-bedroom, free-standing brick veneer home in Greenvale (VIC 3059) — and helps you understand whether the price stacks up.

---

Is This Quote Fair?

The quote in question comes in at $2,213 per year (or $212/month) for combined home and contents cover, with a building sum insured of $900,000 and contents valued at $249,000. Both the building and contents excess are set at $1,000.

Our price rating for this quote is FAIR — Around Average. That assessment is based on how the premium sits relative to what other Greenvale homeowners are paying for similar cover. It's not a bargain, but it's not an outlier either. Given the relatively high sum insured on the building ($900,000 is substantial, even for a 214 sqm home), the premium is broadly reasonable.

That said, "fair" doesn't mean you can't do better. Premiums can vary significantly between insurers for the same property and level of cover, so it's always worth shopping around.

---

How Greenvale Compares

To put this quote in context, here's how it sits against local, state, and national benchmarks — based on 129 quotes collected for the Greenvale area:

| Benchmark | Premium |

|---|---|

| This quote | $2,213/yr |

| Greenvale suburb average | $1,963/yr |

| Greenvale suburb median | $1,925/yr |

| Greenvale 25th percentile | $1,433/yr |

| Greenvale 75th percentile | $2,457/yr |

| LGA (Hume) average | $1,775/yr |

| VIC state average | $3,000/yr |

| VIC state median | $2,718/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

A few things stand out here. First, Greenvale is genuinely affordable by Victorian and national standards. The suburb average of $1,963/yr is well below the state average of $3,000/yr, and a fraction of the national average of $5,347/yr — which is heavily skewed by high-risk areas in Queensland, Northern Australia, and coastal flood zones.

At $2,213/yr, this quote sits above the Greenvale suburb average and median, but comfortably within the 25th–75th percentile range ($1,433–$2,457). In other words, roughly half of Greenvale homeowners are paying between those two figures, and this quote lands squarely in that band. The higher-than-median price is likely driven by the elevated building sum insured and the presence of additional features like a pool and solar panels (more on those below).

Compared to the broader Hume LGA average of $1,775/yr, the quote is around $438 higher — again, largely attributable to the specific property features rather than the suburb itself being expensive to insure.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on the insurance premium:

Brick Veneer Construction & Tiled Roof

Brick veneer with a tiled roof is one of the most common and insurer-friendly combinations in suburban Melbourne. Both materials are considered durable and relatively low-risk, which generally keeps premiums competitive. Compared to timber-framed weatherboard homes or flat roofs, this construction profile is unlikely to attract loading from most insurers.

Slab Foundation

A concrete slab foundation is standard for homes built in this era and is generally viewed neutrally by insurers. It's worth noting, however, that slab homes can be more costly to repair if subsidence or soil movement occurs — something to keep in mind if your policy includes accidental damage cover.

Timber & Laminate Flooring

Timber and laminate floors can be more expensive to replace than carpet, and this is typically factored into contents or building valuations. Ensuring your contents sum insured adequately reflects the replacement cost of your flooring is important — underinsurance is a common issue for Australian homeowners.

Swimming Pool

A pool adds both value and liability to a property. From an insurance perspective, pools can increase the replacement cost of the home (factored into the building sum insured) and may also attract specific liability considerations. Always confirm your policy covers pool-related incidents, including damage to the pool structure itself.

Solar Panels

Solar panels are increasingly common on Melbourne homes and are generally covered under building insurance — but it pays to check the fine print. Panels should be included in your building sum insured calculation, as replacing a full system can cost $5,000–$15,000 or more depending on size and inverter type.

Ducted Climate Control

Ducted heating and cooling systems are a significant fixed asset in any home. Because they're built into the structure, they're typically covered under building insurance. However, the cost of replacing a full ducted system can run into the tens of thousands, so it's worth confirming your sum insured accounts for this.

Building Size & Sum Insured

At 214 sqm with a $900,000 building sum insured, the per-square-metre replacement cost implied here is approximately $4,200/sqm. This is on the higher end for a standard-finish home, though it may reflect the cost of inclusions like the pool, solar system, and ducted climate control. It's worth reviewing your sum insured periodically — both underinsurance and overinsurance can cost you money.

---

Tips for Homeowners in Greenvale

1. Review your building sum insured annually Construction costs in Melbourne have risen sharply over recent years. What was adequate coverage two or three years ago may no longer reflect the true rebuild cost of your home. Use a building cost calculator or speak with a quantity surveyor if you're unsure.

2. Check your solar panels and pool are explicitly covered Not all standard policies automatically extend to solar panel systems or pool structures without specific inclusion. Read your Product Disclosure Statement (PDS) carefully and ask your insurer directly if you're unsure what's covered.

3. Compare at least three quotes before renewing Insurers price risk differently, and loyalty doesn't always pay. Even if your current premium seems fair, you could find equivalent cover for meaningfully less by comparing options. Get a quote through CoverClub to see how your current premium measures up.

4. Consider your excess strategically A $1,000 excess on both building and contents is fairly standard. Opting for a higher excess (say, $2,000) can reduce your annual premium, which may make sense if you're unlikely to make small claims. Just ensure the excess remains affordable if you do need to claim.

---

Ready to Compare?

Whether you're a first-time buyer or a long-time Greenvale resident, it pays to make sure your home insurance is working as hard as you are. CoverClub makes it easy to compare home and contents quotes side by side, so you can see exactly what you're getting — and what you might be overpaying. Start your free quote today and benchmark your premium against the latest Greenvale data.