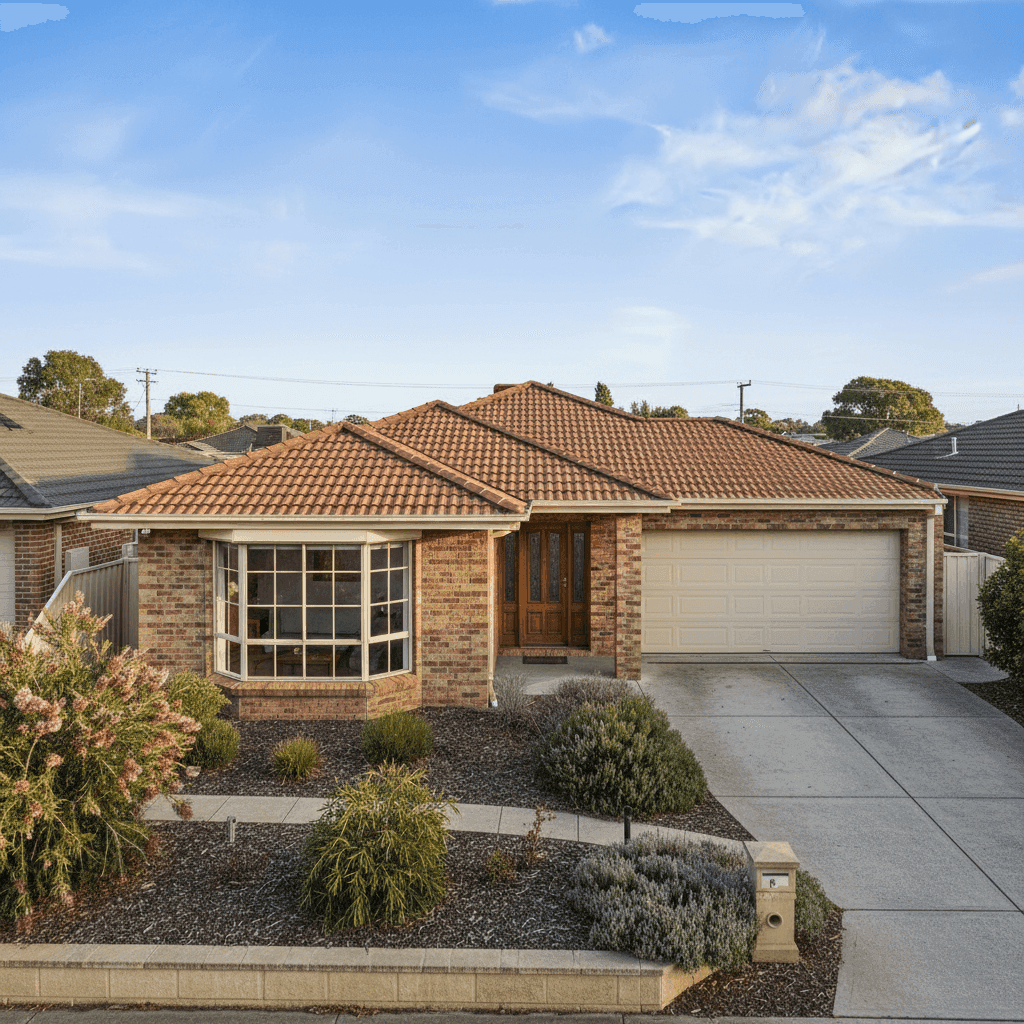

If you own a free standing home in Grovedale, VIC 3216, you're probably curious about what a fair home and contents insurance premium looks like — and whether the quote sitting in your inbox is worth accepting. This article breaks down a real quote for a four-bedroom, two-bathroom brick veneer home in Grovedale, compares it against local, state, and national benchmarks, and offers practical tips to help you make a confident decision.

---

Is This Quote Fair?

The quote in question comes to $1,693 per year (or roughly $166 per month) for combined home and contents cover. It includes a building sum insured of $663,000 and contents cover of $245,000, each with a $1,000 excess.

Our price rating for this quote is FAIR — Around Average, which means it sits in a reasonable range but isn't the cheapest option available in the suburb. To put that in perspective, the suburb's 25th percentile sits at $1,159/yr, meaning around a quarter of comparable properties in Grovedale are being insured for less. At the same time, the 75th percentile reaches $1,712/yr — so this quote is just under the upper boundary of what most locals pay.

In short: you're not overpaying dramatically, but there's likely room to find a more competitive premium if you're willing to shop around.

---

How Grovedale Compares

One of the most reassuring things about insuring a home in Grovedale is just how favourably the suburb compares to broader benchmarks. Here's a quick snapshot:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Grovedale (3216) | $1,413/yr | $1,468/yr |

| Greater Geelong LGA | $1,754/yr | — |

| Victoria (VIC) | $3,000/yr | $2,718/yr |

| National | $5,347/yr | $2,764/yr |

(Based on [Grovedale suburb data](https://coverclub.com.au/stats/VIC/3216/grovedale), [VIC state data](https://coverclub.com.au/stats/VIC), and [national data](https://coverclub.com.au/stats/national).)

The quote of $1,693/yr sits above the suburb average of $1,413/yr and the median of $1,468/yr, which is why it earns a "Fair" rather than "Great" rating. That said, compared to the Victorian state average of $3,000/yr, Grovedale homeowners are paying significantly less — roughly half the state average. And when stacked against the national average of $5,347/yr (which is heavily influenced by high-risk coastal, cyclone-prone, and flood-affected regions), Grovedale looks like a very affordable place to insure a home.

This is consistent with Grovedale's relatively low natural hazard profile. The suburb is not in a cyclone risk zone, and the Greater Geelong area generally doesn't face the extreme weather volatility seen in parts of Queensland, Western Australia, or Northern Australia — all of which push national averages skyward.

It's worth noting the suburb sample size here is 28 quotes, which is a reasonable dataset for a suburb of this size, though a larger sample would give even greater statistical confidence.

---

Property Features That Affect Your Premium

Several characteristics of this particular property influence where the premium lands:

- Brick Veneer Walls & Tiled Roof: This is one of the most common and insurer-favoured construction types in Victoria. Brick veneer offers solid fire resistance and structural durability, while a tiled roof is considered low-risk compared to alternatives like Colorbond or older fibrous cement. This combination typically attracts more competitive premiums.

- Slab Foundation: A concrete slab is a stable, well-understood foundation type that doesn't carry the same risk profile as older stumped or pier foundations. Insurers generally view slab homes favourably.

- Built in 2010: A relatively modern construction year means the home was built to contemporary building codes. Newer homes tend to have better wiring, plumbing, and structural integrity — all factors that reduce the likelihood of a claim and can positively influence your premium.

- 214 sqm Building Size: At 214 square metres, this is a generously sized family home. A larger floor area means a higher rebuilding cost, which is reflected in the $663,000 sum insured. Ensuring your building sum insured accurately reflects current construction costs is critical — underinsurance is a common and costly mistake.

- Ducted Climate Control: The presence of a ducted climate control system is factored into both the building sum insured and the overall risk profile. These systems add value to the property and can be costly to repair or replace, so it's important they're captured in your coverage.

- No Pool, No Solar Panels: The absence of a pool and solar panels keeps the risk profile straightforward. Pools introduce liability considerations, and solar panels (while increasingly common) add complexity around roof damage claims. Neither applies here, which simplifies the policy.

- Standard Fittings: Standard-quality fittings are easier and less expensive to replace than premium or custom finishes, which helps keep the contents and building replacement costs more predictable.

---

Tips for Homeowners in Grovedale

Whether you're reviewing an existing policy or shopping for the first time, here are four practical steps to get the most out of your home insurance:

- Compare multiple quotes before renewing. The difference between the 25th and 75th percentile in Grovedale is over $550 per year — that's real money. Loyalty to a single insurer rarely pays off. Use a comparison tool like CoverClub to see what competing insurers would charge for the same level of cover.

- Review your sum insured annually. Building costs in Victoria have risen considerably in recent years due to labour shortages and material price increases. A sum insured that was accurate in 2022 may leave you underinsured today. Check that your $663,000 building cover still reflects the true cost of rebuilding your home from scratch — not its market value.

- Consider a higher excess to lower your premium. If you have a solid emergency fund and are unlikely to make small claims, increasing your excess from $1,000 to $2,000 or more can meaningfully reduce your annual premium. Just make sure the saving justifies the additional out-of-pocket cost in a claim scenario.

- Document your contents thoroughly. With $245,000 in contents cover, it's worth maintaining an up-to-date home inventory — photos, receipts, and serial numbers stored securely in the cloud. This makes the claims process significantly smoother and helps ensure you're not over- or under-insuring your belongings.

---

Ready to Find a Better Deal?

Whether this quote works for you or you'd like to explore alternatives, CoverClub makes it easy to compare home and contents insurance options tailored to your property in Grovedale. Get a quote today and see how much you could save — or simply gain the confidence of knowing your current cover is genuinely competitive.