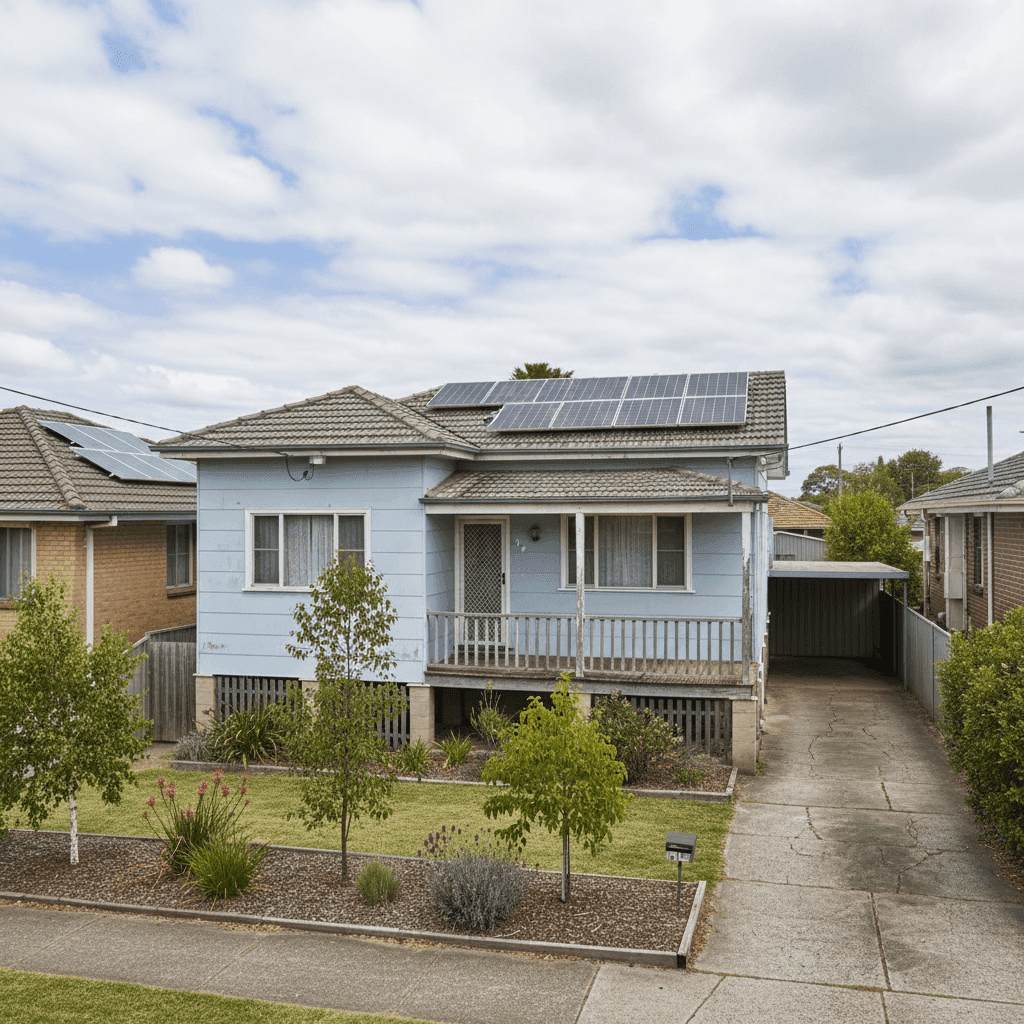

Guildford, nestled in Sydney's western suburbs within the City of Fairfield local government area, is a well-established neighbourhood of predominantly older, character-filled homes. This analysis looks at a building-only insurance quote for a three-bedroom, two-bathroom free-standing home in the 2161 postcode — and asks the question every homeowner should be asking: is this premium actually fair?

---

Is This Quote Fair?

The quote in question comes in at $4,277 per year (or $410 per month) for building-only cover, with a $1,000 building excess and a sum insured of $760,000.

Our price rating for this quote is EXPENSIVE — above average for the area.

To put that into perspective: the average building insurance premium across Guildford sits at just $1,671 per year, with a median of $1,693. This quote is more than 2.5 times the suburb average — a significant gap that warrants a closer look. Even at the 75th percentile (meaning 75% of quotes in the suburb are cheaper), the benchmark is only $2,230 per year. This quote clears that figure by over $2,000.

That said, premiums are never one-size-fits-all. The specific characteristics of this property — particularly its construction materials and age — play a substantial role in pushing the price higher. We'll unpack those factors below.

---

How Guildford Compares

Understanding where a quote sits relative to broader benchmarks helps homeowners make sense of what they're paying. Here's how Guildford stacks up:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Guildford (2161) | $1,671/yr | $1,693/yr |

| LGA (Fairfield) | $2,137/yr | — |

| NSW | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out here. NSW carries one of the highest average premiums in the country — largely driven by extreme outlier properties in flood-prone, bushfire-affected, or coastal high-risk zones that pull the average up sharply. The NSW median of $3,770 is a more reliable indicator for most homeowners, and Guildford's median sits well below that, suggesting the suburb is generally considered a moderate-risk area by insurers.

Compared to the national median of $2,764, Guildford's $1,693 median is genuinely competitive. For most properties in this postcode, insurance is reasonably affordable. This quote, however, is an outlier — driven by property-specific risk factors rather than location alone.

You can explore the full breakdown of Guildford insurance statistics, compare against NSW-wide data, or view national home insurance benchmarks on CoverClub.

---

Property Features That Affect Your Premium

Several characteristics of this home are likely contributing to the elevated premium. Here's what insurers are paying close attention to:

Fibro Asbestos External Walls

This is arguably the single biggest factor. Homes built with fibro asbestos cladding — common in Australian suburbs during the mid-20th century — are treated as high-risk by most insurers. The reason is straightforward: if the home is damaged and needs repair or rebuilding, the safe removal and disposal of asbestos-containing materials is extraordinarily expensive and heavily regulated. Many insurers either decline to cover these properties outright or apply significant premium loadings.

Construction Year: 1969

At over 55 years old, this home predates many modern building codes. Older homes are statistically more susceptible to electrical faults, plumbing failures, and structural issues — all of which increase the likelihood of a claim.

Stump Foundation

Homes on stumps (also known as pier foundations) can be more vulnerable to subsidence, termite damage, and moisture-related issues underneath the floor. Insurers factor this in when assessing structural risk.

Timber and Laminate Flooring

Timber flooring in older homes can be prone to warping, water damage, and fire spread. While not a major premium driver on its own, it contributes to the overall risk profile.

Solar Panels

Solar panels add value to the home and increase the replacement cost — which is reflected in the sum insured. They also introduce electrical risks if panels or inverters are damaged in a storm or fire. Most insurers include solar panels under building cover, but their presence can nudge premiums upward.

Ducted Climate Control

Like solar panels, ducted systems are a significant fixed asset that increases the cost to rebuild or repair. Their inclusion in the sum insured is appropriate, but it does contribute to a higher premium.

Sum Insured: $760,000

The building sum insured is on the higher end for a 139 sqm home, even accounting for construction complexity. It's worth reviewing whether this figure accurately reflects the rebuild cost (not the market value) of the property. Overinsuring can lead to unnecessarily high premiums, while underinsuring leaves you exposed.

---

Tips for Homeowners in Guildford

If you're a homeowner in Guildford — particularly in an older fibro property — here are some practical steps to manage your insurance costs without compromising your cover:

- Get multiple quotes. The spread between the cheapest and most expensive quotes in Guildford is enormous. Based on our data, the 25th percentile sits at $1,097 per year — meaning a quarter of quotes come in under that figure. Shopping around is essential, especially for high-risk construction types.

- Review your sum insured carefully. Work with a quantity surveyor or use an online building calculator to confirm your rebuild cost. If your sum insured is higher than it needs to be, you may be paying a premium loading you don't need.

- Ask about asbestos-specialist insurers. Not all insurers treat fibro homes the same way. Some specialist or non-standard insurers have more competitive pricing for older construction types. A broker with experience in this space can be invaluable.

- Consider your excess. Opting for a higher voluntary excess (say, $2,500 instead of $1,000) can meaningfully reduce your annual premium. Just make sure the saving justifies the additional out-of-pocket cost if you ever need to claim.

---

Compare Your Options with CoverClub

Whether you're renewing your policy or shopping for the first time, comparing quotes is the single most effective way to ensure you're not overpaying. CoverClub makes it easy to benchmark your premium against real data from properties just like yours.

Get a building insurance quote today and see how your current premium stacks up against the Guildford market — you might be surprised by what you find.