If you own a free standing home in Gunalda, QLD 4570, you're likely aware that home insurance can be a significant annual expense — particularly in Queensland, where weather risk and building costs push premiums well above the national norm. This article takes a close look at a real home and contents insurance quote for a four-bedroom weatherboard home in Gunalda, breaks down what's driving the price, and offers practical guidance for local homeowners looking to get the best value for their cover.

---

Is This Quote Fair?

The quote in question comes in at $2,072 per year (or $185 per month) for a combined home and contents policy. The building is insured for $306,000 and contents are covered up to $50,000, with a $4,000 building excess and a $1,000 contents excess.

Our price rating for this quote is FAIR — Around Average, and the data backs that up. The suburb average premium for Gunalda sits at $1,954 per year, meaning this quote is modestly above the local average but well within a reasonable range. Importantly, it falls comfortably below the suburb's 75th percentile of $2,861 per year, which means roughly three-quarters of comparable quotes in the area are either similar or more expensive.

That said, there is room to potentially do better. The suburb median is $1,568 per year, and the 25th percentile sits at $1,367 per year — suggesting that with the right insurer and policy structure, some homeowners in Gunalda are securing meaningfully cheaper cover. Whether those lower-priced policies offer equivalent protection is the critical question worth investigating before switching.

Overall, this quote is neither a bargain nor a rip-off. It's a reasonable starting point, but worth comparing before committing.

---

How Gunalda Compares

One of the most striking things about this quote is just how affordable Gunalda is relative to the broader Queensland and national picture. Take a look at the numbers:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Gunalda (suburb) | $1,954/yr | $1,568/yr |

| Fraser Coast LGA | $4,810/yr | — |

| Queensland (state) | $9,129/yr | $3,903/yr |

| National | $5,347/yr | $2,764/yr |

The contrast is stark. The Queensland state average of $9,129 per year is more than four times the Gunalda suburb average — a reflection of the enormous variation in risk across the state, with coastal and cyclone-prone areas driving premiums dramatically higher. Even the national average of $5,347 per year dwarfs what Gunalda homeowners are typically paying.

Interestingly, this property's quote also sits well below the Fraser Coast LGA average of $4,810 per year, which covers a broader region that includes higher-risk coastal localities. Gunalda's inland position, away from storm surge zones and cyclone corridors, clearly works in homeowners' favour.

You can explore more localised data for this postcode on the Gunalda suburb stats page.

> Note: The suburb sample size for this comparison is 9 quotes, so while directionally useful, these figures should be interpreted with some caution. A larger dataset would provide greater statistical confidence.

---

Property Features That Affect Your Premium

Every property is different, and insurers weigh up a range of characteristics when calculating your premium. Here's how the key features of this particular home are likely influencing the quote:

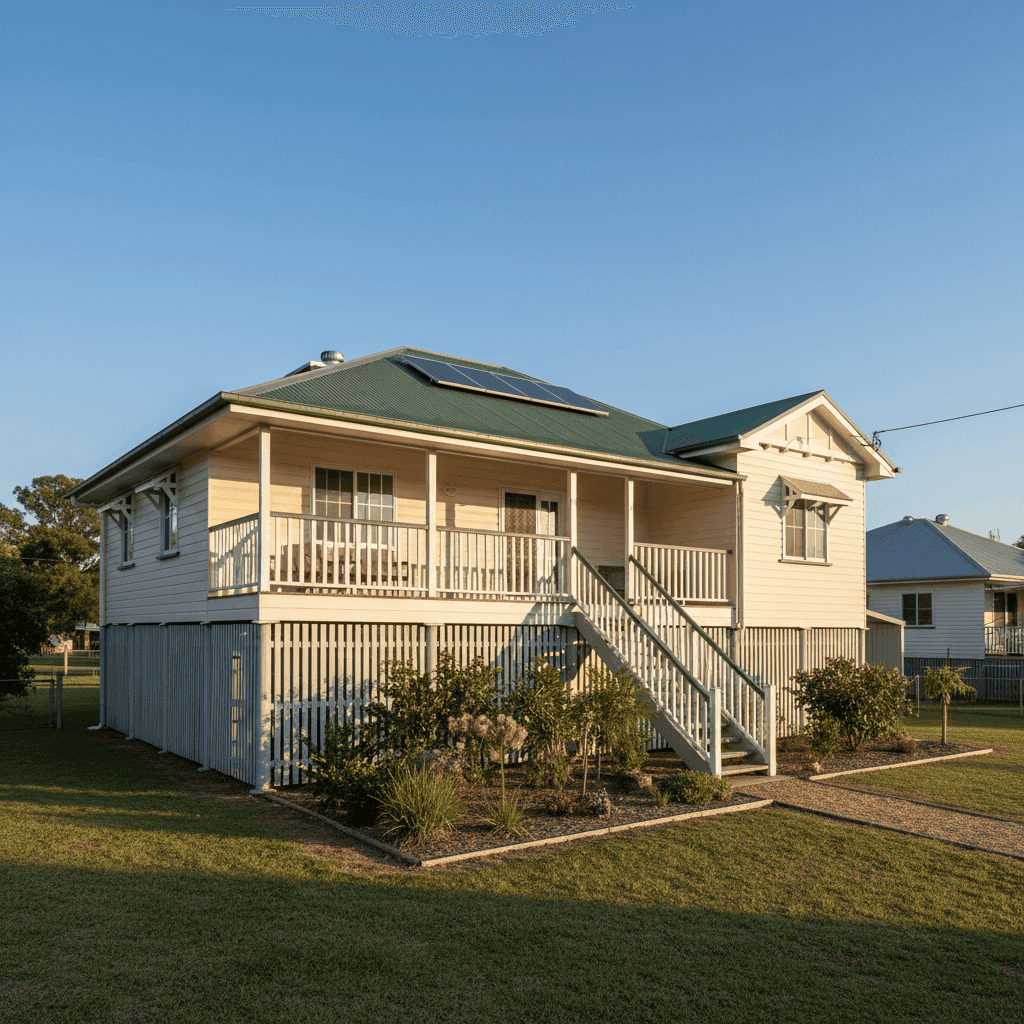

Weatherboard Timber Walls

Weatherboard construction is common in older Queensland homes, but it does carry a higher fire risk than brick or rendered masonry. Insurers typically rate timber-clad homes at a slightly elevated risk, which can push premiums up compared to equivalent brick homes. It also means replacement costs can be higher if significant damage occurs.

Construction Year: 1965

At around 60 years old, this home predates many modern building codes. Older homes can have ageing electrical wiring, plumbing, and structural components that may be more susceptible to damage — all factors that insurers consider. That said, a well-maintained older home can still attract competitive premiums.

Stump Foundation

Homes on stumps (also called timber or steel pier foundations) are very common in Queensland, and insurers are well-versed in underwriting them. The raised foundation can actually be beneficial in areas prone to minor flooding, as it lifts the floor above ground level. However, it also introduces the risk of subfloor damage from moisture, pests, or structural movement.

Steel/Colorbond Roof

This is a genuine positive from an insurance perspective. Colorbond steel roofing is durable, fire-resistant, and performs well in high-wind conditions. It's generally viewed more favourably by insurers than older materials like terracotta tiles or asbestos sheeting, and can contribute to a lower premium.

Solar Panels

The property has solar panels installed. While these are a great investment for energy savings, they do add to the replacement value of the home and should be explicitly covered under the building sum insured. It's worth confirming with your insurer that solar panels — including inverters and mounting hardware — are included in your policy.

Sum Insured: $306,000 for 105 sqm

At approximately $2,914 per square metre, the building sum insured is within a plausible range for a weatherboard home with standard fittings, though construction costs have risen sharply in recent years. It's worth reviewing this figure periodically to ensure you're not underinsured.

---

Tips for Homeowners in Gunalda

1. Review Your Sum Insured Annually

Building costs in regional Queensland have increased significantly since the COVID-era construction boom. If your sum insured hasn't been updated in a few years, there's a real risk you could be underinsured in the event of a total loss. Use an independent building cost calculator or speak with a local builder to get a realistic rebuild estimate.

2. Consider Raising Your Excess Strategically

This policy carries a $4,000 building excess, which is relatively high. While a higher excess does typically reduce your annual premium, make sure you could comfortably cover that amount out of pocket if you needed to make a claim. If cash flow is a concern, it may be worth modelling the premium difference at a lower excess level.

3. Confirm Solar Panel Coverage

As noted above, solar panels are an asset worth thousands of dollars. Check your policy's Product Disclosure Statement (PDS) to confirm they're covered, under what circumstances, and whether there are any sub-limits that apply. Not all policies treat solar the same way.

4. Compare at Least Every Two Years

Insurance premiums can shift significantly from year to year, and loyalty doesn't always pay. Given that the Gunalda suburb data shows a spread from $1,367 to $2,861 per year, there's clearly meaningful variation between insurers. Running a comparison before your renewal date costs nothing and could save you hundreds.

---

Ready to Compare Home Insurance in Gunalda?

Whether you're reviewing an existing policy or shopping for cover on a new property, comparing quotes is the single most effective way to ensure you're not overpaying. At CoverClub, we make it easy to see how your premium stacks up against local and national benchmarks.

Get a home insurance quote today and find out if you could be paying less for the same level of protection.