If you own a free standing home in Hamilton, VIC 3300, you've probably wondered whether you're paying too much — or too little — for home insurance. This article breaks down a real home and contents insurance quote for a three-bedroom, two-bathroom brick veneer home in Hamilton, comparing it against local, state, and national benchmarks to help you understand what's driving the price and whether it represents good value.

---

Is This Quote Fair?

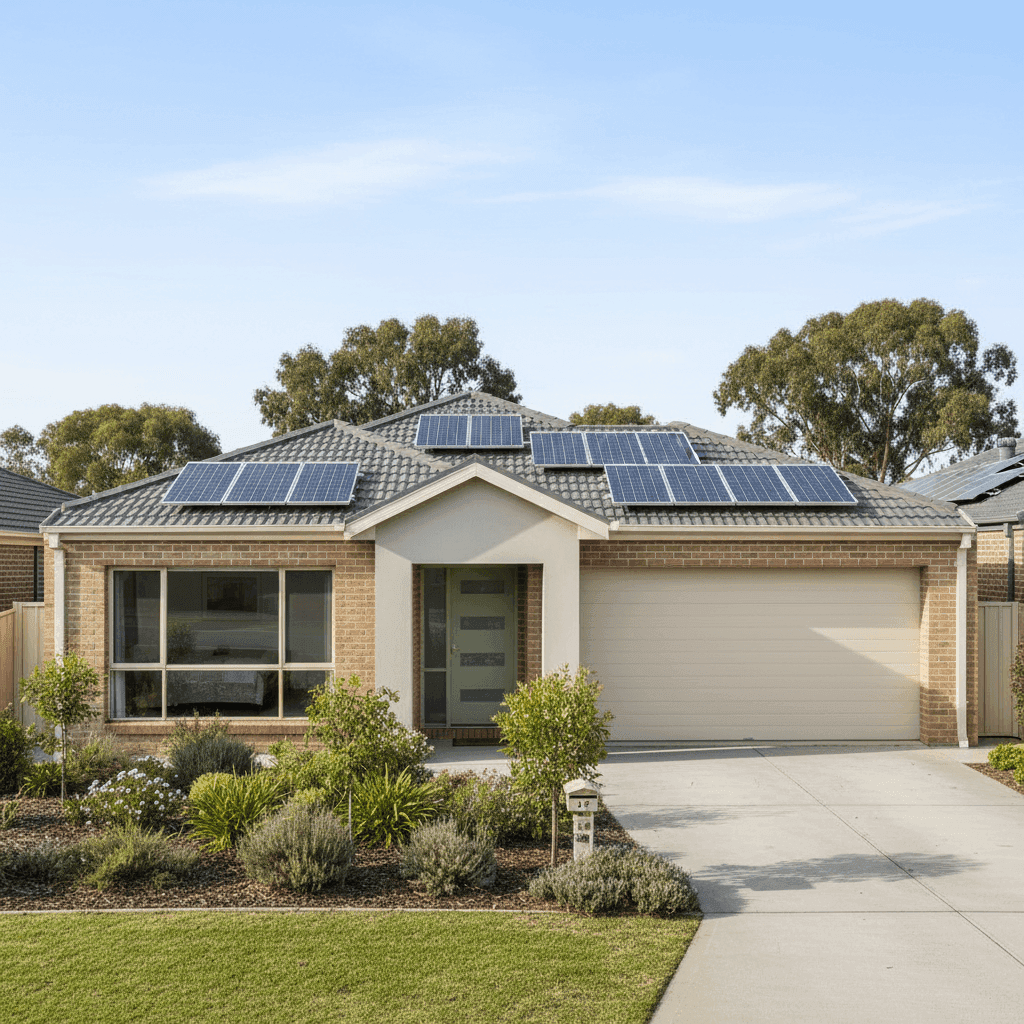

The quote in question comes in at $1,524 per year (or roughly $146 per month) for combined home and contents cover, with a building sum insured of $550,000 and contents valued at $90,000. The building excess sits at $5,000, with a separate $1,000 excess for contents claims.

Our price rating for this quote is CHEAP — below average — and the data backs that up convincingly.

Compared to the suburb average for Hamilton of $2,168/year, this quote is $644 cheaper annually, representing a saving of nearly 30%. Even against the suburb's 25th percentile — meaning the cheapest quarter of quotes collected — the premium of $1,780/year is still higher than what this homeowner is paying. In other words, this quote sits below the cheapest tier of the local market, making it genuinely competitive.

For a homeowner in Hamilton, this is a strong result. The combination of a relatively modest contents value, a higher building excess of $5,000, and the property's solid construction characteristics all contribute to keeping the premium down.

---

How Hamilton Compares

To put this quote in proper context, it helps to zoom out and look at the broader insurance landscape.

| Benchmark | Annual Premium |

|---|---|

| This Quote | $1,524 |

| Hamilton Suburb Average | $2,168 |

| Hamilton Suburb Median | $2,137 |

| Hamilton 25th Percentile | $1,780 |

| Hamilton 75th Percentile | $2,500 |

| VIC State Average | $3,000 |

| VIC State Median | $2,718 |

| Southern Grampians LGA Average | $3,537 |

| National Average | $5,347 |

| National Median | $2,764 |

(Based on 27 quotes collected for Hamilton VIC 3300. See the full [Hamilton suburb stats](https://coverclub.com.au/stats/VIC/3300/hamilton), [VIC state stats](https://coverclub.com.au/stats/VIC), and [national stats](https://coverclub.com.au/stats/national).)

What stands out here is just how affordable Hamilton is relative to the rest of Victoria and the country. The VIC state average of $3,000/year is nearly double this quote, and the national average of $5,347/year is more than three times higher. Much of that national figure is skewed upward by high-risk regions — particularly cyclone-prone areas in Queensland and Western Australia — but even the national median of $2,764 sits well above what Hamilton homeowners typically pay.

Interestingly, the Southern Grampians LGA average of $3,537 is noticeably higher than the Hamilton suburb average of $2,168. This suggests that while Hamilton itself is relatively affordable to insure, other parts of the LGA — potentially more rural or flood-exposed areas — pull the regional average up. If you're located in Hamilton proper, you're likely benefiting from a more favourable risk profile than the broader LGA suggests.

---

Property Features That Affect Your Premium

Several characteristics of this property work in the homeowner's favour when it comes to insurance pricing.

Brick veneer construction is generally well-regarded by insurers. It offers solid fire resistance compared to timber-framed homes with weatherboard cladding, and it holds up well against everyday weather events. Combined with a concrete tile roof, this home presents a relatively low-risk profile from a structural standpoint — concrete roofs are durable, fire-resistant, and less susceptible to storm damage than older corrugated iron roofing.

The slab foundation is another positive. Slab homes tend to have fewer issues with subfloor moisture, pests, and structural movement compared to homes on stumps or piers — all factors that can influence how an insurer assesses your risk.

Built in 2005, this property is modern enough to have been constructed under relatively recent building codes, which typically mandate improved fire safety, structural standards, and waterproofing. Homes built post-2000 often attract more competitive premiums than older stock.

Solar panels are worth noting. While they add value to the property, they can slightly increase rebuild costs and introduce a minor fire risk if not properly maintained. Most standard home insurance policies do cover solar panels as a fixture of the building, but it's worth confirming your policy wording to ensure your system is adequately protected.

The presence of ducted climate control adds to the overall replacement value of the home, which is already reflected in the $550,000 building sum insured. Ensuring your sum insured accurately accounts for all fixed features — including HVAC systems — is important to avoid being underinsured at claim time.

Hamilton is not in a cyclone risk zone, which is a meaningful factor. Cyclone-rated premiums in northern Australia can be eye-watering, so Hamilton homeowners benefit from a more benign climate risk profile overall.

---

Tips for Homeowners in Hamilton

1. Review your building sum insured regularly Construction costs have risen significantly in recent years. With a sum insured of $550,000 on a three-bedroom brick veneer home built in 2005, it's worth checking whether this figure would genuinely cover a full rebuild — including demolition, debris removal, and the cost of hiring tradespeople in a regional area. Underinsurance is one of the most common and costly mistakes homeowners make.

2. Consider whether your excess level suits your situation This quote carries a $5,000 building excess, which is on the higher end. While a higher excess typically reduces your premium, it also means you'll need to cover more out of pocket before your insurer steps in. If a $5,000 outlay would be a financial stretch, it may be worth requesting a lower excess — even if it bumps the annual premium slightly.

3. Check your solar panel coverage With solar panels installed, confirm with your insurer exactly what's covered. Some policies cover panels under the building, others treat them separately, and coverage for mechanical or electrical breakdown can vary. Make sure you're not left exposed if panels are damaged by hail, storm, or a system fault.

4. Shop around at renewal time Even though this quote is already well below average, insurance premiums can shift significantly at renewal. Insurers don't always reward loyalty with competitive pricing. Setting a reminder to compare quotes each year — even if you're happy with your current cover — is a simple habit that can save hundreds of dollars.

---

Compare Home Insurance Quotes in Hamilton

Whether you're a first-time buyer or a long-term homeowner in Hamilton, comparing quotes is the single most effective way to ensure you're not overpaying. At CoverClub, you can quickly see how your premium stacks up against others in your suburb and across Victoria — and find cover that suits both your property and your budget.