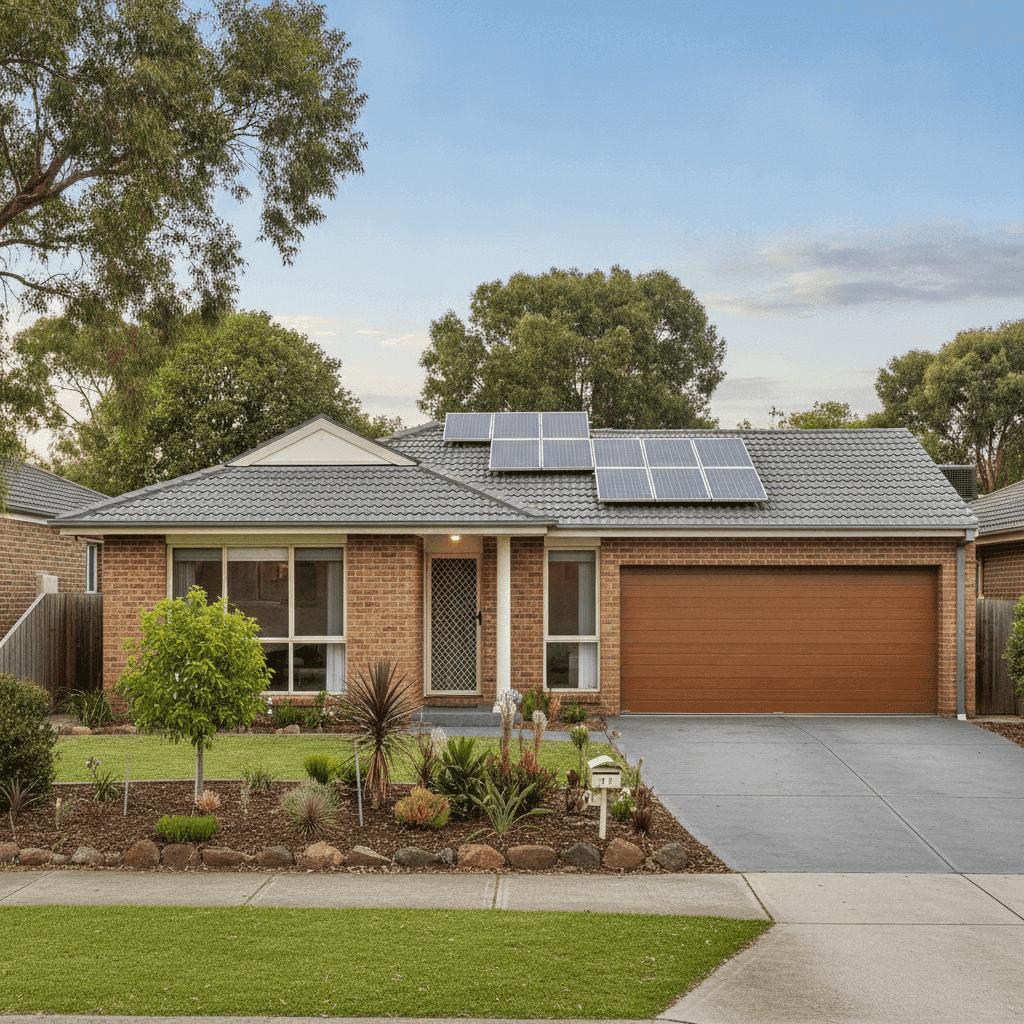

If you own a free standing home in Hampton Park, VIC 3976, you've probably wondered whether you're paying a fair price for home and contents insurance — or whether there's a better deal out there. This article breaks down a real insurance quote for a four-bedroom, two-bathroom brick veneer home in the suburb, compares it against local, state, and national benchmarks, and offers practical tips to help you get better value on your cover.

---

Is This Quote Fair?

The quote in question comes in at $1,997 per year (or $191/month) for combined home and contents insurance, covering a building sum insured of $622,000 and contents valued at $150,000, each with a $1,000 excess.

Our price rating for this quote is Expensive — above average for the Hampton Park area.

To put that in context: the suburb average premium in Hampton Park sits at $1,358/year, with a median of $1,344/year. This quote lands $639 above the suburb average — roughly 47% more than what many comparable properties in the area are paying. Even against the 75th percentile of $1,653/year (meaning 75% of quotes are cheaper), this premium is still $344 higher.

That said, "expensive" doesn't automatically mean "wrong." The building sum insured of $622,000 is likely higher than many comparable properties in the suburb, and the $150,000 contents cover adds meaningful weight to the premium. Higher insured values naturally push premiums up. But it does suggest there's room to shop around and potentially find equivalent cover at a more competitive price point.

---

How Hampton Park Compares

Understanding where Hampton Park sits in the broader insurance landscape helps put this quote in perspective.

| Benchmark | Premium |

|---|---|

| This quote | $1,997/yr |

| Hampton Park suburb average | $1,358/yr |

| Hampton Park suburb median | $1,344/yr |

| LGA (Casey) average | $2,142/yr |

| VIC state average | $3,000/yr |

| VIC state median | $2,718/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

(Based on 31 quotes sampled in the Hampton Park area.)

Compared to Victoria as a whole, this quote is actually below the state average of $3,000/year — a meaningful saving. And when you zoom out to the national picture, where the average premium sits at a striking $5,347/year (driven significantly by high-risk regions like North Queensland and coastal flood zones), Hampton Park homeowners are in a relatively favourable position.

The City of Casey LGA average of $2,142/year also sits above this quote, suggesting that while the premium is expensive within the immediate suburb, it's not out of step with the broader local government area.

The takeaway? Hampton Park is a relatively affordable suburb to insure compared to much of Victoria and the country — but within the suburb itself, this particular quote has room for improvement.

---

Property Features That Affect Your Premium

Several characteristics of this property will be influencing the premium, both positively and negatively.

Brick veneer construction is generally viewed favourably by insurers. It's durable, fire-resistant, and less susceptible to storm damage than timber-framed homes with weatherboard cladding. Paired with a tiled roof, this home presents a solid risk profile from a structural standpoint — tiles are long-lasting and perform well in most weather conditions.

The slab foundation is standard for homes of this era and construction type in Melbourne's south-east, and doesn't typically attract any premium loading. Similarly, timber and laminate flooring is a common feature that insurers treat as routine.

Built in 1995, the home is now around 30 years old. While not brand new, it's also not old enough to attract significant age-related risk loadings — though insurers may factor in the likelihood of ageing plumbing, wiring, or roofing materials when pricing the policy.

At 214 square metres, this is a comfortably sized family home, and the $622,000 building sum insured reflects the cost of rebuilding a property of this scale with standard fittings in today's construction environment. It's worth ensuring this figure is accurate — underinsurance is a serious risk, but overinsurance means you're paying more than necessary.

The presence of solar panels is worth noting. Panels add replacement value to the roof and can complicate claims if damaged by hail or storm. Some insurers include solar panels under the building policy automatically; others require you to specify them or may apply a loading. It's worth confirming exactly how your policy treats solar panel cover.

Ducted climate control is another feature that adds to the replacement value of the home's fixtures and fittings, and is factored into the building sum insured. Ensure your policy explicitly covers fixed air conditioning systems — most building policies do, but it's always worth checking the Product Disclosure Statement (PDS).

The absence of a pool removes one common source of liability risk and premium loading, which works in the homeowner's favour.

---

Tips for Homeowners in Hampton Park

1. Review your sum insured carefully. The $622,000 building sum insured is the single biggest driver of your premium. Use an independent building cost calculator (such as the one provided by the Housing Industry Association or your insurer) to verify this figure is accurate for your property size, construction type, and local labour costs. If it's higher than necessary, you may be able to reduce it — and your premium along with it.

2. Shop around — at least annually. The 47% gap between this quote and the suburb average is a strong signal that comparable cover may be available at a lower price. Insurers price risk differently, and loyalty doesn't always pay. Use a comparison service like CoverClub to benchmark your renewal quote before you accept it.

3. Confirm your solar panel coverage. With solar panels on the roof, make sure your policy clearly outlines how panels are covered — whether for storm, hail, fire, or accidental damage. Some policies exclude panels or cap their replacement value. If your insurer's treatment of solar isn't satisfactory, it may be a reason to switch.

4. Consider your excess level. Both the building and contents excess on this policy sit at $1,000. Increasing your excess — say, to $2,000 — can meaningfully reduce your annual premium. If you have the financial buffer to absorb a larger out-of-pocket cost in the event of a claim, a higher excess is often a smart trade-off.

---

Compare Your Home Insurance Today

Whether you're renewing your policy or buying cover for the first time, it pays to compare. Hampton Park is a competitive suburb to insure, and there's clearly a range of pricing in the market. Get a home insurance quote through CoverClub to see how your current premium stacks up — and whether you could be paying less for the same level of protection.