Home insurance premiums can vary dramatically from one street to the next, and Hampton Park in Melbourne's south-east is no exception. This article breaks down a real home and contents insurance quote for a five-bedroom, free-standing home in Hampton Park, VIC 3976 — examining whether the price stacks up, how it compares to local and national benchmarks, and what you can do to make sure you're not overpaying.

---

Is This Quote Fair?

The quote in question comes in at $2,329 per year (or $223/month) for combined home and contents cover, with a $850,000 building sum insured and $150,000 in contents cover. Both the building and contents excess are set at $1,000.

Our price rating for this quote is Expensive — above average for the Hampton Park area.

To put that in context: the suburb average annual premium sits at just $1,358, and the median is $1,344. That means this quote is running roughly $971 above the suburb average — a 71% premium over what most Hampton Park homeowners are paying. Even the 75th percentile for the suburb (meaning 75% of quotes are cheaper) is only $1,653 per year, which is still $676 less than this quote.

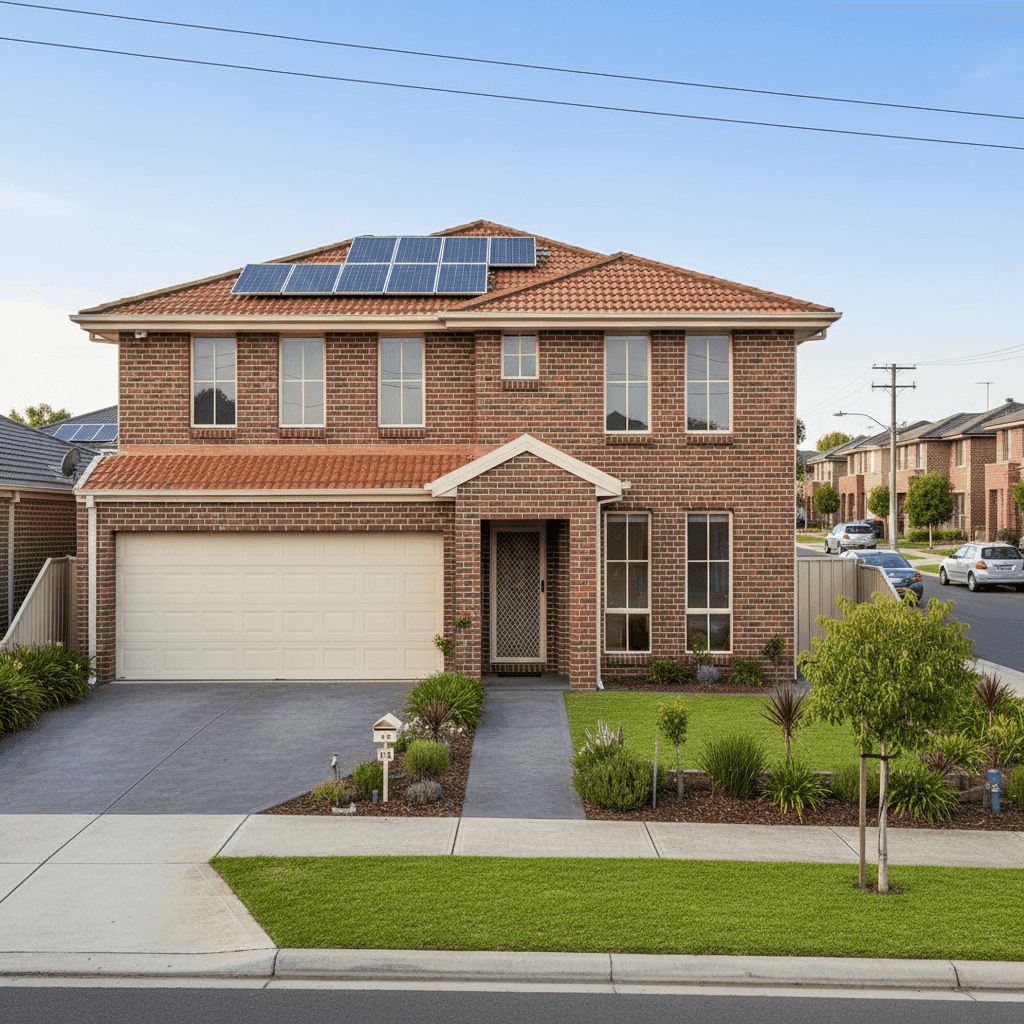

That said, it's worth noting that this is a large, well-appointed home — 286 sqm across five bedrooms and three bathrooms — which naturally attracts a higher premium than a typical three-bedroom property. The $150,000 contents cover and $850,000 building sum insured are also on the higher end and will be driving the cost up. Still, the gap is significant enough to warrant shopping around.

---

How Hampton Park Compares

Looking at the broader picture, Hampton Park actually sits well below both state and national averages — which is good news for locals. Here's how the numbers line up:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $2,329 |

| Hampton Park Suburb Average | $1,358 |

| Hampton Park Suburb Median | $1,344 |

| LGA (Casey) Average | $2,142 |

| VIC State Average | $3,000 |

| VIC State Median | $2,718 |

| National Average | $5,347 |

| National Median | $2,764 |

(Based on 31 quotes collected for the Hampton Park suburb)

Compared to the Victorian state average of $3,000/yr, this quote is actually below the state benchmark — which is a reasonable sign. And when you zoom out to the national average of $5,347/yr, it looks positively affordable. Australia's insurance market has been under significant pressure in recent years due to extreme weather events, rising rebuild costs, and reinsurance price hikes, which is pushing national averages skyward.

At the LGA level, the City of Casey average sits at $2,142/yr — and this quote at $2,329 is only modestly above that, suggesting the pricing isn't wildly out of step with the broader local government area, even if it's above the suburb's own average.

The takeaway? This quote is expensive relative to Hampton Park, but reasonable when viewed through a state or national lens. The suburb itself appears to be a relatively affordable area for home insurance, which makes the above-average pricing here more noticeable.

---

Property Features That Affect Your Premium

Several characteristics of this property will be influencing the premium, both positively and negatively.

Factors likely keeping the premium in check:

- Brick veneer construction is generally well-regarded by insurers. It offers solid fire resistance and structural durability compared to weatherboard or lightweight cladding, which can attract lower base rates.

- Tiled roof is another tick in the right column — tiles are durable, fire-resistant, and less prone to storm damage than some alternatives like Colorbond in certain conditions.

- Concrete slab foundation is considered low-risk by most insurers, as it's less susceptible to subsidence or pest damage than older stumped or timber-framed foundations.

- No pool removes a common liability risk and a source of additional premium loading.

- No cyclone risk — Hampton Park is not in a designated cyclone zone, which keeps premiums lower than properties in northern Australia.

- Construction year of 2005 means the home is relatively modern, built to contemporary building codes, and unlikely to have the wiring or plumbing issues associated with older properties.

Factors that may be pushing the premium higher:

- 286 sqm of living space across five bedrooms and three bathrooms is a large home. Larger homes cost more to rebuild, and the $850,000 sum insured reflects that.

- Solar panels add value to the property but also introduce an additional insurable asset. Many insurers will factor in the replacement cost of solar systems, which can add to the building sum insured.

- Ducted climate control is another high-value fixed asset that contributes to rebuild costs and, by extension, to the appropriate sum insured.

- $150,000 contents cover is a meaningful amount — higher contents values mean higher premiums, though it's important not to underinsure here.

---

Tips for Homeowners in Hampton Park

1. Review your sum insured carefully A $850,000 building sum insured is substantial. Make sure this figure reflects the rebuild cost of your home (not its market value), including demolition, materials, and labour at current rates. Overinsuring inflates your premium unnecessarily, while underinsuring leaves you exposed. Consider using an online building calculator or engaging a quantity surveyor for a more precise figure.

2. Shop around — especially if you're above the suburb average With 31 quotes in our Hampton Park dataset showing an average of just $1,358/yr, there's clearly a wide range of pricing in this suburb. Even accounting for the size and features of this property, comparing multiple insurers could yield meaningful savings. Get a quote through CoverClub to see how different providers price your specific risk.

3. Consider your excess level Both building and contents excesses are set at $1,000 here, which is a moderate level. Opting for a higher voluntary excess — say $2,000 or $2,500 — can noticeably reduce your annual premium. Just make sure you can comfortably cover that amount out of pocket if you need to make a claim.

4. Bundle and ask about discounts Many insurers offer discounts for combining home and contents cover (which this policy already does), but there may be further savings available for paying annually rather than monthly, for security features like alarm systems, or for long-term customer loyalty. It's always worth asking.

---

Compare Your Home Insurance Today

Whether you're a Hampton Park local or elsewhere in Victoria, it pays to know where your premium sits relative to the market. CoverClub makes it easy to benchmark your current cover and explore alternatives — without the hassle of ringing around. Start comparing home insurance quotes now and find out if you're getting a fair deal on your most valuable asset.