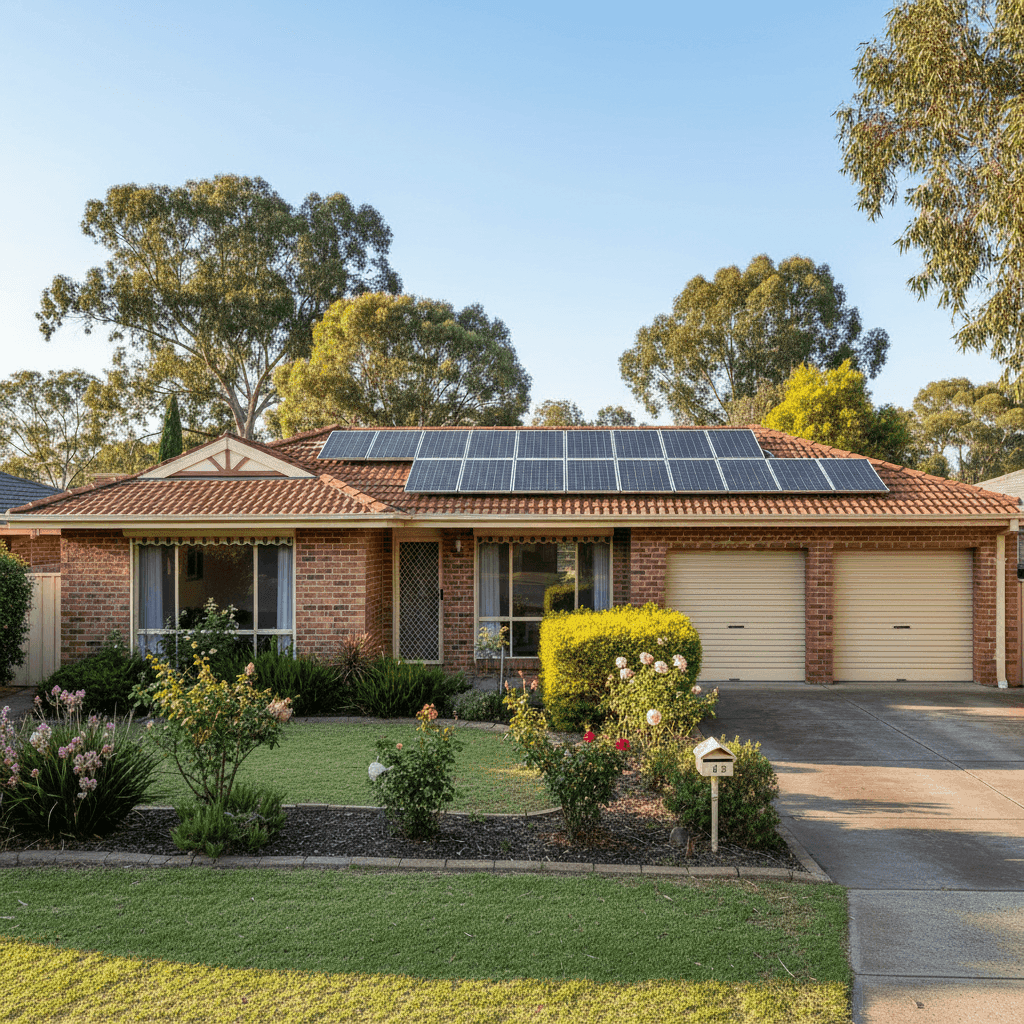

Happy Valley, nestled in the southern suburbs of Adelaide within the City of Onkaparinga, is a well-established residential area known for its leafy streets and family-friendly character. For owners of free standing homes in this suburb, understanding what drives your home insurance premium — and whether you're paying a fair price — can make a meaningful difference to your household budget. This article breaks down a real home and contents insurance quote for a four-bedroom brick veneer home in Happy Valley, SA 5159, and puts it in context against local, state, and national benchmarks.

---

Is This Quote Fair?

The annual premium for this quote comes in at $1,868 per year (or $179/month), covering both building (sum insured: $650,000) and contents ($251,000), each with a $500 excess. Based on our pricing analysis, this quote is rated Expensive — above average for the Happy Valley area.

To put that in perspective: the suburb average premium sits at $1,254/year, and the median is even lower at $1,205/year. This quote is roughly 49% above the suburb average and sits well above the 75th percentile threshold of $1,616/year — meaning fewer than one in four quotes in this suburb come in this high.

That said, "expensive" doesn't automatically mean "wrong." The sum insured figures here are on the higher end — a $650,000 building cover and $251,000 in contents is a substantial level of protection. Higher insured values naturally push premiums up, and insurers price accordingly. The presence of solar panels and ducted climate control also adds to the replacement cost calculation, which can influence the final premium.

---

How Happy Valley Compares

Understanding where Happy Valley sits in the broader insurance landscape helps frame whether you're getting value for money. Here's a snapshot:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $1,868 |

| Happy Valley Suburb Average | $1,254 |

| Happy Valley Suburb Median | $1,205 |

| Happy Valley 25th Percentile | $787 |

| Happy Valley 75th Percentile | $1,616 |

| LGA (Onkaparinga) Average | $1,431 |

| SA State Average | $2,433 |

| SA State Median | $1,679 |

| National Average | $5,347 |

| National Median | $2,764 |

You can explore the full local data on the Happy Valley suburb stats page, or compare it against broader South Australia insurance statistics and the national home insurance overview.

One encouraging takeaway: Happy Valley remains significantly more affordable than both the SA state average and the national average. Even this above-average quote is well below the SA average of $2,433/year and a fraction of the national average of $5,347/year. Homeowners in this part of Adelaide are, broadly speaking, in a relatively favourable insurance environment — though there's clearly still room to shop around within the suburb itself.

---

Property Features That Affect Your Premium

Several characteristics of this property directly influence how insurers assess risk and calculate premiums.

Brick veneer construction is generally viewed favourably by insurers. It offers solid fire resistance and structural durability compared to timber or weatherboard exteriors, which can translate to more competitive premiums. Combined with a tiled roof, this property sits in a lower-risk construction category — tiles are durable and fire-resistant, though they can be more costly to repair after storm or hail events.

The slab foundation is standard for homes of this era and construction type, and doesn't typically attract any premium loading in South Australia's climate. Similarly, tile flooring throughout is considered low-risk from an insurance perspective, as it's durable and less susceptible to water damage than carpet or timber.

The home was built in 1980, which places it in a common age bracket for suburban Adelaide. Homes of this vintage are generally well-understood by insurers — old enough to have known characteristics, but not so old as to carry significant heritage or structural uncertainty risk. That said, ageing wiring, plumbing, and roofing materials can sometimes attract scrutiny, so it's worth ensuring your policy accurately reflects any updates or renovations made since construction.

Solar panels are increasingly common on Australian rooftops, but they do add complexity to a building insurance policy. Panels need to be covered for storm damage, hail, and fire, and their replacement cost contributes to the overall sum insured. Make sure your policy explicitly covers solar panels — not all standard policies do by default.

Ducted climate control is another feature that adds to the replacement cost of the home. These systems can be expensive to repair or replace, and insurers factor this into the building sum insured calculation.

With no pool and no cyclone risk designation, this property avoids two common sources of premium loading seen elsewhere in Australia.

---

Tips for Homeowners in Happy Valley

1. Review your sum insured carefully A $650,000 building sum insured is substantial. Use a building cost calculator to confirm this reflects the actual cost to rebuild your home — not its market value. Over-insuring adds unnecessary cost, while under-insuring can leave you significantly out of pocket after a claim.

2. Shop around within the suburb With 60 quotes sampled in Happy Valley, there's meaningful variation in pricing — from $787/year at the 25th percentile to $1,616/year at the 75th. That's nearly a $830 annual difference for comparable cover. Comparing multiple insurers is one of the most effective ways to reduce your premium.

3. Confirm your solar panels are covered Don't assume your solar system is automatically included. Ask your insurer specifically whether panels are covered under the building policy, what events are included, and whether there's a separate limit. This is especially relevant as panels age and their replacement cost evolves.

4. Consider your excess strategically Both the building and contents excess on this policy are set at $500. Opting for a higher excess (e.g., $1,000 or $2,000) can meaningfully reduce your annual premium. If you have a solid emergency fund and a low claims history, a higher excess may be a smart trade-off.

---

Find a Better Deal on CoverClub

Whether you're renewing your policy or comparing for the first time, CoverClub makes it easy to see how your quote stacks up. With real data from homeowners across Happy Valley and South Australia, you can make an informed decision rather than guessing. Get a home insurance quote today and find out if there's a better deal waiting for you.