If you own a free standing home in Hawkins Creek, QLD 4850, you already know that insuring a property in Far North Queensland comes with its own set of challenges — and costs. This article breaks down a real home and contents insurance quote for a three-bedroom, two-bathroom property in the area, examines how the premium stacks up against local, state, and national benchmarks, and offers practical tips to help you manage your insurance costs.

---

Is This Quote Fair?

The quote in question comes in at $26,876 per year (or $2,576/month) for combined home and contents cover, with a building sum insured of $646,000 and contents valued at $50,000. Both the building and contents excess are set at $1,000.

Our price rating for this quote is FAIR — around average for the Hawkins Creek area. That might sound reassuring at first glance, but it's worth putting that figure into context. "Around average" in Hawkins Creek is a very different benchmark from what most Australians pay elsewhere in the country.

The suburb average premium sits at $32,136 per year, with a median of $31,709. This quote lands below both of those figures and sits close to the 25th percentile for the suburb ($26,382), meaning it's actually on the more competitive end of the local market. In other words, while the premium is high in absolute terms, it is genuinely one of the better prices available for this type of property in this postcode.

---

How Hawkins Creek Compares

To appreciate just how significant the regional premium loading is, it helps to look at the broader picture.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Hawkins Creek (4850) | $32,136/yr | $31,709/yr |

| Queensland | $9,129/yr | $3,903/yr |

| National | $5,347/yr | $2,764/yr |

The gap is stark. The suburb average is roughly 3.5× the Queensland average and nearly 6× the national average. Even the median Hawkins Creek premium is more than eight times the national median.

This isn't a reflection of poor value from any particular insurer — it's a direct consequence of the elevated risk profile that comes with properties in this part of Queensland. You can explore the full breakdown of local pricing data on the Hawkins Creek suburb stats page, compare it against Queensland-wide figures, or view the national insurance statistics for broader context.

---

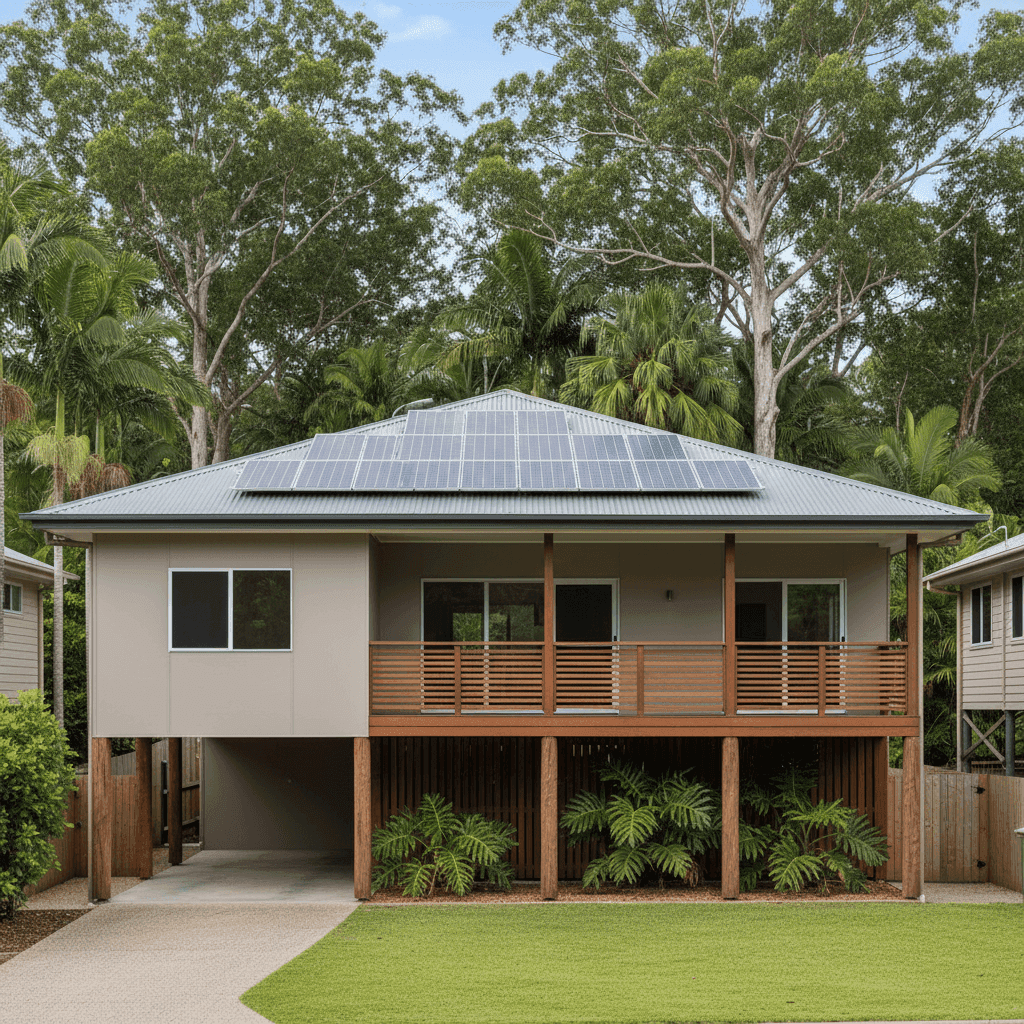

Property Features That Affect Your Premium

Several characteristics of this particular property have a meaningful influence on what insurers are willing to charge — for better and for worse.

Cyclone Risk Zone

This is the single biggest driver of premium costs in Hawkins Creek. The area falls within a designated cyclone risk zone, which significantly increases the likelihood of a major weather event causing structural damage. Insurers price this risk heavily, and it accounts for a large portion of the premium loading you see compared to southern Queensland or interstate properties.

Elevated Foundation (Stumps)

The home is elevated by at least one metre on stumps — a classic Queensland construction style. Elevation can actually work in a homeowner's favour in flood-prone areas, as it reduces the risk of inundation damage to the building's interior. Some insurers recognise this with modest premium reductions, particularly when flood cover is included.

Concrete External Walls & Colorbond Roof

Concrete walls offer strong resistance to wind and impact damage, which is a genuine advantage in cyclone country. Similarly, a steel Colorbond roof is considered more resilient than traditional tiles in high-wind events, and insurers generally view this construction type favourably. These features may be helping to keep this quote closer to the lower end of the local range.

Solar Panels & Ducted Climate Control

The presence of solar panels adds replacement value to the building sum insured and introduces a specific risk (storm or hail damage to panels). Ducted climate control is another fixed installation that increases the overall rebuild cost. Both are factored into the $646,000 building sum insured and contribute to the premium.

Timber & Laminate Flooring

While aesthetically appealing and common in elevated Queensland homes, timber and laminate flooring can be more susceptible to water damage than alternatives like tile. This is worth keeping in mind if you're assessing your contents and building cover limits.

---

Tips for Homeowners in Hawkins Creek

1. Don't Underinsure Your Home

With a rebuild cost of $646,000 for a 139 sqm home — roughly $4,647 per square metre — it's clear that construction costs in regional Far North Queensland are significantly higher than in metropolitan areas. Underinsuring to save on premiums can leave you severely out of pocket after a major event. Review your sum insured annually and factor in rising material and labour costs.

2. Harden Your Home Before Cyclone Season

Many insurers offer discounts or more competitive quotes for homes that have undergone cyclone mitigation upgrades — such as roof tie-downs, reinforced garage doors, and storm shutters. Given the property's Colorbond roof and concrete walls, you may already be in a strong position, but it's worth asking your insurer what additional measures could reduce your premium.

3. Compare Quotes Every Year

The local market for cyclone-zone properties can shift considerably between insurers from one year to the next. With a sample of 10 quotes in the Hawkins Creek area showing a range from roughly $26,382 (25th percentile) to $42,057 (75th percentile), there's clearly significant variation between providers. Running a fresh comparison each renewal period is one of the most effective ways to avoid overpaying.

4. Review Your Contents Cover Separately

At $50,000, the contents cover in this quote is relatively modest. If you've accumulated furniture, appliances, electronics, and personal items over several years, it's worth doing a proper stocktake to ensure you're not underinsured on contents. In the event of a cyclone or flooding, contents losses can be substantial.

---

Ready to Compare?

Whether you're renewing your policy or buying a home in Hawkins Creek for the first time, it pays to shop around. CoverClub makes it easy to compare home and contents insurance quotes from multiple providers in one place — so you can see exactly where your quote sits in the market and make an informed decision.

Get a home insurance quote now and find out if you're getting the best available price for your property.