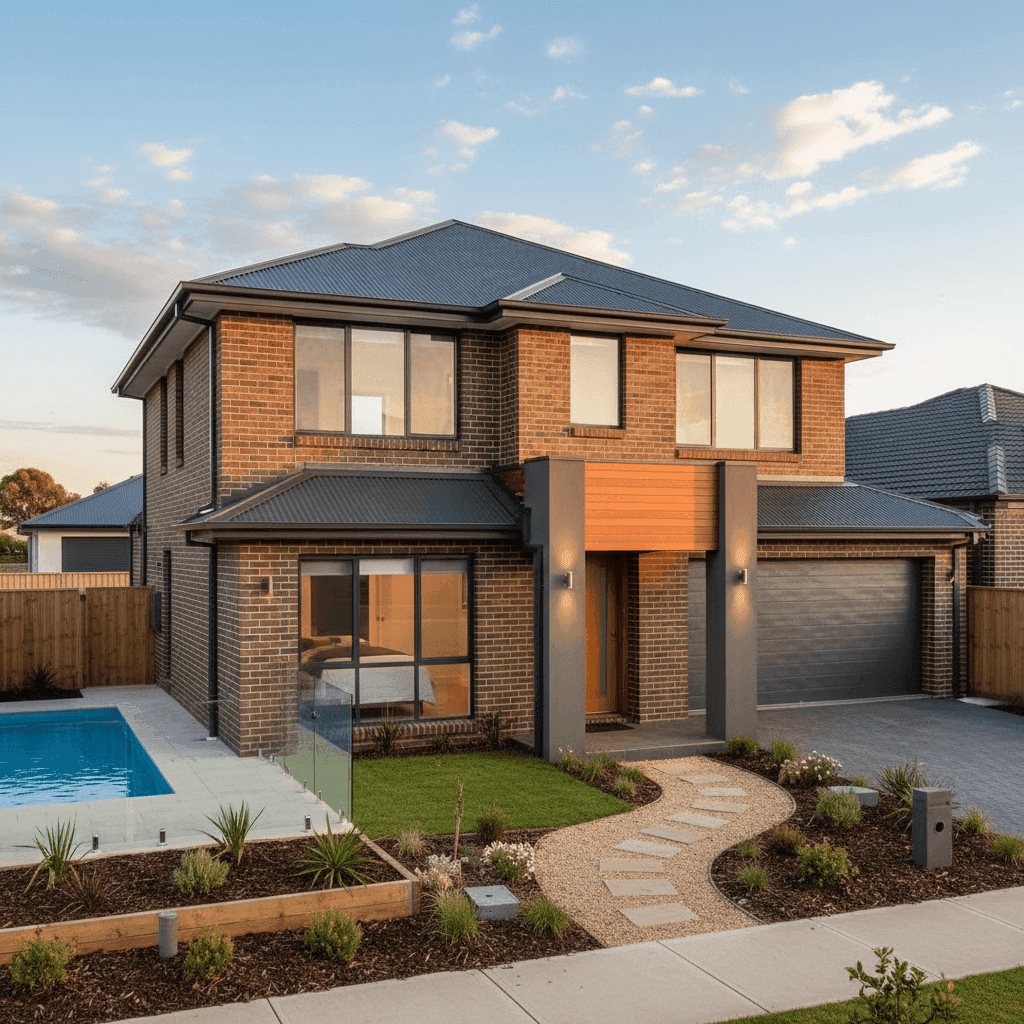

Home insurance in coastal South Australia can vary enormously depending on your property's size, features, and location. This article takes a close look at a real home and contents insurance quote for a five-bedroom free standing home in Henley Beach, SA 5022 — a popular beachside suburb just 11 kilometres west of the Adelaide CBD — and puts it in context against local, state, and national benchmarks.

---

Is This Quote Fair?

The quote in question sits at $9,348 per year (or $896/month), covering both building (sum insured: $1,432,000) and contents ($151,000), each with a $1,000 excess.

Our price rating for this quote is Expensive — Above Average, and the data backs that up. The suburb average premium in Henley Beach is just $2,225/year, meaning this quote comes in at more than four times what a typical property in the same postcode is paying. Even at the 75th percentile — where the pricier end of local quotes sit — the figure is only $2,097/year.

That said, context is everything. This is a large, high-value property with a building sum insured of $1.432 million. The contents cover alone adds $151,000 to the equation. When you're insuring a property of this size and replacement value, a higher premium is expected. The key question isn't just whether the dollar figure is high — it's whether it's proportionate to the risk and value being covered.

For homeowners who feel their quote may be inflated beyond what's justified, it's worth comparing offers from multiple insurers. You can get a quote and compare options at CoverClub to see whether a more competitive rate is available for the same level of cover.

---

How Henley Beach Compares

To understand where this quote sits in the broader landscape, here's a snapshot of average premiums across different comparison points:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Henley Beach (SA 5022) | $2,225/yr | $1,661/yr |

| Charles Sturt LGA | $1,695/yr | — |

| South Australia | $2,433/yr | $1,679/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out here. First, Henley Beach premiums are actually slightly below the South Australian state average, suggesting the suburb is not considered especially high-risk by insurers in general. The Charles Sturt LGA average of $1,695/year is even lower, reinforcing that this is a relatively affordable area to insure — for a typical property.

Second, the national average of $5,347/year is notably higher than both the suburb and state figures. This reflects the outsized influence of high-risk regions like North Queensland, cyclone-prone coastal areas, and flood-affected zones in other states. Henley Beach, by contrast, is not classified as a cyclone risk area, which is a meaningful factor in keeping baseline premiums lower for most local properties.

You can explore full suburb-level data on the Henley Beach insurance stats page, compare across South Australia, or view national home insurance benchmarks.

---

Property Features That Affect Your Premium

Several characteristics of this property directly influence what insurers charge. Here's how each one plays a role:

Size and Sum Insured

At 235 sqm with five bedrooms and two bathrooms, this is a substantial home. The building sum insured of $1,432,000 is the single biggest driver of the premium — larger replacement costs mean larger payouts in the event of a total loss, and insurers price accordingly.

Brick Veneer Walls and Colorbond Roof

Brick veneer construction is generally viewed favourably by insurers. It offers solid fire resistance and structural durability, which can help moderate premiums compared to timber-framed or clad exteriors. The steel Colorbond roof is similarly well-regarded — it's low maintenance, highly durable, and resistant to ember attack, making it a preferred roofing material in Australian conditions.

Slab Foundation

A concrete slab foundation is standard for homes built in this era and is considered low-risk from an insurance perspective. It reduces the likelihood of subsidence-related claims and is generally straightforward to assess.

Timber and Laminate Flooring

While attractive and common in above-average quality homes, timber and laminate flooring can be more expensive to repair or replace after water damage than tiles. This is a minor factor but one insurers do consider when pricing contents and building cover.

Swimming Pool

The presence of a pool adds to the insured value of the property and introduces additional liability considerations. Pool-related claims — from damage to the pool structure itself, or liability for injuries — contribute to a marginally higher premium.

Above-Average Fittings Quality

This property is noted as having above-average fittings, which means fixtures, appliances, and finishes are of higher quality and therefore more costly to replace. Insurers factor this into both building and contents valuations.

Ducted Climate Control

Ducted air conditioning systems are expensive to repair or replace and are included in the building sum insured. Their presence is reflected in the overall replacement cost estimate.

---

Tips for Homeowners in Henley Beach

Whether you're reviewing an existing policy or shopping for the first time, here are some practical steps to make sure you're getting the right cover at a fair price.

- Review your sum insured regularly. Building costs have risen sharply in recent years. If your sum insured hasn't been updated to reflect current construction costs, you may be underinsured — or overpaying for a figure that doesn't match today's rebuild reality. Use a qualified quantity surveyor or an online building cost calculator to verify your estimate.

- Compare quotes across multiple insurers. Premiums for the same property can vary by hundreds — or even thousands — of dollars between providers. Using a comparison platform like CoverClub makes it easy to see your options side by side without the legwork.

- Consider your excess strategically. Both the building and contents excess on this policy sit at $1,000. Opting for a higher voluntary excess can meaningfully reduce your annual premium — just make sure the amount is something you could comfortably cover out of pocket if you needed to make a claim.

- Check for discounts on bundled cover. Combining home and contents insurance under a single policy (as this quote does) often attracts a discount compared to purchasing them separately. Confirm with your insurer that you're receiving this benefit, and ask about any other loyalty or security-feature discounts that may apply.

---

Ready to Compare?

If you're a homeowner in Henley Beach or anywhere in South Australia, it pays to know what others are paying — and whether your current policy is genuinely competitive. CoverClub makes it simple to compare home and contents insurance quotes tailored to your property, so you can make a confident, informed decision. Don't just renew on autopilot — a few minutes of comparison could save you significantly.