Hepburn is a charming township nestled in the Macedon Ranges of central Victoria, known for its mineral springs, heritage character, and leafy surroundings. It's also an area where home insurance costs can vary quite significantly depending on your property's features and the insurer you choose. This article breaks down a recent home and contents insurance quote for a three-bedroom, free-standing home in Hepburn (VIC 3461) — and helps you understand whether the price stacks up.

---

Is This Quote Fair?

The quote in question comes in at $2,968 per year (or $284/month) for a combined home and contents policy, covering a building sum insured of $651,000 and $150,000 in contents. Both the building and contents excess are set at $2,000.

Our price rating for this quote is Expensive (Above Average) — meaning it sits above what most comparable properties in Hepburn are paying. To put that in perspective:

- The suburb average for Hepburn is $2,233/yr

- The suburb median is $2,141/yr

- The 75th percentile sits at $2,898/yr

This quote lands above the 75th percentile for the suburb, meaning it's pricier than at least three-quarters of quotes we've seen for similar properties in the area. That's a meaningful signal that there may be room to shop around.

That said, "expensive" is relative. The quote is still below the Victorian state average of $3,000/yr and well below the national average of $5,347/yr — so while it's on the higher end locally, it's not out of step with broader market trends.

---

How Hepburn Compares

Understanding how your premium fits into the bigger picture is key to making an informed decision. Here's a snapshot of where Hepburn sits across different benchmarks:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Hepburn (3461) | $2,233/yr | $2,141/yr |

| LGA (Macedon Ranges) | $2,890/yr | — |

| Victoria | $3,000/yr | $2,718/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out here. First, Hepburn's suburb-level premiums are notably lower than both the LGA average (Macedon Ranges at $2,890/yr) and the Victorian state average. This suggests that Hepburn itself may be considered a relatively lower-risk postcode within the region — though individual property factors can push premiums higher.

Second, the gap between the national average ($5,347/yr) and the national median ($2,764/yr) is striking. This tells us that a small number of very high-risk properties (think cyclone-prone areas of Queensland or flood-affected zones) are pulling the average up significantly. For a Victorian property like this one, the median is a more meaningful comparison point.

Based on 46 quotes collected for the Hepburn suburb, the 25th percentile sits at just $1,550/yr — meaning some homeowners in the area are paying considerably less. If your current quote is above the median, it's worth exploring your options.

---

Property Features That Affect Your Premium

Several characteristics of this property influence how insurers price the risk. Let's walk through the key ones:

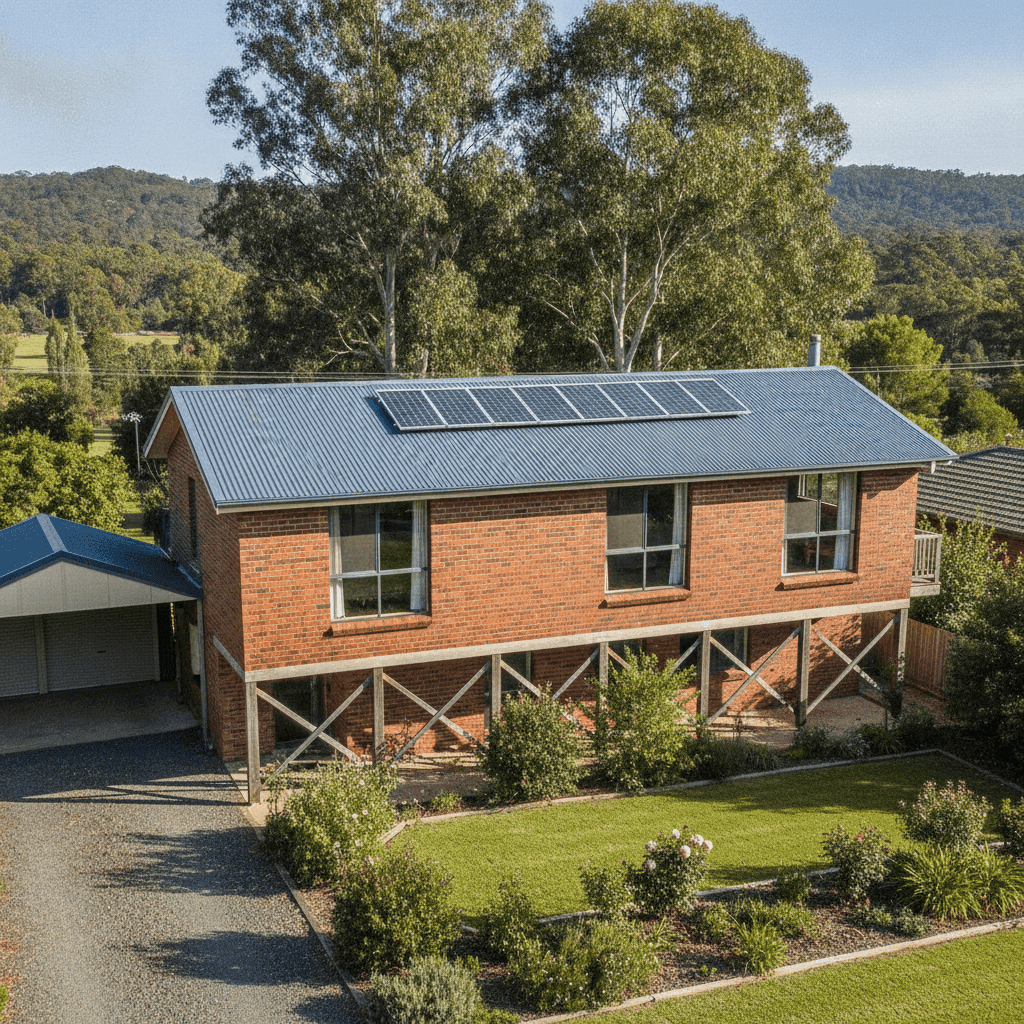

Double Brick Construction Double brick walls are generally viewed favourably by insurers. They're highly durable, fire-resistant, and less susceptible to storm damage than timber-framed alternatives. This should, in theory, work in your favour when it comes to premiums.

Steel / Colorbond Roof Colorbond steel roofing is another positive from an insurance perspective. It's lightweight, resistant to fire and corrosion, and performs well in high-wind conditions. Insurers typically regard it as lower risk compared to older tile or fibrous cement roofing.

Stump Foundation (Elevated Less Than 1m) The property sits on stumps and is elevated by less than one metre. While a stump foundation is common in older Victorian homes (this one was built in 1985), it can introduce some vulnerability to underfloor flooding and pest ingress. The slight elevation may also be a factor in how wind loading is assessed, though at under 1m it's unlikely to significantly inflate the premium.

Solar Panels Solar panels are increasingly common on Australian homes, but they do add to the replacement cost of a property. Insurers need to factor in the cost of replacing panels and associated equipment if they're damaged — which contributes to the higher building sum insured of $651,000.

Ducted Climate Control Ducted heating and cooling systems are a significant fixed asset within the home. Their inclusion increases the overall rebuild and replacement cost, which is reflected in the sum insured.

Carpet Flooring & Standard Fittings Standard-quality fittings and carpet flooring suggest a mid-range fit-out, which is appropriate for a 1985-built home. This keeps the contents and building valuations grounded rather than inflated by premium finishes.

No Pool, No Cyclone Risk Zone The absence of a pool removes a common source of liability and accidental damage claims. And being outside a designated cyclone risk area (as is the case for all of Victoria) means this property avoids one of the biggest premium drivers seen in northern Australia.

---

Tips for Homeowners in Hepburn

If you're looking to get better value on your home and contents insurance, here are four practical steps worth considering:

- Compare quotes from multiple insurers. The spread between the 25th percentile ($1,550/yr) and this quote ($2,968/yr) in Hepburn is substantial. Even moving from above the 75th percentile to near the median could save you $800 or more annually. Use a comparison tool like CoverClub to see what's available for your specific property.

- Review your sum insured carefully. At $651,000, the building sum insured is significant. Make sure this figure reflects the actual cost to rebuild your home (not its market value), including demolition, debris removal, and current construction costs. Over-insuring inflates your premium unnecessarily, while under-insuring can leave you exposed.

- Consider your excess level. This policy carries a $2,000 excess on both building and contents. Opting for a higher excess can reduce your annual premium — but only do this if you're comfortable covering that amount out of pocket in the event of a claim.

- Check what's included for solar panels and ducted systems. Not all policies automatically cover solar panel systems or ducted climate control as part of the building. Confirm these are explicitly listed in your policy schedule to avoid surprises at claim time.

---

Compare Home Insurance for Your Hepburn Property

Whether you're renewing your current policy or shopping for the first time, it pays to compare. CoverClub makes it easy to see real quotes for properties in Hepburn and across Victoria — so you can make a confident, informed decision. Get a quote today and find out if you're getting the best deal for your home.