If you own a free standing home in Hermit Park, QLD 4812, you already know that insuring it comes with some unique considerations. Located in Townsville's inner suburbs, Hermit Park sits in a region exposed to tropical weather, cyclone risk, and the broader pressures that drive North Queensland insurance premiums well above the national norm. This article breaks down a real building insurance quote for a large, character-filled home in the suburb — and helps you understand whether the price stacks up.

---

Is This Quote Fair?

The quote in question is $18,724 per year (or $1,787/month) for building-only cover on a six-bedroom, three-bathroom free standing home, with a $1,000 building excess and a sum insured of $1,899,000.

Our price rating for this quote is Expensive (Above Average).

To put that in perspective: the average building insurance premium across Hermit Park sits at $7,730 per year, with a median of $6,541. This quote comes in at more than 2.4 times the suburb average — a significant gap that warrants a closer look.

That said, "expensive" doesn't automatically mean "wrong." A premium this high is likely the result of several compounding risk factors specific to this property, rather than a case of simply overpaying. The key is understanding why the price is where it is, and whether there's room to bring it down without sacrificing meaningful cover.

---

How Hermit Park Compares

Zooming out beyond the suburb gives important context. Here's how premiums in Hermit Park sit relative to broader benchmarks:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Hermit Park (suburb) | $7,730/yr | $6,541/yr |

| Townsville LGA | $7,258/yr | — |

| Queensland (state) | $4,547/yr | $3,931/yr |

| National | $2,965/yr | $2,716/yr |

Even at the suburb average, Hermit Park homeowners are paying roughly 2.6 times the national median — a stark illustration of just how much cyclone-prone North Queensland inflates insurance costs. The Hermit Park suburb stats page shows the full spread of quotes in the area, from a 25th percentile of $4,964 up to a 75th percentile of $9,747 per year (based on a sample of 35 quotes).

Queensland as a whole averages $4,547/yr — already 53% above the national average of $2,965/yr. The further north you go in the state, the more pronounced that gap becomes.

---

Property Features That Affect Your Premium

Several characteristics of this particular property help explain why its premium lands so far above the suburb average.

Size and Sum Insured

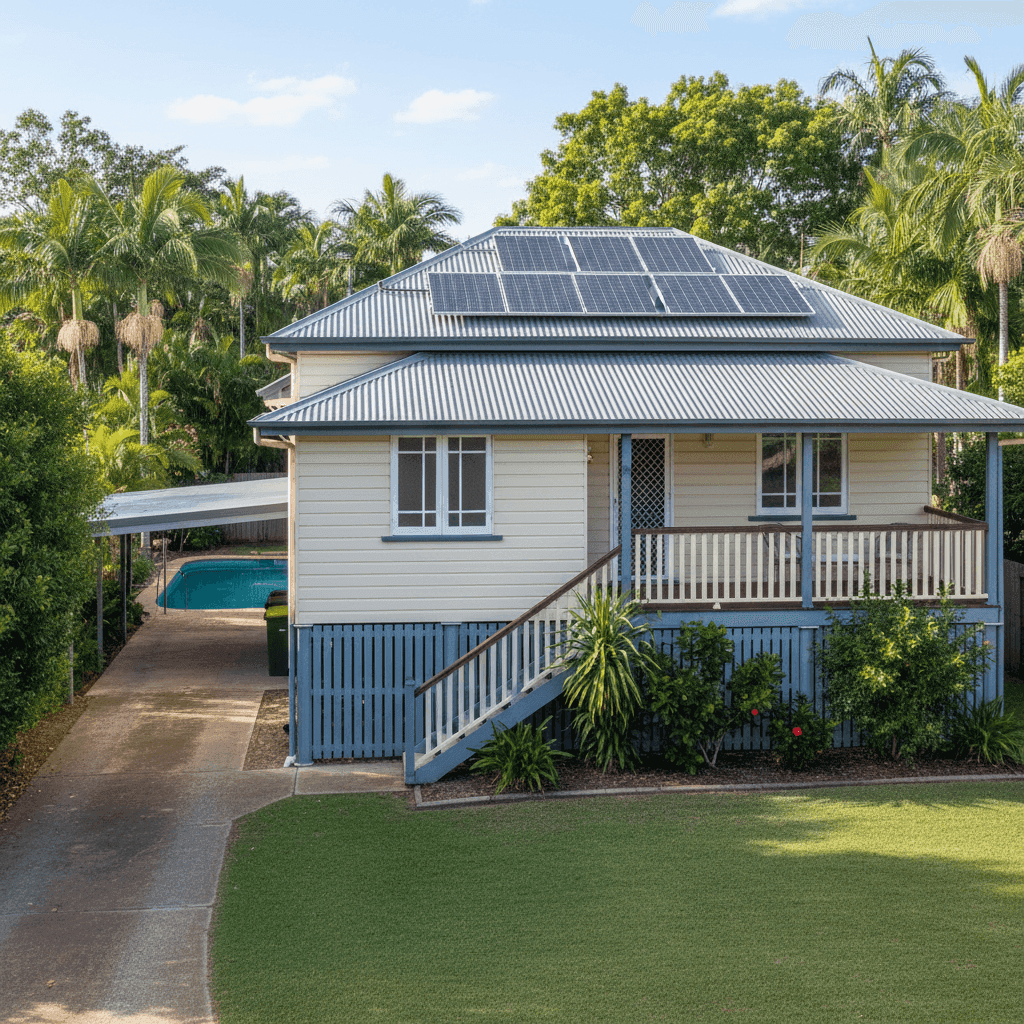

At 462 square metres with a sum insured of $1,899,000, this is a large home with a substantial rebuild cost. Insurers price building cover based heavily on the cost to reconstruct — and at nearly $1.9 million, this property sits in a high-value tier that commands a correspondingly high premium.

Age and Construction: Weatherboard Wood Walls

Built in 1940, this is a pre-war home with weatherboard timber walls. Older timber construction is viewed by insurers as higher risk — timber is more susceptible to fire, termite damage, and storm impact than modern brick or rendered construction. Weatherboard homes also tend to be more expensive to repair or replace like-for-like, particularly when heritage or character features are involved.

Cyclone Risk Area

Hermit Park falls within a designated cyclone risk zone, which is one of the single biggest premium drivers in North Queensland. Insurers apply significant loadings for properties in these areas due to the potential for catastrophic wind and water damage during a severe tropical cyclone event.

Steel/Colorbond Roof

On the positive side, a steel Colorbond roof is generally viewed favourably by insurers compared to older tile or fibrous cement alternatives. It's durable, lightweight, and performs well in high-wind conditions — which may be providing a modest offset to some of the other risk factors.

Pool and Solar Panels

The presence of a swimming pool adds liability and replacement cost considerations, while solar panels represent additional equipment that must be covered under the building sum insured. Both features contribute incrementally to the overall premium.

Above-Average Fittings

With above-average fittings quality, the internal finishes of this home — think quality joinery, fixtures, and flooring — increase the cost to rebuild to the same standard. Insurers factor this into their assessment of the sum insured and the overall risk profile.

---

Tips for Homeowners in Hermit Park

If you're a homeowner in Hermit Park — whether this is your quote or you're simply benchmarking — here are some practical steps to consider.

1. Review Your Sum Insured Carefully

A sum insured of $1,899,000 is substantial. Make sure it reflects the actual cost to rebuild your home (not its market value), including demolition, professional fees, and like-for-like construction. Overinsuring drives premiums up unnecessarily; underinsuring leaves you exposed. Consider using a quantity surveyor or your insurer's rebuild cost estimator to validate the figure.

2. Compare Multiple Quotes

With a premium this far above the suburb average, it's absolutely worth shopping around. Different insurers assess cyclone risk, timber construction, and property age very differently. Using a comparison platform like CoverClub lets you see multiple quotes side by side and identify whether a better deal exists for the same level of cover.

3. Cyclone-Proof Your Home Where Possible

Some insurers offer premium discounts for homes that meet certain cyclone mitigation standards — such as upgraded roof tie-downs, storm shutters, or compliance with modern wind-resistance requirements. Given this home was built in 1940, a structural assessment and targeted upgrades could potentially reduce your risk rating over time.

4. Consider a Higher Excess

The current building excess is set at $1,000. Opting for a higher voluntary excess (say, $2,500 or $5,000) can meaningfully reduce your annual premium. This strategy works best for homeowners who have the financial buffer to absorb a larger out-of-pocket cost in the event of a claim — and who are primarily seeking cover for major, catastrophic events rather than minor repairs.

---

Ready to Compare?

Whether you're looking to benchmark this quote or find a better deal entirely, CoverClub makes it easy to compare home insurance options tailored to your property and location. Get a quote today and see how your premium stacks up against real data from homes just like yours in Hermit Park and across Queensland.