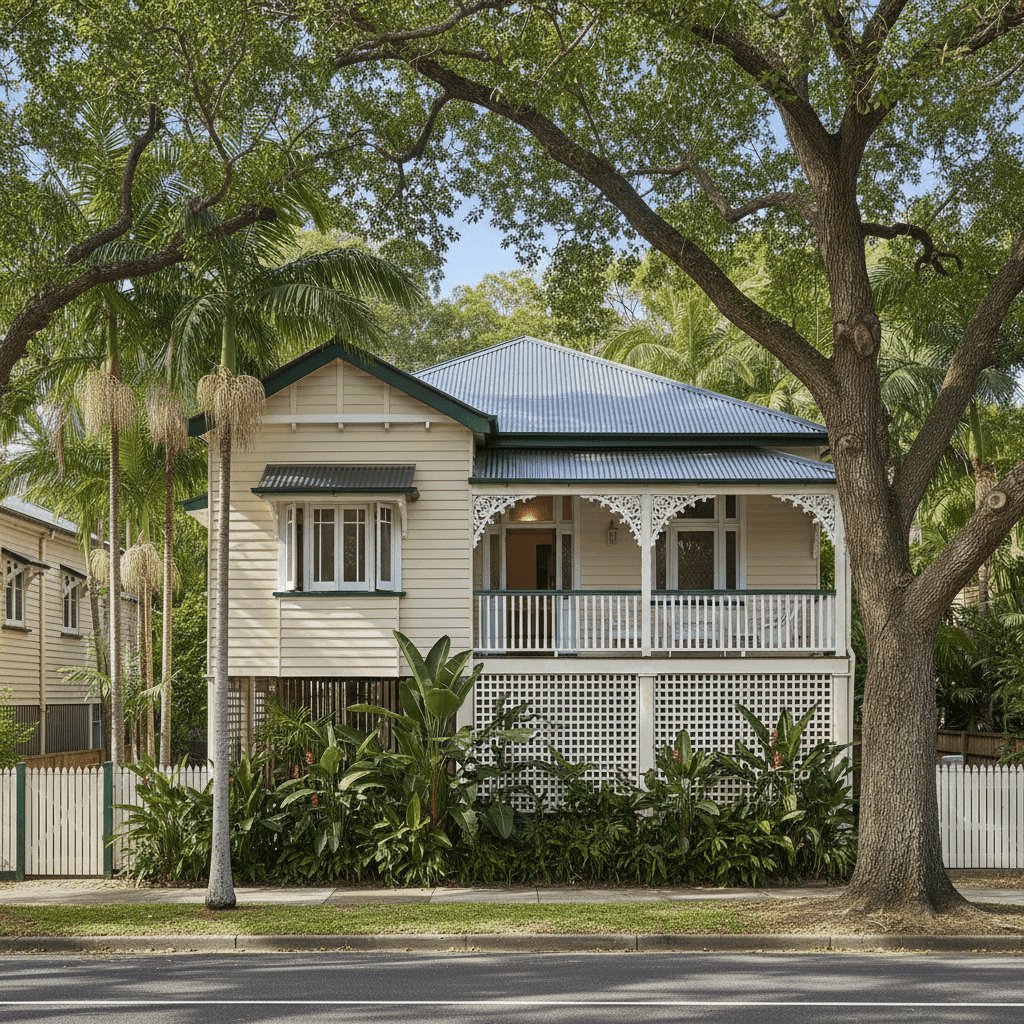

Herston is one of Brisbane's most characterful inner-north suburbs, sitting just a kilometre from the CBD and home to a rich collection of classic Queensland architecture. If you own a free standing home here — particularly one of the older weatherboard Queenslanders that define the streetscape — understanding what you should be paying for home and contents insurance is genuinely valuable. This article breaks down a real quote for a 4-bedroom, 2-bathroom property in Herston (postcode 4006) and puts the numbers in context against suburb, state, and national benchmarks.

---

Is This Quote Fair?

The annual premium for this property came in at $8,606 per year (or $843/month), covering both building and contents. The building is insured for $1,128,000 and contents for $249,000, with a $3,000 building excess and $1,000 contents excess.

CoverClub's pricing engine has rated this quote as FAIR — around average for the suburb. That's a reasonable result, but "average" in Herston carries some nuance. The suburb average premium sits at $5,960/yr, and the median is $4,369/yr — both noticeably lower than this quote. However, the 75th percentile for Herston reaches $9,037/yr, which means roughly one in four properties in this area attracts a premium above $9,000. At $8,606, this quote is sitting in the upper band of the local range, but still comfortably below the 75th percentile threshold.

The elevated sum insured — $1,128,000 for the building alone — is a significant driver here. A 235 sqm home built in 1930 with above-average fittings, weatherboard construction, and a polished interior commands a higher rebuild cost than a standard brick-and-tile suburban home. This isn't a case of being overcharged; it's a reflection of what it genuinely costs to rebuild a well-appointed heritage-style home in inner Brisbane.

---

How Herston Compares

Putting this quote into a broader geographic context helps clarify the picture. You can explore the full data on the Herston suburb insurance stats page, but here's a quick summary:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Herston (4006) | $5,960/yr | $4,369/yr |

| Brisbane LGA | $4,485/yr | — |

| Queensland | $4,547/yr | $3,931/yr |

| National | $2,965/yr | $2,716/yr |

A few things stand out. First, Herston premiums are already running well above Queensland state averages and more than double the national median. This reflects the concentration of older, higher-value homes in the suburb, many of which are elevated timber structures that carry unique risk profiles. Second, the gap between the suburb average ($5,960) and the 75th percentile ($9,037) is wide — indicating significant variation in the types of properties and coverage levels being quoted. A 4-bedroom home with above-average fittings and a high sum insured naturally skews toward the upper end.

The Brisbane LGA average of $4,485/yr confirms that Herston sits above the broader city norm, which is consistent with the suburb's premium property values and older housing stock.

---

Property Features That Affect Your Premium

Several characteristics of this property have a meaningful impact on the premium, and it's worth understanding each one.

Age and construction (built 1930, weatherboard walls): Older homes cost more to insure. Sourcing period-appropriate materials, engaging tradespeople familiar with heritage construction, and meeting modern building codes during a rebuild all add cost. Weatherboard timber walls are also more susceptible to fire, moisture damage, and pest ingress than brick or rendered masonry — factors insurers price into their risk models.

Elevated foundations (poles, at least 1m high): This is the classic Queensland design, and it's a double-edged sword. Elevation provides excellent flood resilience by keeping the living areas above ground-level inundation, but it also means the subfloor structure — bearers, stumps, joists — is exposed and must be maintained. Insurers account for the additional complexity of repairing or rebuilding an elevated home.

Timber and laminate flooring: Combined with the elevated structure, timber flooring adds to the rebuild cost estimate. High-quality timber floors in a 235 sqm home represent a significant line item in any reinstatement quote.

Above-average fittings quality: Kitchens, bathrooms, and fixtures that are above average in quality cost more to replace like-for-like. This is reflected in both the building sum insured and the $249,000 contents valuation.

Steel/Colorbond roof: On the positive side, a Colorbond roof is a modern, durable material that performs well in Queensland's climate. It's resistant to corrosion, handles heat well, and is generally viewed favourably by insurers compared to older roofing materials like terracotta tiles or asbestos sheeting sometimes found on homes of this era.

Ducted climate control: A ducted air conditioning system adds to the sum insured for both building (the ductwork and ceiling cassettes) and potentially contents (the internal units). It's a meaningful contributor to the overall insured value.

---

Tips for Homeowners in Herston

1. Review your sum insured regularly — and don't underinsure. Construction costs in Brisbane have risen sharply in recent years. A $1,128,000 building sum insured for a 235 sqm heritage home with above-average fittings may sound high, but underinsurance is a serious risk. Use a quantity surveyor or your insurer's rebuild cost calculator annually to ensure your coverage keeps pace with actual reinstatement costs.

2. Shop around — even if your current quote seems fair. A "fair" rating means you're around the market average, not that you're getting the best available deal. With 24 quotes sampled in this suburb, there's genuine variation in what different insurers charge for similar properties. Compare quotes on CoverClub to see whether a better rate is available without sacrificing cover quality.

3. Maintain your subfloor and stumps. Elevated homes on timber stumps require periodic inspection and maintenance. Deteriorating stumps or bearers can affect the structural integrity of the home and may complicate insurance claims if neglect is identified as a contributing factor. Budget for a licensed building inspector to check the subfloor every few years.

4. Document your contents thoroughly. With $249,000 in contents cover, having a detailed home inventory — including photos, receipts, and serial numbers for high-value items — makes the claims process significantly smoother. Store this documentation in the cloud or offsite so it's accessible even if the property is damaged.

---

Compare Your Quote With CoverClub

Whether you're renewing your existing policy or shopping for the first time, it pays to benchmark your premium against the market. CoverClub aggregates real quote data from across Australia so you can see exactly where your property sits relative to your suburb, city, and state. Get a home insurance quote today and find out if you're getting a fair deal — or if there's room to do better.