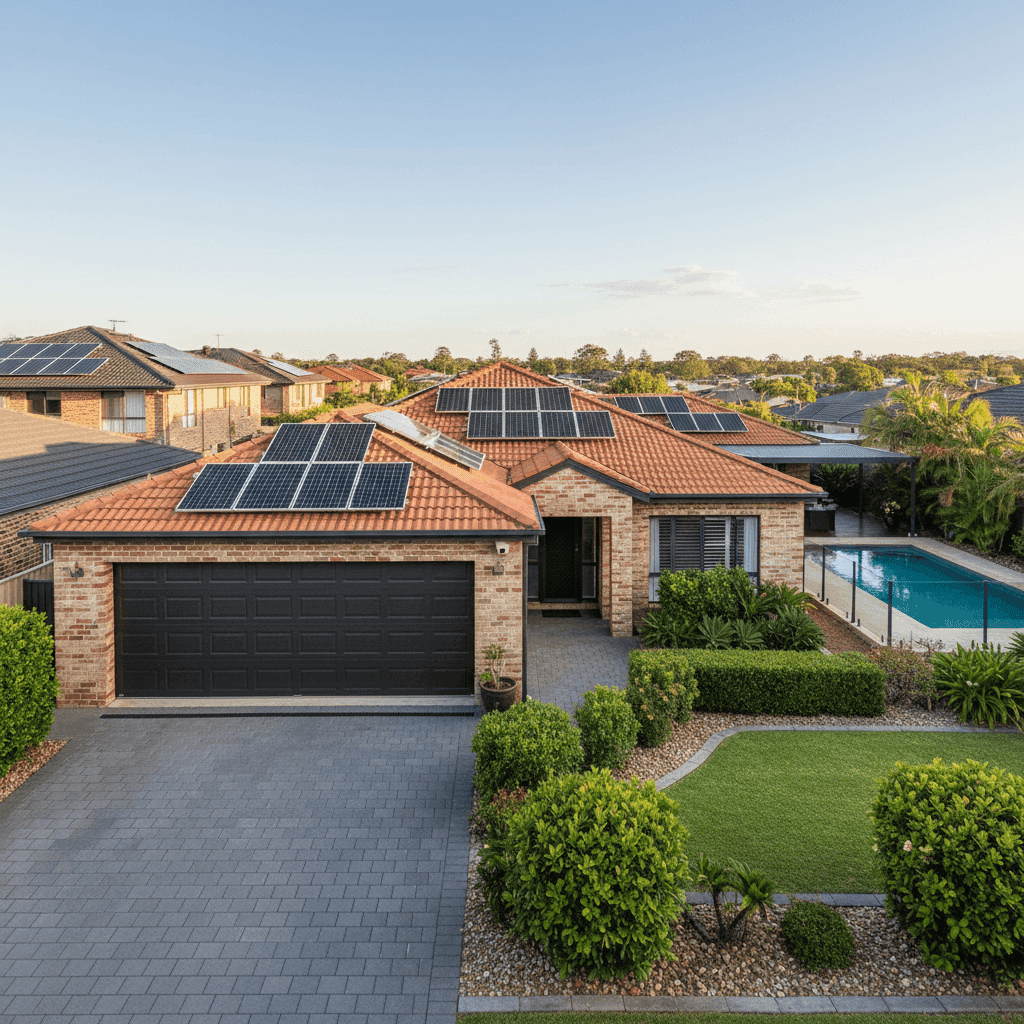

If you own a free standing home in Hollywell, QLD 4216, you're sitting in one of the Gold Coast's quieter residential pockets — a suburb that blends suburban comfort with proximity to the Broadwater. Like most Queensland homeowners, understanding what you're paying for building insurance (and whether it's a fair deal) can be surprisingly tricky. This article breaks down a recent building-only insurance quote for a 3-bedroom, 2-bathroom brick veneer home in Hollywell, and puts the numbers in context against suburb, state, and national benchmarks.

---

Is This Quote Fair?

The quote in question comes in at $2,969 per year (or $285/month) for building-only cover on a home insured for $501,000, with a building excess of $5,000. Our analysis rates this quote as CHEAP — below the suburb average — which is genuinely good news for the homeowner.

To put that in perspective: the suburb average for Hollywell sits at $4,526/year, meaning this quote is roughly $1,557 cheaper than what the typical Hollywell homeowner is paying annually. That's a meaningful saving — enough to cover a decent chunk of a home maintenance bill or a family holiday.

It's worth noting that a $5,000 building excess is on the higher side, and that does contribute to the lower premium. A higher excess means you're agreeing to cover more out-of-pocket before the insurer steps in, so it's a trade-off worth understanding. If your home were to suffer minor damage — say, a small section of roof tiles dislodged in a storm — you'd need to weigh whether a claim is even worth making at that excess level.

That said, for homeowners who are financially comfortable absorbing smaller repair costs and want to protect against major structural events, a higher excess paired with a lower premium can be a smart strategy.

---

How Hollywell Compares

Zooming out to the broader picture reveals some interesting dynamics. Here's how this quote stacks up across different geographic benchmarks:

| Benchmark | Premium |

|---|---|

| This Quote | $2,969/yr |

| Hollywell Suburb Average | $4,526/yr |

| Hollywell Suburb Median | $4,352/yr |

| Hollywell 25th Percentile | $3,252/yr |

| QLD State Average | $9,129/yr |

| QLD State Median | $3,903/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

| Gold Coast LGA Average | $8,161/yr |

A few things stand out here. First, the QLD state average of $9,129/year is extraordinarily high — this is largely driven by cyclone-prone regions in Far North Queensland, where premiums can be eye-watering. The state median of $3,903 gives a more realistic picture of what most Queenslanders are paying, and this quote sits comfortably below even that figure.

Compared to the Gold Coast LGA average of $8,161/year, this quote looks especially competitive. The LGA average is heavily influenced by waterfront and high-risk properties across the broader Gold Coast region, so Hollywell's suburb-level numbers — and this quote in particular — paint a more favourable picture for inland or lower-risk streets.

At the national level, the average premium of $5,347 reflects the wide variance across Australia, from low-risk metro suburbs to flood and cyclone-affected regional areas. The national median of $2,764 is actually slightly below this quote, which suggests that while this is a good deal locally, it's broadly in line with what many Australian homeowners pay nationally.

You can explore more localised data on the Hollywell suburb stats page, compare against all of Queensland, or view national home insurance trends.

---

Property Features That Affect Your Premium

Several characteristics of this particular property influence what insurers are willing to charge — for better and for worse.

Brick Veneer Walls & Tiled Roof Brick veneer construction with a tiled roof is generally viewed favourably by insurers. Brick veneer offers solid weather resistance and fire performance, while tiles are more durable than Colorbond or corrugated iron in many scenarios. This combination tends to attract more competitive premiums compared to weatherboard or fibro homes.

Slab Foundation A concrete slab foundation is the norm for Queensland homes built from the 1990s onward, and insurers generally regard it as low-risk compared to older timber stumped homes, which can be vulnerable to subsidence, termite damage, and moisture ingress.

Construction Year: 1990 At around 35 years old, this home sits in a middle ground — old enough that some components (roof tiles, plumbing, electrical) may be approaching end-of-life, but modern enough to have been built under more rigorous building codes than pre-1980s homes. Insurers may factor in age-related wear when assessing risk.

Swimming Pool A pool adds liability considerations to a property. While it doesn't dramatically affect building premiums, it's a feature that increases the overall replacement cost of the property and can nudge premiums slightly higher. Ensuring your sum insured accurately accounts for the pool, fencing, and associated equipment is important.

Solar Panels Solar panels are an increasingly common feature on Queensland homes, and most modern building policies cover them as a fixed fixture. However, it's worth confirming with your insurer that your panels and inverter are explicitly covered under the building sum insured, particularly for storm or hail damage.

Ducted Climate Control Ducted air conditioning is a significant fixed asset. Like solar, it should be factored into your building sum insured to avoid being underinsured in the event of a total loss.

---

Tips for Homeowners in Hollywell

1. Review Your Sum Insured Annually With construction costs rising sharply across Queensland, the cost to rebuild a 139 sqm brick veneer home has increased significantly in recent years. Make sure your $501,000 sum insured reflects current labour and materials costs — underinsurance is one of the most common and costly mistakes homeowners make.

2. Understand Your Excess Before You Claim A $5,000 building excess is a meaningful financial commitment. Before lodging a claim for minor damage, get a repair quote first. If the repair cost is only marginally above the excess, it may not be worth claiming — and avoiding unnecessary claims can help keep your premium down at renewal.

3. Confirm What's Covered Under Building vs. Contents This policy is building-only, which means your personal belongings, furniture, and portable items are not covered. If you haven't already, consider whether a separate contents policy makes sense for your household. Even a basic contents policy can provide valuable protection for appliances, clothing, and valuables.

4. Check Your Pool and Solar Are Adequately Covered Ask your insurer directly whether your pool, solar panels, and ducted system are included in the building sum insured. Some policies treat certain fixtures as optional add-ons or cap payouts for specific items. Knowing this upfront avoids nasty surprises at claim time.

---

Compare Your Own Quote

Whether you're renewing your existing policy or shopping for the first time, it pays to compare. The difference between the cheapest and most expensive quotes in Hollywell spans thousands of dollars per year — and the right cover isn't always the cheapest or the most expensive option. It's the one that fits your property, your risk tolerance, and your budget.

Get a home insurance quote at CoverClub and see how your property stacks up against real data from your suburb and beyond.