If you own a free standing home in Hoppers Crossing, VIC 3029, you're probably wondering whether the insurance premium you've been quoted is reasonable — or whether you're leaving money on the table. This analysis breaks down a real home and contents insurance quote for a four-bedroom brick veneer home in the suburb, comparing it against local, state, and national benchmarks so you can make a confident, informed decision.

---

Is This Quote Fair?

The quoted annual premium for this property is $1,630 per year (or $169 per month), covering a building sum insured of $758,000 and contents valued at $50,000. The building excess sits at $3,000 and the contents excess at $1,000.

Our price rating for this quote is FAIR — Around Average.

That assessment holds up under scrutiny. The premium lands above the Hoppers Crossing suburb median of $1,462/yr and slightly above the suburb average of $1,531/yr, but it falls comfortably within the middle range of what locals are paying. The suburb's 75th percentile sits at $1,894/yr, meaning roughly a quarter of comparable homes in the area attract higher premiums than this quote. On the flip side, the 25th percentile is $1,052/yr — so there is room to potentially reduce costs by shopping around.

In short: this isn't a bargain, but it's not an outlier either. It's a reasonable starting point that deserves a closer look before you commit.

---

How Hoppers Crossing Compares

One of the most telling aspects of this quote is just how favourably Hoppers Crossing stacks up against broader benchmarks.

| Benchmark | Average Premium |

|---|---|

| Hoppers Crossing (suburb avg) | $1,531/yr |

| LGA — Melton | $2,509/yr |

| Victoria (state avg) | $3,000/yr |

| National average | $5,347/yr |

The quoted premium of $1,630 is nearly half the Victorian state average of $3,000/yr and a fraction of the national average of $5,347/yr. Even compared to the broader Melton LGA average of $2,509/yr, Hoppers Crossing homeowners are getting a notably better deal.

Much of this comes down to risk profile. Hoppers Crossing is not classified as a cyclone risk area, sits away from high bushfire zones, and benefits from relatively modern suburban infrastructure. These factors collectively keep premiums lower than many other parts of Victoria and well below coastal or regional areas that dominate the national average.

For context, the national median of $2,764/yr and Victoria's median of $2,718/yr both sit well above this quote — reinforcing that Hoppers Crossing is genuinely one of the more affordable suburbs for home insurance in Australia.

---

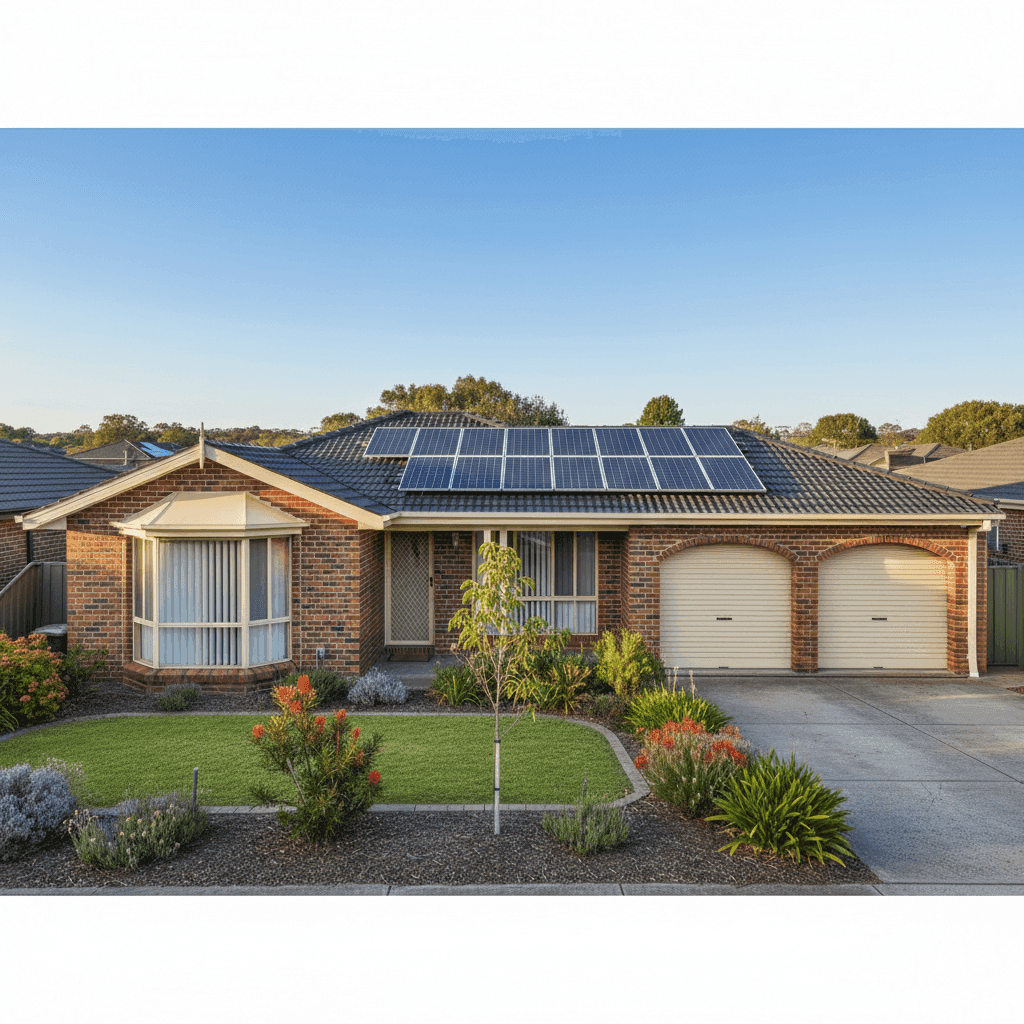

Property Features That Affect Your Premium

Every property tells its own insurance story, and this one has a number of features that directly influence what you'll pay.

Brick Veneer Walls & Tiled Roof

Brick veneer construction is generally viewed favourably by insurers. It offers solid fire resistance and structural durability compared to timber or cladding alternatives. Combined with a tiled roof — another low-risk, long-lasting material — this home presents a relatively low-risk profile from a building perspective.

Slab Foundation

A concrete slab foundation is standard for homes built in the 1990s across Victoria's outer suburbs. It's structurally stable and less susceptible to the subsidence or moisture issues that can affect older homes with strip or pier footings.

Built in 1996

At around 28–29 years old, this home is mature but not aged. Homes from the mid-1990s are generally well-regarded by insurers — they're past the era of some older wiring or plumbing concerns, yet old enough that certain systems (hot water, roof tiles, electrical) may be approaching the end of their service life. It's worth ensuring your building sum insured reflects current rebuild costs.

Solar Panels

The presence of solar panels adds a layer of complexity to your cover. Panels are typically covered under the building policy, but it's important to confirm this with your insurer — particularly for damage from storms, hail, or electrical faults. Some policies may require specific endorsements.

Ducted Climate Control

Ducted heating and cooling systems are expensive to repair or replace. Their inclusion in the property is a factor that can nudge premiums slightly higher, as they represent a significant asset within the building structure.

Timber & Laminate Flooring

While attractive and popular, timber and laminate floors can be costly to replace after water damage events. This is worth keeping in mind when assessing whether your contents and building cover limits are adequate.

Standard Fittings

Standard-quality fittings mean the insurer isn't pricing in high-end finishes or bespoke fixtures, which helps keep the premium more manageable compared to properties with premium or luxury specifications.

---

Tips for Homeowners in Hoppers Crossing

1. Review Your Building Sum Insured Annually

At $758,000, the building sum insured for this property needs to keep pace with rising construction costs. Melbourne's outer western suburbs have seen significant growth in labour and materials costs post-pandemic. Underinsurance is a real risk — use a building cost calculator or speak with a quantity surveyor to validate your figure each year.

2. Shop Around Within the Suburb's Price Range

With a 25th percentile of $1,052/yr and a 75th percentile of $1,894/yr among 132 quotes sampled in Hoppers Crossing, there's meaningful variation in what insurers charge for similar properties. A few hours of comparison shopping could save you hundreds annually.

3. Clarify Solar Panel Coverage

Before renewing or switching policies, ask your insurer explicitly: are the solar panels covered under the building policy? What events are included — storm, hail, fire, accidental damage? Some insurers treat panels as a separate item or apply different excess amounts.

4. Consider Increasing Your Excess to Lower Premiums

The current building excess is $3,000 — already on the higher side, which likely helps reduce the annual premium. If cash flow allows, opting for a higher voluntary excess can further reduce what you pay upfront each year. Just ensure you could comfortably cover that amount if a claim arose.

---

Compare Your Options with CoverClub

Whether this quote is the right fit depends on more than just the price — policy inclusions, claim handling reputation, and cover limits all matter. The best way to know if you're getting value is to compare. At CoverClub, you can get a home insurance quote in minutes and see how different insurers price your specific property. Don't settle for the first number you see — a fairer deal could be just a few clicks away.