If you own a free standing home in Horsley, NSW 2530, you've probably wondered whether your home insurance premium is reasonable — or whether you're paying more than you need to. Horsley is a well-established suburb in the Wollongong local government area, popular with families thanks to its quiet streets, good schools, and proximity to the coast. In this article, we break down a real home and contents insurance quote for a four-bedroom brick veneer home in the area and put the numbers in context so you can make a more informed decision.

---

Is This Quote Fair?

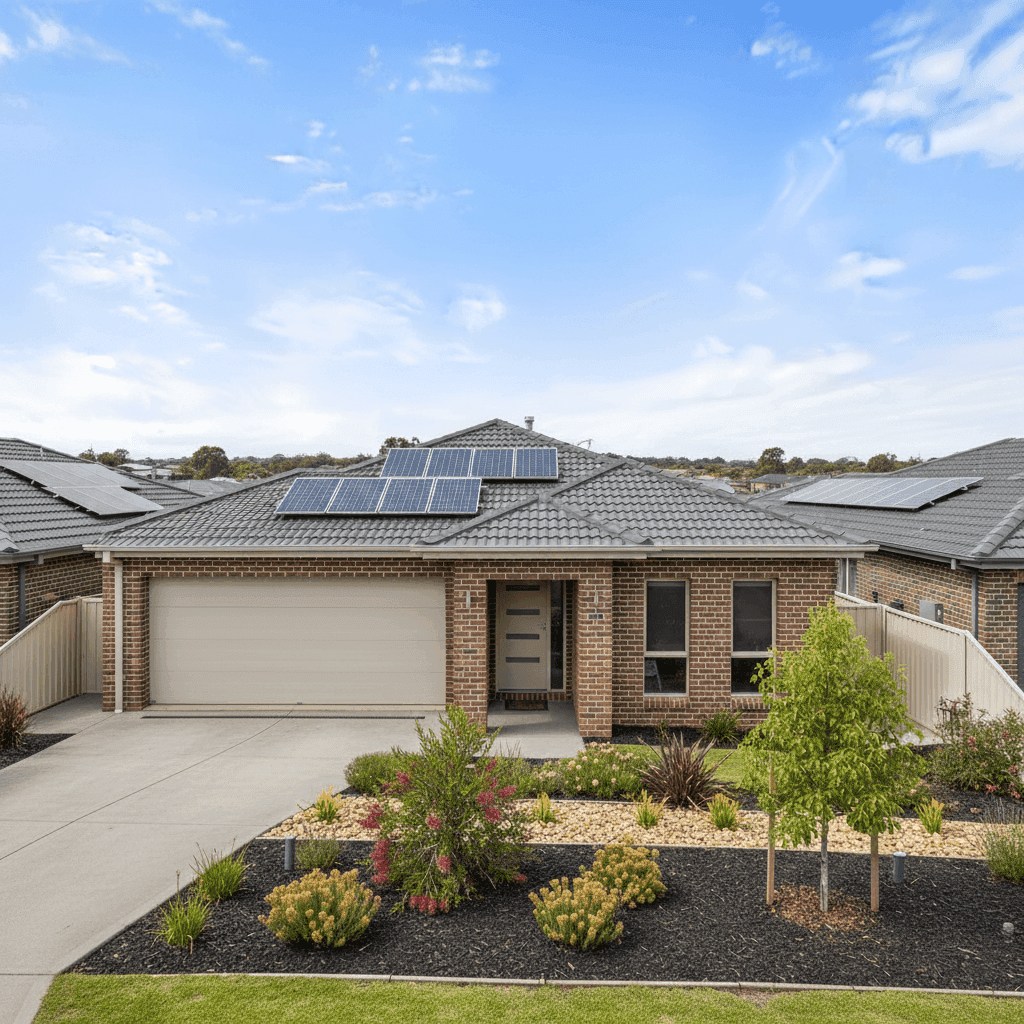

The quote in question comes in at $2,295 per year (or $220/month) for combined home and contents cover, with a building sum insured of $627,000 and contents valued at $104,000. Both the building and contents excess are set at $1,000.

Our price rating for this quote is FAIR — Around Average. That assessment is backed up by the data. The suburb average premium for Horsley sits at $2,282 per year, meaning this quote lands almost exactly on the local average. It's comfortably within the typical range for the area, which runs from around $969/yr at the 25th percentile up to $2,684/yr at the 75th percentile.

So while this isn't the cheapest quote available in the suburb, it's by no means an outlier. For a well-appointed four-bedroom home with solar panels and ducted climate control — both of which add to the insured value — a premium in this range is understandable.

---

How Horsley Compares

To really appreciate what this quote means, it helps to zoom out and look at the broader picture. Here's how Horsley stacks up against state and national benchmarks:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Horsley (NSW 2530) | $2,282/yr | $1,669/yr |

| New South Wales | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

| Wollongong LGA | $2,751/yr | — |

A few things stand out here. The NSW state average of $9,528/yr looks alarming at first glance, but it's heavily skewed by high-risk and high-value properties across the state — the median of $3,770/yr is a more representative figure for typical NSW homeowners. Even so, Horsley's median of $1,669/yr sits well below the state median, suggesting the suburb is considered relatively low-risk by insurers.

Compared to the national median of $2,764/yr, this quote of $2,295/yr is actually below the national median — a positive sign for Horsley homeowners. The Wollongong LGA average of $2,751/yr also provides useful local context; this quote comes in beneath that figure, which is reassuring.

It's worth noting that the suburb data is based on a sample of 21 quotes, so while directionally useful, the averages can shift as more data comes in. You can explore the latest figures on the Horsley suburb stats page.

---

Property Features That Affect Your Premium

Every home is different, and insurers price risk based on a range of property characteristics. Here's how the features of this particular home are likely influencing the premium:

Brick Veneer Walls & Tiled Roof Brick veneer is one of the most common external wall types in Australian suburban homes, and insurers generally view it favourably. It offers solid fire resistance and durability. Combined with a tiled roof — another low-risk roofing material — this home presents a relatively standard risk profile from a construction standpoint.

Slab Foundation A concrete slab foundation is typical for homes built around the year 2000 in NSW. It's generally considered stable and less susceptible to subsidence issues compared to older pier-and-beam styles, which can work in your favour at claims time.

Solar Panels The presence of solar panels adds to the replacement cost of the home, which is reflected in the building sum insured. Insurers need to account for the cost of replacing panels if they're damaged by a storm, fire, or other insured event. It's important to ensure your building sum insured covers the full replacement value of the system.

Ducted Climate Control Ducted air conditioning systems are a significant fixed asset within the home. As part of the building's permanent fixtures, they're typically covered under the building component of a home and contents policy — and their value contributes to the overall sum insured.

No Pool, Standard Fittings The absence of a pool keeps the risk profile straightforward. Standard-quality fittings also mean there's less exposure to high-cost replacements for things like premium benchtops or designer fixtures, which can push premiums higher in more prestige properties.

Year Built: 2000 A home built in 2000 benefits from modern building codes that were in place at the time of construction. It's old enough to have some wear but not so old that it carries the elevated risk associated with homes built in the 1960s or 70s.

---

Tips for Homeowners in Horsley

Whether you're renewing your policy or shopping around for the first time, here are some practical steps to make sure you're getting the right cover at the right price.

- Review your building sum insured regularly. Construction costs have risen significantly in recent years. If your sum insured hasn't been updated to reflect current rebuild costs, you could be underinsured. Use a building calculator or speak with a quantity surveyor to get an accurate figure.

- Check that your solar panels are covered. Not all policies automatically include solar panel systems under the building cover. Read your Product Disclosure Statement (PDS) carefully to confirm they're included — and at the right value.

- Consider the impact of your excess on your premium. A $1,000 excess is fairly standard, but opting for a higher excess can reduce your annual premium. If you have a healthy emergency fund and are unlikely to make small claims, this trade-off may be worth exploring.

- Compare quotes before renewing. Loyalty doesn't always pay in insurance. Premiums can vary significantly between providers for the same level of cover. Using a comparison tool means you can see multiple quotes side by side without having to contact each insurer individually.

---

Ready to Compare?

If you're a homeowner in Horsley or anywhere else in Australia, it pays to shop around. CoverClub makes it easy to compare home and contents insurance quotes from multiple providers in one place — so you can be confident you're getting value for money. Get a quote today and see how your current premium stacks up.