Howard is a quiet regional town in Queensland's Fraser Coast region, sitting roughly halfway between Bundaberg and Maryborough. It's the kind of place where properties are affordable, the community is tight-knit, and home insurance costs can vary dramatically depending on who you ask. This article breaks down a real home and contents insurance quote for a 2-bedroom free standing home in Howard (QLD 4659) — and puts it in context against local, state, and national benchmarks so you can judge whether you're getting a fair deal.

---

Is This Quote Fair?

The short answer: yes — this is a genuinely competitive quote.

At $2,536 per year (or $236/month), this home and contents policy covers a building sum insured of $412,000 and $45,000 in contents, with a $1,000 building excess and $500 contents excess. CoverClub's pricing algorithm rates this quote as CHEAP — below the suburb average — and the numbers back that up convincingly.

To put it plainly, this quote comes in at less than half the suburb average of $5,999/year. Even measured against the suburb's 25th percentile — meaning only 25% of quotes in Howard are cheaper — this policy at $2,536 sits well below the $3,921/year mark. That's a strong result by any measure.

It's worth noting that the suburb sample size is 15 quotes, which is a reasonable snapshot for a town of Howard's size. The spread in that data is wide — from $3,921 at the lower end to $9,085 at the 75th percentile — which tells you that insurers are pricing Howard properties very differently from one another. Finding the right insurer clearly matters here.

---

How Howard Compares

To understand just how well this quote performs, it helps to zoom out and look at the broader pricing landscape. Here's how Howard stacks up:

| Benchmark | Premium |

|---|---|

| This Quote | $2,536/yr |

| Howard Suburb Average | $5,999/yr |

| Howard Suburb Median | $4,349/yr |

| Fraser Coast LGA Average | $4,810/yr |

| QLD State Average | $9,129/yr |

| QLD State Median | $3,903/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

A few things stand out in this comparison. First, Queensland's state average of $9,129/year is extraordinarily high — nearly double the national average of $5,347/year. This reflects the reality that QLD carries significant natural hazard risk across much of the state, including cyclone exposure in the north, flood-prone river catchments, and severe storm corridors. The state median of $3,903/year is far more representative of what most Queenslanders actually pay, but the average is dragged up by high-risk coastal and northern postcodes.

Howard, sitting in the Fraser Coast LGA, benefits from a relatively moderate risk profile compared to many QLD postcodes. The Fraser Coast LGA average of $4,810/year is well below the state average, which is encouraging. At $2,536, this quote beats the LGA average by nearly $2,300.

Compared to national benchmarks, this quote also performs well — sitting below the national median of $2,764/year and less than half the national average. For a comprehensive home and contents policy with a $412,000 building sum insured, that's a solid outcome.

You can explore more QLD home insurance data here.

---

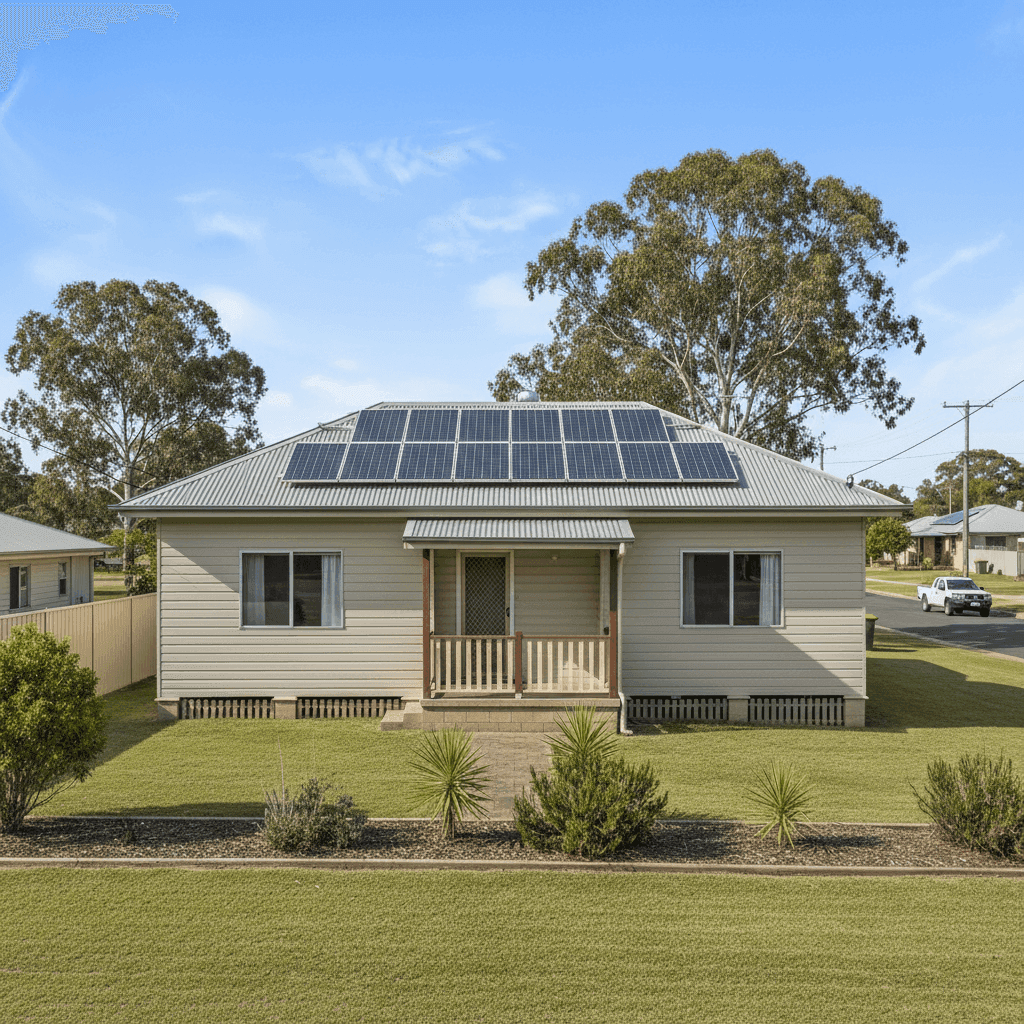

Property Features That Affect Your Premium

Several characteristics of this property work in its favour from an insurance pricing perspective.

Construction materials: The home features Hardiplank/Hardiflex external walls and a steel/Colorbond roof. Both are well-regarded by insurers. Fibre cement cladding like Hardieplank is fire-resistant, durable, and holds up well in Queensland's humid subtropical climate. Colorbond steel roofing is similarly valued — it's resistant to corrosion, handles heavy rain effectively, and is less susceptible to storm damage than some older roofing materials.

Slab foundation: A concrete slab foundation is generally viewed favourably by insurers. It reduces the risk of subfloor damage, pest intrusion, and certain types of water ingress that can affect homes on stumps or piers.

Construction year (2010): A home built in 2010 benefits from compliance with post-2006 Queensland building codes, which introduced stricter wind-load and structural requirements following cyclone events. This can positively influence how insurers assess the property's resilience.

No cyclone risk designation: Howard is not classified as a cyclone risk area, which is a meaningful factor in keeping premiums lower. Many QLD coastal and northern postcodes attract significant cyclone loading charges — the absence of this here is a genuine financial advantage.

Solar panels: The presence of solar panels adds some value to the property that needs to be accounted for in the sum insured. Most standard home policies cover rooftop solar as part of the building, but it's worth confirming this with your insurer. Damage to solar systems during storms is not uncommon in Queensland.

Ducted climate control: Ducted air conditioning systems are a higher-value fitting and can increase the cost to rebuild or repair — which is already factored into the $412,000 sum insured. Ensuring your building sum insured reflects the full replacement cost, including systems like this, is important to avoid underinsurance.

---

Tips for Homeowners in Howard

1. Don't assume your sum insured is correct — check it annually. Building costs have risen sharply in regional Queensland over recent years. A $412,000 sum insured may be appropriate today, but construction costs can shift quickly. Use a building calculator or speak to a local builder to verify your sum insured reflects current replacement costs — not just the market value of the home.

2. Confirm your solar panels are covered. Ask your insurer specifically whether your rooftop solar system is included under the building definition in your policy. Some policies cover it automatically; others may require it to be listed separately or may have sub-limits. Given that storm damage is a real risk in Queensland summers, this is worth clarifying upfront.

3. Review your contents sum insured regularly. At $45,000, the contents cover in this policy is on the modest side. Take a room-by-room inventory of your belongings — furniture, appliances, clothing, electronics, and tools — to make sure your contents sum insured reflects what it would actually cost to replace everything new. Many Australians are significantly underinsured on contents.

4. Compare quotes at renewal — every time. The wide spread of premiums in Howard (from under $4,000 to over $9,000 per year) tells you that insurers price this suburb very differently. Loyalty doesn't always pay in home insurance. Even if you're happy with your current insurer, it takes only a few minutes to compare quotes at CoverClub and confirm you're still getting a competitive rate.

---

Ready to Compare?

Whether you're renewing your policy or insuring a home for the first time, CoverClub makes it easy to see how your quote stacks up against real market data. Get a home insurance quote today and find out if you're paying a fair price — or leaving money on the table.