If you own a free standing home in Howard, QLD 4659, you already know that finding the right home insurance can feel like navigating a maze. Premiums vary wildly across Queensland — and the Fraser Coast region is no exception. In this article, we take a close look at a real home and contents insurance quote for a two-bedroom, one-bathroom free standing home in Howard, breaking down what the numbers mean and how this quote stacks up against local, state, and national benchmarks.

---

Is This Quote Fair?

The quote in question comes in at $2,735 per year (or $267 per month), covering both building and contents for a property insured at $520,000 for the building and $101,000 for contents, each with a $1,000 excess.

Our price rating for this quote? CHEAP — Below Average. That's a strong result.

To put it in perspective, the suburb average premium for Howard (4659) sits at $5,999 per year, with a median of $4,349. This quote comes in at less than half the suburb average — and well below even the 25th percentile of $3,921. In other words, fewer than one in four quotes in this suburb are this affordable. That's a genuinely competitive outcome.

At the Queensland state level, the average annual premium is a steep $9,129, though the state median is considerably lower at $3,903 — a sign that a small number of very high-risk properties are pulling the average up significantly. This quote beats both figures comfortably.

Zooming out to the national picture, the average Australian home insurance premium is $5,347 per year, with a national median of $2,764. This quote sits just below the national median — a strong result for a property in regional Queensland, where premiums can often be elevated due to weather-related risk factors.

In short: this is a well-priced quote. Whether you're a first-time buyer or a long-term homeowner in Howard, locking in a premium at this level would represent genuine value.

---

How Howard Compares

Howard is a small town in the Fraser Coast Local Government Area, situated roughly 270 kilometres north of Brisbane. It's a tight-knit community with a mix of older and newer residential properties — and its insurance market reflects that diversity.

| Benchmark | Annual Premium |

|---|---|

| This Quote | $2,735 |

| Howard Suburb Median | $4,349 |

| Howard Suburb Average | $5,999 |

| Fraser Coast LGA Average | $4,810 |

| QLD State Average | $9,129 |

| National Average | $5,347 |

| National Median | $2,764 |

(Based on a sample of 15 quotes collected for the Howard 4659 postcode.)

The wide gap between Howard's average ($5,999) and median ($4,349) suggests the local market has some outlier quotes pushing the average up — possibly properties with higher risk profiles, older construction, or elevated sum insured values. The 75th percentile sits at a striking $9,085 per year, which shows just how expensive insurance can get in this area for some homeowners.

This quote's position well below the 25th percentile ($3,921) is particularly noteworthy. It suggests the insurer has assessed this specific property favourably — and the property's features likely play a meaningful role in that outcome.

---

Property Features That Affect Your Premium

Several characteristics of this home work in its favour from an insurance pricing perspective:

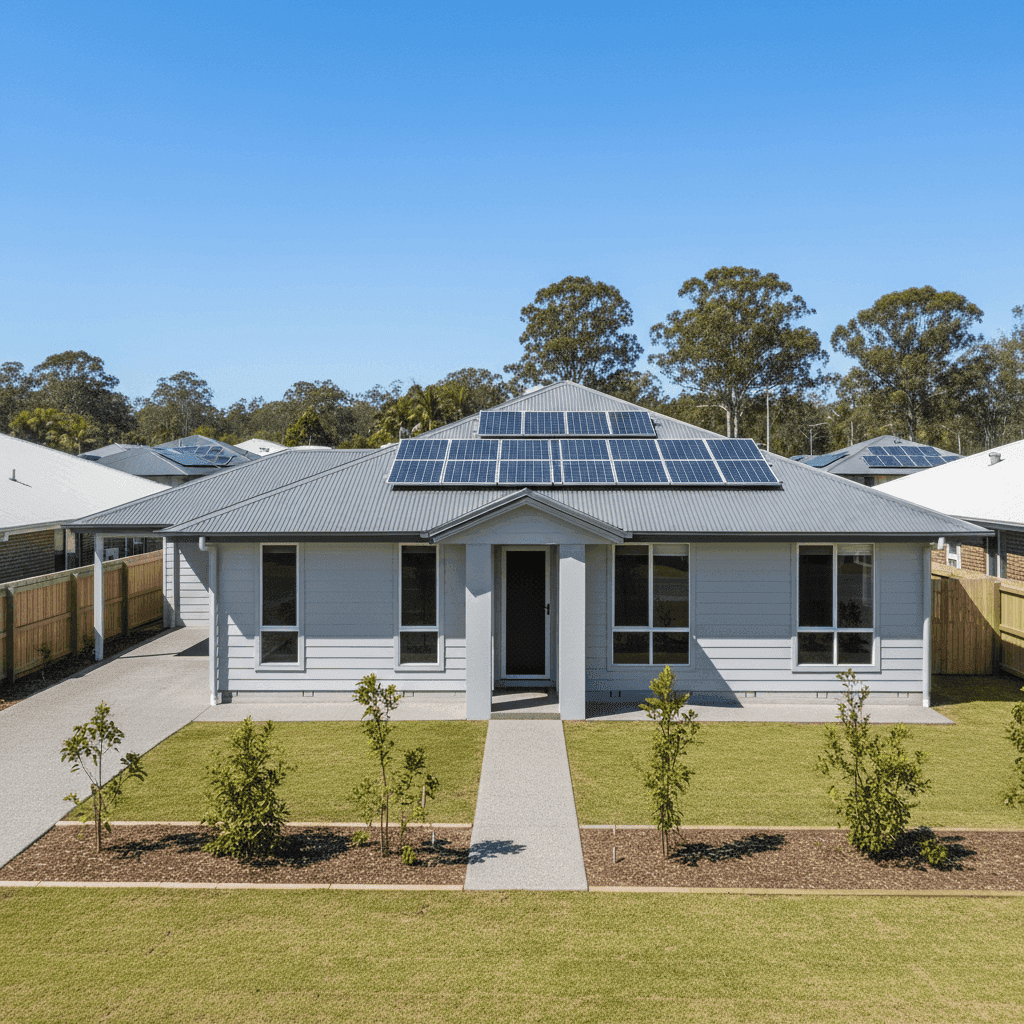

Hardiplank / Hardiflex External Walls Fibre cement cladding like Hardiplank is a popular choice in Queensland for good reason. It's resistant to rot, termites, and fire — all of which insurers view positively. Compared to older timber weatherboard homes, Hardiflex-clad properties often attract lower premiums.

Steel / Colorbond Roof Colorbond steel roofing is widely regarded as one of the most insurer-friendly roof types in Australia. It's durable, low-maintenance, and performs well in high winds and heavy rain. For a regional Queensland property, this is a meaningful risk-reduction factor.

Slab Foundation Concrete slab foundations are considered stable and low-risk by most insurers. They're less susceptible to subsidence and pest damage compared to raised or timber-framed stumped foundations common in older Queensland homes.

Construction Year: 1997 At just under 30 years old, this home sits in a sweet spot — modern enough to meet contemporary building standards, but not so new that it carries a premium replacement cost. Homes built in the late 1990s typically benefited from improved building codes introduced after Cyclone Tracy and the broader national shift toward more resilient residential construction.

Solar Panels The presence of solar panels adds some complexity to insurance. Panels themselves need to be covered (usually under building insurance), and their replacement cost should be factored into the sum insured. It's worth confirming with your insurer that solar panels are explicitly included in your policy and that the $520,000 building sum insured accounts for their replacement value.

Ducted Climate Control Ducted air conditioning systems are a fixed building feature and should be covered under building insurance. Again, it's worth verifying this is captured in your sum insured — particularly given the cost of ducted system replacement in regional areas.

No Pool, Vinyl Flooring, Standard Fittings The absence of a pool removes a common source of liability and maintenance claims. Vinyl flooring and standard fittings keep replacement costs predictable and moderate, which generally supports lower premiums compared to properties with high-end finishes.

---

Tips for Homeowners in Howard

1. Review Your Building Sum Insured Regularly Construction costs in regional Queensland have risen sharply in recent years. A sum insured of $520,000 for a 130 sqm home works out to approximately $4,000 per square metre — which is within a reasonable range for regional QLD, but worth reviewing annually. Underinsurance is one of the most common and costly mistakes homeowners make.

2. Confirm Solar Panel Coverage Not all policies automatically cover rooftop solar systems to their full replacement value. Check your Product Disclosure Statement (PDS) carefully and ask your insurer to confirm that your panels — and any associated inverter or battery storage — are included in your building cover.

3. Shop Around at Renewal Time Even if you're happy with your current premium, the insurance market shifts constantly. Given that Howard's suburb average is nearly double this quote's price, there's clearly significant variation between insurers in this postcode. Use a comparison tool like CoverClub at each renewal to ensure you're not drifting into overpriced territory.

4. Consider Your Excess Strategy Both the building and contents excess on this policy sit at $1,000 — a standard level. If you're financially comfortable absorbing a higher out-of-pocket cost in the event of a claim, increasing your excess to $2,000 or more can meaningfully reduce your annual premium. Conversely, if cash flow is a concern, a lower excess may be worth the slightly higher premium.

---

Get Your Own Quote

Whether you're in Howard or anywhere else across Australia, it pays to compare. CoverClub makes it easy to see what multiple insurers would charge for your specific property — so you can make an informed decision rather than just renewing on autopilot. Start comparing home insurance quotes today and find out whether your current premium is as competitive as this one.