If you own a free standing home in Huonville, TAS 7109, you're probably curious about what a fair home insurance premium looks like — and whether the quote sitting in your inbox is worth accepting. Huonville is the commercial heart of the Huon Valley, a region known for its apple orchards, cool temperate climate, and a growing community of tree-changers drawn from Hobart. It's a beautiful part of Tasmania, but like anywhere, the right home and contents cover is essential for protecting what matters most.

In this article, we analyse a real home and contents insurance quote for a 3-bedroom, 2-bathroom free standing home in Huonville and put it in context against local, state, and national benchmarks.

---

Is This Quote Fair?

The quote in question comes in at $1,798 per year (or $172/month), covering a building sum insured of $572,000 and contents valued at $221,000 — both with a $1,000 excess. Based on data from 47 quotes collected for Huonville (postcode 7109), this premium is rated CHEAP, sitting comfortably below the suburb average.

To put that in perspective:

- The suburb average is $2,869/yr — this quote is $1,071 cheaper

- The suburb median sits at $2,729/yr

- Even the 25th percentile (the cheapest quarter of quotes) is $1,991/yr — meaning this quote beats even the budget end of the local market

In short, $1,798/yr for this level of cover in Huonville represents genuine value. Homeowners who haven't shopped around recently may well be paying significantly more for equivalent protection.

---

How Huonville Compares

Understanding where Huonville sits in the broader insurance landscape helps frame just how competitive — or otherwise — local premiums are.

| Benchmark | Average Premium |

|---|---|

| Huonville (7109) | $2,869/yr |

| Derwent Valley LGA | $2,913/yr |

| Tasmania (state) | $2,814/yr |

| National | $5,347/yr |

Huonville premiums are broadly in line with the Tasmanian state average of $2,814/yr, which itself sits well below the national average of $5,347/yr. This reflects Tasmania's relatively lower exposure to some of the catastrophic weather events — cyclones, severe flooding, and extreme heatwaves — that drive up premiums in Queensland, Western Australia, and parts of New South Wales.

That said, Tasmania is not without its risks. Bushfire remains a real concern in rural and semi-rural areas, and Huonville's proximity to forested hillsides means insurers do factor in fire exposure when pricing policies. The Huon Valley also experiences significant rainfall, which can contribute to localised flooding and storm damage claims.

The Derwent Valley LGA average of $2,913/yr is slightly above the suburb figure, suggesting Huonville itself may be viewed as a marginally lower-risk pocket within the broader local government area.

---

Property Features That Affect Your Premium

Every property is unique, and insurers weigh up a range of characteristics when calculating your premium. Here's how the features of this particular home are likely to influence its pricing:

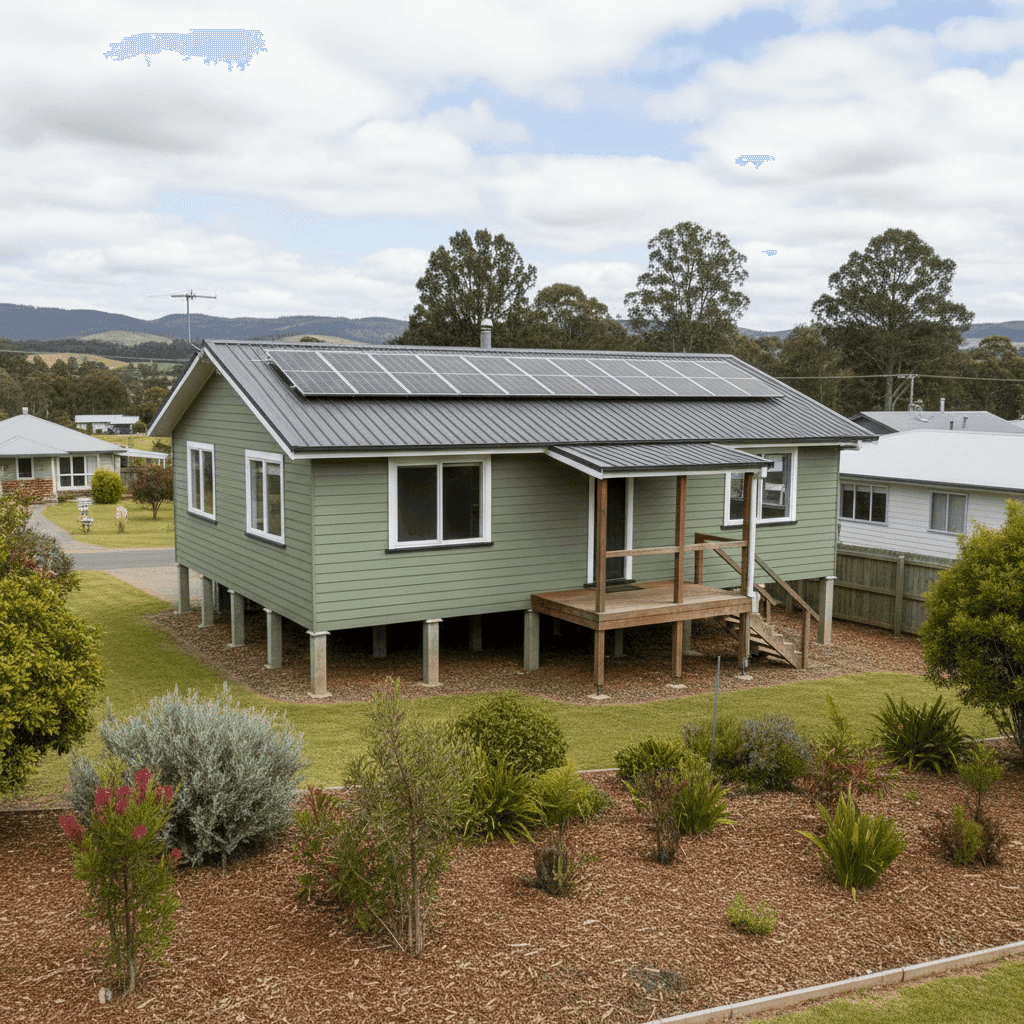

Age of construction (1920): At over 100 years old, this is a heritage-era home. Older properties can attract higher premiums due to the cost of sourcing period-appropriate materials and trades for repairs. However, if the home has been well maintained and upgraded over the decades, some insurers take a more favourable view.

Weatherboard timber walls: Weatherboard is a classic construction material in Tasmania and is widely insured, but it does carry a higher fire risk than brick or rendered cement. Insurers price this in, though it's a very common wall type in the region.

Steel/Colorbond roof: This is actually a positive from an insurer's perspective. Colorbond roofing is durable, low-maintenance, and performs well in high-wind and heavy-rain conditions. It's likely helping keep this premium competitive.

Stump foundations: Homes on stumps are common in older Tasmanian properties and can be associated with higher maintenance needs. Some insurers may apply a loading, particularly if the stumps are original timber rather than concrete or steel replacements.

Timber/laminate flooring: Timber floors add replacement value to a contents or building claim, but they're standard in this region and unlikely to significantly skew the premium.

Solar panels: The presence of solar panels adds to the insured value of the building and can affect premiums slightly upward, as panels themselves can be costly to replace. It's worth confirming your policy explicitly covers solar panel damage.

Ducted climate control: Ducted systems are a fixed building feature and should be included in your building sum insured. At $572,000, the sum insured here appears to account for the full rebuild cost of this 130 sqm home with its inclusions.

No pool, no cyclone risk zone: These two factors work in the homeowner's favour. Pools add liability and maintenance complexity, while cyclone-rated areas (predominantly in northern Australia) can dramatically increase premiums. Neither applies here.

---

Tips for Homeowners in Huonville

Whether you're reviewing an existing policy or shopping for the first time, here are four practical steps to make sure you're getting the best deal:

- Check your building sum insured annually. Construction costs have risen sharply in recent years. A sum insured of $572,000 for a 130 sqm home may be appropriate today, but it's worth reviewing each year to ensure you're not underinsured — especially with a heritage-era weatherboard home where rebuild costs can be higher than average.

- Ask about bushfire and storm cover specifics. Given Huonville's rural surroundings, make sure your policy clearly covers bushfire damage and storm-related events like fallen trees and water ingress. Not all policies treat these the same way.

- Review your stump and subfloor coverage. Homes on stumps can develop issues over time — termite damage, rot, or movement. Check whether your policy covers subfloor structures and under what circumstances.

- Confirm solar panel coverage. Solar panels are increasingly common but not always automatically covered under a standard building policy. Ask your insurer directly whether panels are included in your sum insured and whether accidental damage or storm damage to the system is covered.

---

Compare Home Insurance Quotes in Huonville

This quote is a strong example of what's possible when you take the time to compare. At $1,798/yr, it's well below what most Huonville homeowners are paying — but the only way to know if you're getting a similarly competitive deal is to check.

Get a home and contents quote at CoverClub and see how your current premium stacks up against the market in seconds. You can also explore detailed Huonville insurance statistics to better understand what your neighbours are paying.