Illawong is a leafy, sought-after suburb in Sydney's Sutherland Shire, known for its bushland surroundings, generous block sizes, and family-friendly streets. If you own a free standing home here, you're sitting on a significant asset — and protecting it with the right insurance policy is essential. This article breaks down a real home and contents insurance quote for a four-bedroom property in Illawong (NSW 2234), examines whether the premium is fair, and offers practical guidance for local homeowners looking to get better value.

---

Is This Quote Fair?

The quote in question comes in at $8,755 per year (or $839/month) for combined home and contents cover, with a building sum insured of $1,567,000 and contents valued at $192,000. Both the building and contents excess are set at $1,000.

Our price rating for this quote is Expensive — Above Average.

To understand why, it helps to look at the numbers in context. The average home and contents premium across Illawong sits at around $3,723 per year, with a median of $3,579. This quote is more than double that local average, which is a significant gap worth examining closely.

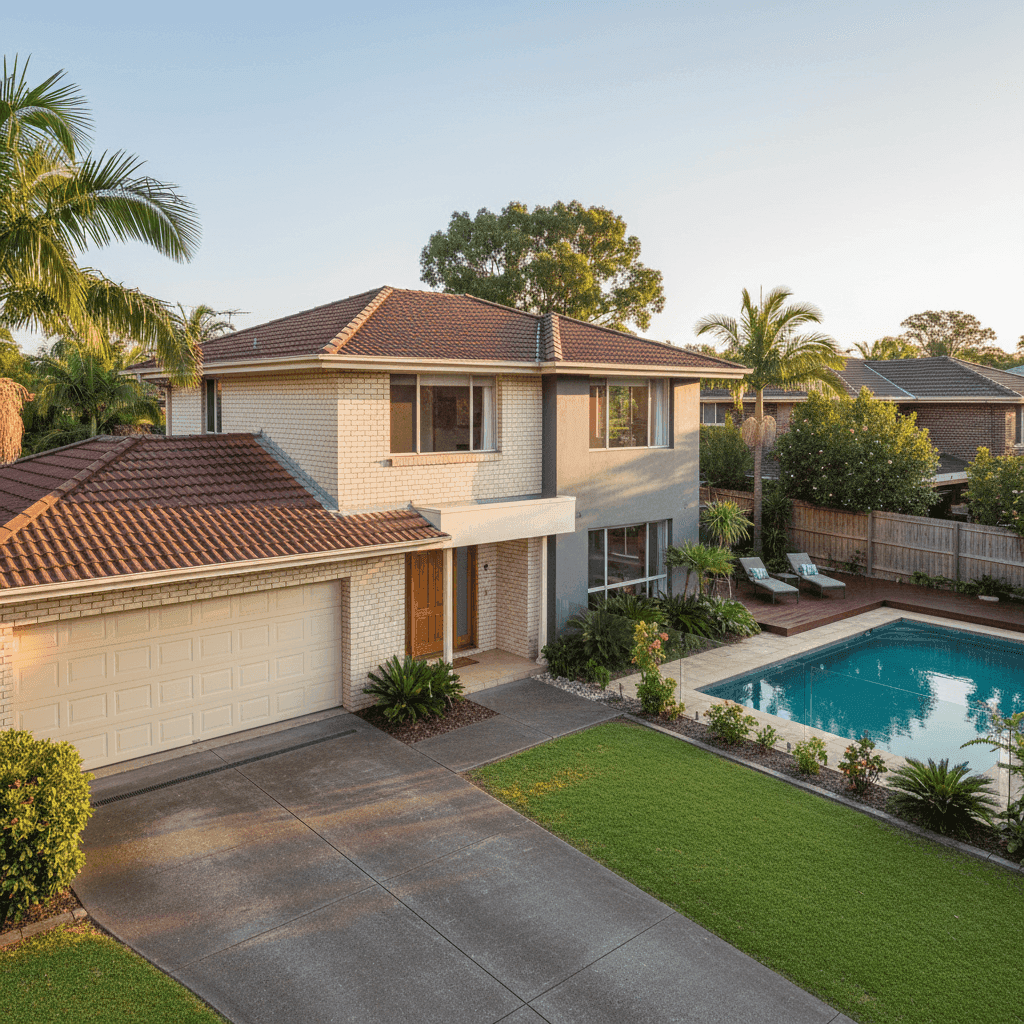

That said, the building sum insured of $1,567,000 is a major driver here. Larger, higher-value homes naturally attract higher premiums because the cost to rebuild in the event of a total loss is substantially greater. A 305 sqm brick veneer home with above-average fittings, a pool, and ducted climate control is not a standard suburban dwelling — it's a premium property, and the insurer is pricing it accordingly.

Still, even accounting for the property's size and value, this premium warrants a closer look. Comparing quotes from multiple insurers is always worthwhile, particularly when your annual outlay is approaching $9,000.

---

How Illawong Compares

Understanding where this quote sits relative to broader benchmarks gives a clearer picture of the insurance landscape. Here's how Illawong stacks up:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Illawong (NSW 2234) | $3,723/yr | $3,579/yr |

| NSW (State) | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

| Sutherland LGA | $23,423/yr | — |

(Based on [Illawong suburb data](https://coverclub.com.au/stats/NSW/2234/illawong), [NSW state data](https://coverclub.com.au/stats/NSW), and [national data](https://coverclub.com.au/stats/national) from CoverClub.)

A few things stand out here. The NSW state average of $9,528 is notably higher than the state median of $3,770 — a sign that a relatively small number of very high-value or high-risk properties are pulling the average upward. The Sutherland LGA average of $23,423 is extraordinary, likely skewed by prestige waterfront and large-acreage properties within the broader local government area.

The quote of $8,755 sits below the NSW state average and well below the Sutherland LGA average, which provides some reassurance. However, it remains well above the Illawong suburb average, suggesting there may be room to negotiate or shop around — particularly if the building sum insured can be reviewed for accuracy.

The suburb sample size of 63 quotes gives us reasonable confidence in the local data, placing this property in the upper tier of premiums for the area.

---

Property Features That Affect Your Premium

Several characteristics of this property directly influence the cost of cover. Understanding these factors can help you have more informed conversations with insurers.

Construction (1985, Brick Veneer, Tiled Roof, Slab Foundation)

Built in 1985, this home falls into a mid-aged category. Properties of this era are generally well-regarded by insurers — they're past the teething issues of new builds but haven't yet reached the age where major structural concerns become common. Brick veneer external walls are considered a solid, fire-resistant construction type that typically attracts favourable underwriting treatment. A tiled roof is similarly well-regarded for durability and weather resistance. The slab foundation is standard for the region and presents no unusual risk factors.

Size and Fittings Quality

At 305 sqm, this is a substantial home. Combined with above-average fittings quality — think stone benchtops, quality cabinetry, premium fixtures — the rebuild cost per square metre is meaningfully higher than a standard home. This directly justifies a higher building sum insured and, in turn, a higher premium.

Swimming Pool

The presence of a pool adds to the insurable risk. Pools can be expensive to repair or replace following storm damage, subsidence, or accidental damage, and they introduce liability considerations as well. Most insurers factor this into their pricing.

Ducted Climate Control

Ducted air conditioning is a significant fixed asset. Replacing a full ducted system can cost tens of thousands of dollars, and this is reflected in both the building sum insured and the premium calculation.

No Cyclone Risk

Illawong is not in a cyclone risk zone, which is a meaningful positive for premium pricing. Homeowners in northern Queensland, for example, face dramatically higher premiums due to cyclone exposure. This property benefits from the comparatively benign coastal Sydney climate.

---

Tips for Homeowners in Illawong

1. Review Your Building Sum Insured Carefully

The single biggest lever on your premium is the building sum insured. At $1,567,000, this figure should reflect the cost to rebuild — not the market value of the property. Engage a quantity surveyor or use an insurer's building calculator to verify this figure. Over-insuring is common and can mean you're paying a premium on coverage you'll never need.

2. Compare Quotes from Multiple Insurers

With an annual premium of $8,755, even a 15% saving represents over $1,300 per year. Get a quote through CoverClub to see how different insurers price your specific property — coverage terms, exclusions, and premiums can vary considerably.

3. Consider Your Excess Level

Both the building and contents excess are set at $1,000. Increasing your excess — to $2,000 or even $2,500 — can reduce your annual premium noticeably. This strategy works well if you have sufficient savings to cover a higher out-of-pocket cost in the event of a claim.

4. Bundle and Ask for Discounts

Many insurers offer discounts for bundling home and contents cover (which this policy already does), as well as loyalty discounts, security system discounts, and claim-free bonuses. It's worth asking your insurer directly what discounts are available — they're not always advertised upfront.

---

Ready to Compare?

Whether you're reviewing an existing policy or shopping for cover for the first time, comparing quotes is the most effective way to ensure you're getting fair value. CoverClub makes it easy to benchmark your premium against real data from your suburb and beyond. Start your comparison today and see what Illawong homeowners are actually paying for home and contents insurance.

For more local insights, explore the Illawong insurance stats page, the NSW state overview, or browse national home insurance data to see how your premium stacks up across the country.