Iluka is a coastal gem tucked at the mouth of the Clarence River in northern New South Wales — and like many sought-after seaside communities, insuring a home here comes with its own set of considerations. This article breaks down a real home and contents insurance quote for a two-bedroom, two-bathroom free-standing home in Iluka (postcode 2466), helping you understand what's driving the premium and whether it represents good value.

---

Is This Quote Fair?

The quote in question comes in at $5,366 per year (or $525 per month) for combined home and contents cover, with a building sum insured of $700,000 and contents valued at $70,000. The building excess is $2,000, and the contents excess is $1,000.

Our pricing analysis rates this quote as Fair — Around Average. That's a reasonable outcome, but "average" in Iluka still sits well above what most Australians pay for home insurance. To understand why, it helps to look at the numbers in context.

The quote lands almost exactly on the suburb average of $5,419 per year, and sits above the suburb median of $4,559. That means roughly half of comparable quotes in the area come in cheaper — though the spread is wide, with the 75th percentile reaching $6,495. In other words, this homeowner is paying less than a quarter of Iluka properties surveyed, which is a positive sign. You can explore the full local pricing picture on the Iluka suburb stats page.

---

How Iluka Compares

The price gap between Iluka and broader benchmarks is striking:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Iluka (2466) | $5,419/yr | $4,559/yr |

| Clarence Valley LGA | $6,052/yr | — |

| NSW | $3,801/yr | $3,410/yr |

| National | $2,965/yr | $2,716/yr |

At $5,366, this quote is 41% above the NSW average and 81% above the national average. That's a substantial gap — but not surprising for a coastal property in a regional area. Coastal locations across Australia attract higher premiums due to elevated exposure to storm, flood, and wind events, and Iluka is no exception.

Interestingly, this quote actually comes in below the Clarence Valley LGA average of $6,052, which suggests the property's specific characteristics are working in the homeowner's favour relative to some neighbours. Browse NSW insurance statistics or national benchmarks to see how your own situation stacks up.

---

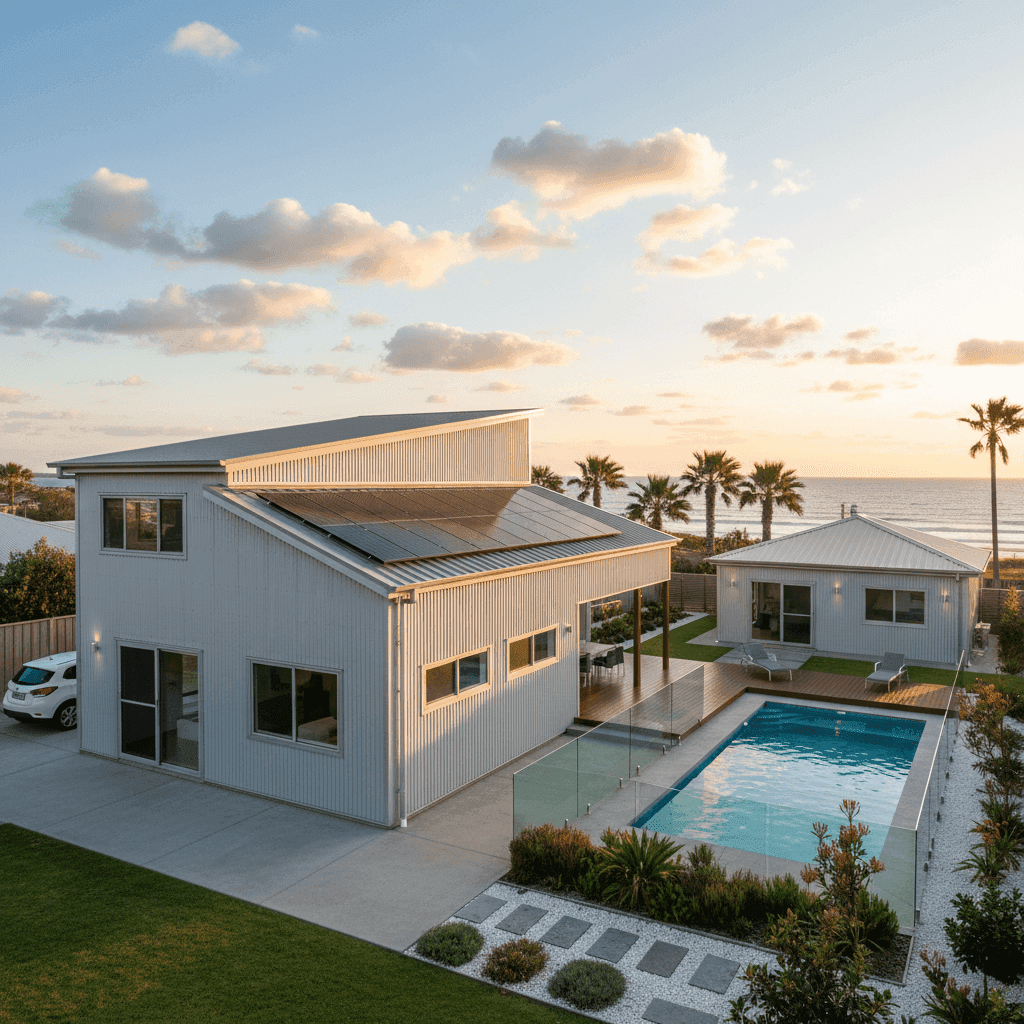

Property Features That Affect Your Premium

Several characteristics of this particular home have a meaningful influence on the premium quoted.

Modern Construction (2014 Build)

Homes built in 2014 benefit from relatively recent building codes, which generally means better structural integrity, improved fire resistance, and compliance with contemporary safety standards. Insurers typically view newer builds more favourably than older homes requiring ongoing maintenance.

Aluminium Cladding & Colorbond Roof

Aluminium external walls and a steel Colorbond roof are both considered durable, low-maintenance materials. Colorbond roofing in particular is highly regarded by insurers — it's resistant to fire, corrosion, and impact, and performs well in coastal environments where salt air can accelerate deterioration in lesser materials.

Slab Foundation

A concrete slab foundation is generally seen as structurally sound and resistant to subsidence, which can be a risk factor in some regional areas. It also eliminates the underfloor moisture and pest concerns associated with raised foundations.

Timber & Laminate Flooring

While aesthetically appealing and common in above-average-quality homes, timber and laminate flooring can be more susceptible to water damage than tiles. This is worth keeping in mind for a coastal property, where humidity and the occasional storm event can put floor coverings at risk.

Above-Average Fittings

The property's above-average fittings quality lifts the rebuild cost estimate, which is reflected in the $700,000 building sum insured. Higher-quality finishes — think stone benchtops, premium cabinetry, or designer fixtures — cost more to replace, and insurers price accordingly.

Pool, Solar Panels & Granny Flat

The swimming pool adds liability exposure and increases the overall replacement cost of the property. Solar panels, while an asset, introduce additional risk — particularly around electrical faults and storm damage to the panels themselves. The granny flat is a significant factor: it effectively adds a second dwelling to the policy, increasing both the rebuild cost and the contents footprint. Together, these extras meaningfully contribute to a premium that sits above the national norm.

---

Tips for Homeowners in Iluka

1. Review your building sum insured regularly Construction costs have risen sharply in recent years. A $700,000 sum insured may have been accurate at policy inception but could be under or over the mark today. Use a building cost calculator or speak with a quantity surveyor to confirm your coverage is still appropriate — being underinsured at claim time can be a costly mistake.

2. Consider a higher excess to reduce your premium With a $2,000 building excess, there may be room to adjust. Opting for a higher voluntary excess can meaningfully reduce your annual premium, particularly if you have the financial buffer to cover a larger out-of-pocket expense in the event of a claim.

3. Ask about bundling discounts Some insurers offer discounts when you hold multiple policies — for instance, combining home, contents, and landlord insurance (if the granny flat is tenanted). It's worth asking your insurer directly whether a bundled arrangement could reduce your overall cost.

4. Don't forget the granny flat in your contents assessment If the granny flat is occupied — whether by a family member or a tenant — make sure the contents coverage adequately reflects what's stored or furnished there. Many homeowners underestimate the value of contents in secondary dwellings, which can lead to a shortfall at claim time.

---

Compare Quotes and Find a Better Deal

Insurance premiums in coastal NSW can vary significantly between providers, even for identical properties. The best way to know whether you're getting a competitive rate is to compare. Get a home insurance quote through CoverClub and see how multiple insurers price your specific property — it takes just a few minutes and could save you hundreds of dollars a year.