Iluka is a coastal village at the mouth of the Clarence River in northern New South Wales — a place known for its World Heritage-listed rainforest, pristine beaches, and relaxed lifestyle. It's also a location where home insurance premiums reflect the realities of coastal living. If you own a free standing home in Iluka (postcode 2466), understanding what drives your insurance costs — and whether your quote stacks up — can save you hundreds of dollars a year.

This article breaks down a real home and contents insurance quote for a four-bedroom, two-bathroom free standing home in Iluka, compares it against local, state, and national benchmarks, and offers practical tips to help you get better value on your cover.

---

Is This Quote Fair?

The quote in question comes in at $4,327 per year (or $417/month) for combined home and contents cover, with a building sum insured of $395,000 and contents valued at $33,000. Both the building and contents excess are set at $5,000.

Our pricing engine rates this quote as Fair — Around Average, and the data backs that up. At $4,327, this premium sits just below the suburb median of $4,559/yr and meaningfully below the suburb average of $5,419/yr. In other words, this homeowner is paying less than what most comparable properties in Iluka attract — a solid outcome given the coastal location and the elevated risk profile that typically comes with it.

That said, "fair" doesn't necessarily mean "the best available." There's always room to compare, and even a modest saving of 10–15% on a premium at this level could put $430–$650 back in your pocket each year.

---

How Iluka Compares

To put this quote in proper context, it helps to look at the numbers across three levels: suburb, state, and nationally.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Iluka (2466) | $5,419/yr | $4,559/yr |

| NSW | $3,801/yr | $3,410/yr |

| National | $2,965/yr | $2,716/yr |

| Clarence Valley LGA | $6,052/yr | — |

A few things stand out immediately. Iluka premiums are significantly higher than the NSW average — roughly 43% above the state mean — and more than 80% higher than the national average. Even within the Clarence Valley LGA, Iluka sits below the LGA average of $6,052/yr, suggesting that some neighbouring areas carry even higher risk profiles.

The wide spread between Iluka's 25th percentile ($4,242/yr) and 75th percentile ($6,495/yr) tells an important story: there's considerable variation in what homeowners here are paying. The right insurer, the right policy structure, and the right property features can make a substantial difference to where you land in that range.

You can explore the full pricing data for Iluka at CoverClub's Iluka suburb stats page, compare it against NSW state-wide figures, or benchmark against national home insurance averages.

---

Property Features That Affect Your Premium

Every property is different, and insurers weigh up a range of construction and location factors when calculating your premium. Here's how the features of this particular home likely influence its pricing.

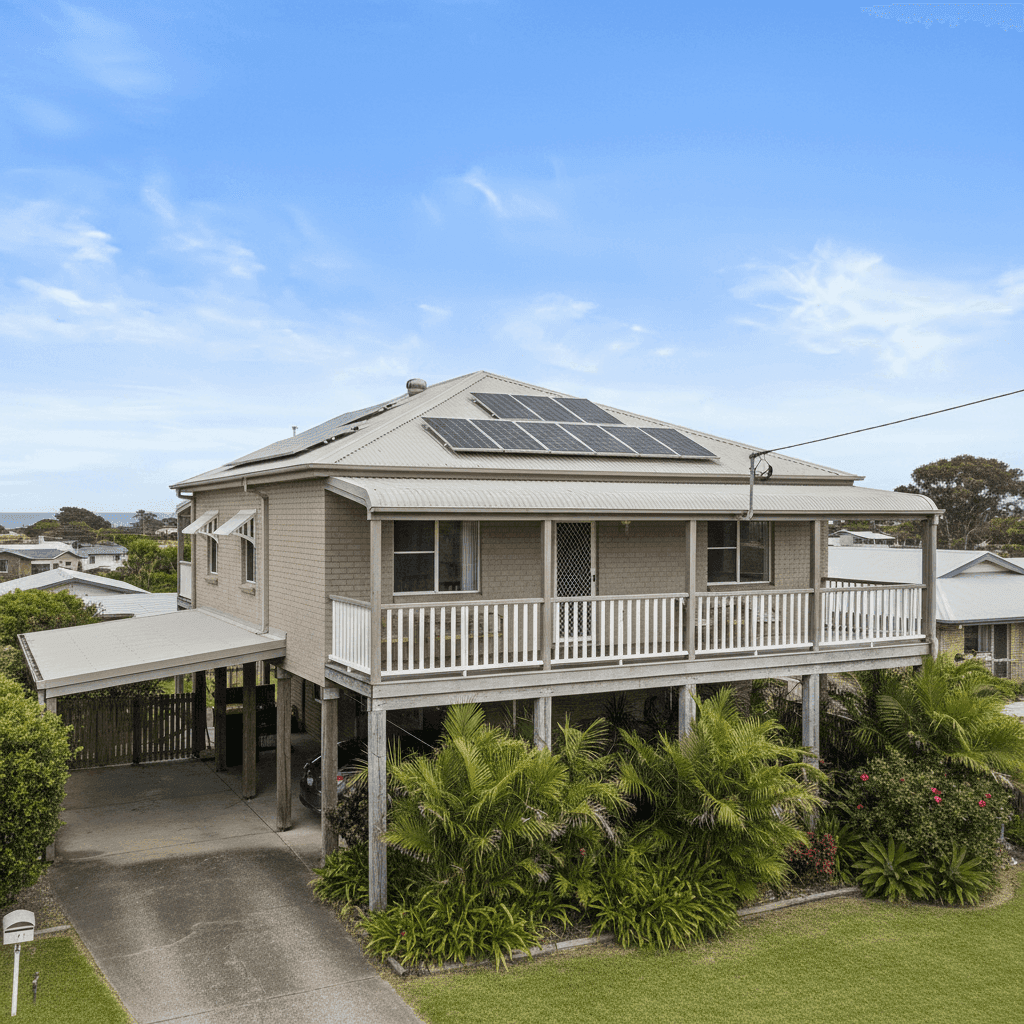

Double Brick Construction

Double brick walls are generally viewed favourably by insurers. They offer strong resistance to fire, wind, and general wear — all of which translate to lower risk of a major claim. This is one of the more premium-friendly features of this property.

Steel / Colorbond Roof

Colorbond roofing is a popular choice in coastal and regional Australia for good reason — it's durable, low-maintenance, and handles heat and rain well. Insurers typically rate it positively compared to older materials like terracotta or asbestos sheeting.

Elevated on Stumps

This is a particularly relevant feature for Iluka. Being elevated by at least one metre means the home sits above ground level, which can significantly reduce flood and storm inundation risk — a real concern in a low-lying coastal area near the Clarence River. Many insurers will price this more favourably than a slab-on-ground home in the same area.

Solar Panels

Solar panels add value to a property but also add replacement cost in the event of storm damage, hail, or fire. Insurers factor this into the building sum insured calculation, and it's important to ensure your $395,000 building cover adequately accounts for the panels.

Coastal Location

Iluka's position on the coast near the Clarence River mouth means exposure to salt air corrosion, storm surge risk, and periodic flooding. This is the primary reason premiums in this suburb run well above state and national norms — it's not a reflection of poor construction, but of geography.

Tiles and Standard Fittings

Tiled flooring and standard-quality fittings keep replacement costs at a manageable level. High-end finishes and specialty flooring can push rebuild costs — and therefore premiums — considerably higher.

---

Tips for Homeowners in Iluka

1. Review Your Building Sum Insured Annually

Construction costs in regional NSW have risen sharply in recent years. A sum insured of $395,000 may have been adequate when the policy was first taken out, but it's worth checking whether it still reflects the true cost to rebuild your home — including the solar panels, elevated stumps, and any improvements made since 2002. Underinsurance is one of the most common and costly mistakes homeowners make.

2. Consider Your Excess Carefully

Both the building and contents excess on this policy are set at $5,000 — which is on the higher end. A higher excess typically lowers your annual premium, but it means you'll need to cover more out of pocket before your insurer steps in. Make sure you have that amount readily accessible, and weigh up whether a lower excess (and slightly higher premium) might suit your financial situation better.

3. Compare Quotes Every Renewal

The 25th–75th percentile spread in Iluka ($4,242 to $6,495/yr) shows just how much variation exists between insurers for the same type of property. Don't assume your current insurer is offering you the best rate. Shopping around at renewal — or even mid-term — can uncover meaningful savings without sacrificing cover quality.

4. Document Your Contents Thoroughly

With $33,000 in contents cover, it's worth maintaining an up-to-date home inventory — photos, receipts, and serial numbers for valuables. In the event of a claim, especially after a storm or flood event, clear documentation can speed up the process and reduce disputes over item values.

---

Compare Your Home Insurance Quote Today

Whether you're a long-time Iluka local or you've recently made the move to this beautiful corner of the NSW coast, making sure you have the right cover at the right price is worth the effort. CoverClub makes it easy to compare home and contents insurance quotes from multiple insurers in minutes.

Get a quote now at CoverClub and see how your current premium stacks up — you might be surprised at what's available.