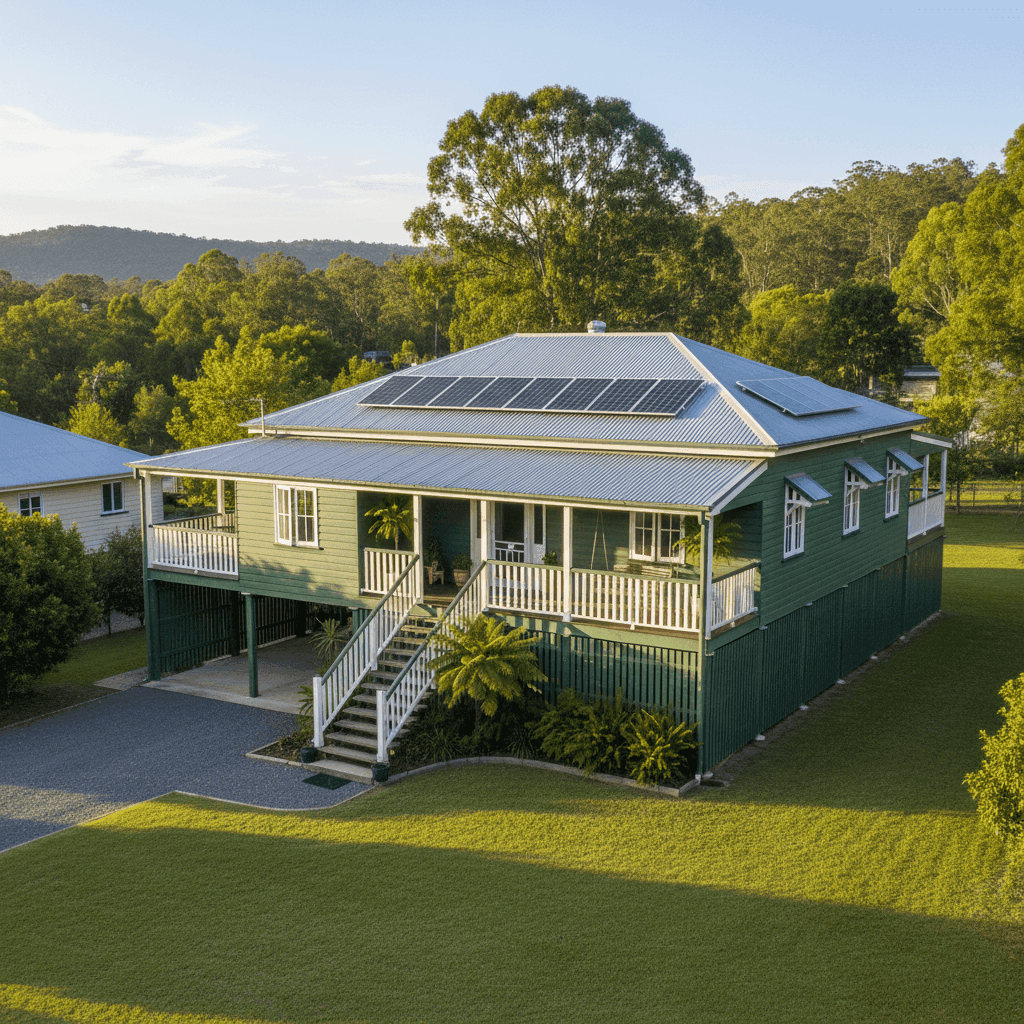

Imbil is a quiet hinterland township nestled in the Sunshine Coast's rural interior, surrounded by state forest and the waters of Lake Baroon. It's the kind of place where older character homes sit comfortably on large blocks — and this 2-bedroom, 1-bathroom free-standing home built in 1926 is a classic example of the region's heritage housing stock. But what does it actually cost to insure a property like this, and is the quoted premium a good deal? Let's take a close look.

---

Is This Quote Fair?

The annual premium for this building-only policy comes in at $2,266 per year (or $228/month), with a building sum insured of $350,000 and a $3,000 excess. CoverClub's pricing engine rates this quote as Fair — Around Average.

To put that in context:

- The suburb average for Imbil (postcode 4570) sits at $4,985/yr, with a median of $4,372/yr

- The 25th percentile for the suburb is $1,841/yr, and the 75th percentile reaches $6,621/yr

- This quote lands between the 25th and 75th percentile — closer to the lower half of the range

So while "Fair" might sound underwhelming, it's actually a solid result. At $2,266/yr, this premium is well below both the suburb average and median, suggesting the homeowner is paying meaningfully less than most others in the same postcode. The "Around Average" label reflects the broader national picture, where this premium sits closer to the middle of the pack.

---

How Imbil Compares

One of the most striking takeaways from this quote is just how expensive home insurance in Imbil tends to be relative to state and national benchmarks — and how this particular quote bucks that trend.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Imbil (4570) | $4,985/yr | $4,372/yr |

| Queensland | $4,547/yr | $3,931/yr |

| National | $2,965/yr | $2,716/yr |

| Fraser Coast LGA | $3,385/yr | — |

A few things stand out here. First, Imbil's suburb average of $4,985/yr is higher than the Queensland state average of $4,547/yr — which is itself already well above the national average. This tells us that Imbil carries above-average risk in the eyes of insurers, likely driven by a combination of factors including flood exposure, the prevalence of older timber homes, and the region's bushfire risk profile.

Second, the national median of $2,716/yr is a useful anchor. At $2,266/yr, this quote sits below the national median, which is a genuinely competitive outcome for a property in a suburb where premiums routinely exceed $4,000–$5,000 per year.

The Fraser Coast LGA average of $3,385/yr also provides useful context — this quote comes in roughly $1,100 below the LGA average, further reinforcing that the pricing here is on the favourable end of the spectrum for the area.

---

Property Features That Affect Your Premium

Several characteristics of this property are worth unpacking, as they each play a role in how insurers price the risk.

Age and Construction (Built 1926, Weatherboard Timber Walls)

At nearly 100 years old, this home is firmly in heritage territory. Older weatherboard homes are generally considered higher risk by insurers — timber is more susceptible to fire, rot, and pest damage than modern materials like brick veneer or fibre cement. Replacement costs can also be higher due to the need for period-appropriate materials and craftsmanship. This likely pushes the premium upward compared to a newer brick home of similar size.

Steel / Colorbond Roof

On the positive side, a Colorbond steel roof is viewed favourably by most insurers. It's durable, fire-resistant, and performs well in severe weather. This is a meaningful offset to the risk profile of the timber walls and the home's age.

Elevated on Stumps (At Least 1 Metre)

Being elevated by at least one metre on stumps is a significant factor in flood-prone regions of Queensland. Elevation reduces the likelihood of floodwater entering the living areas of the home, which can translate to lower flood-related risk assessments. For a property in the Sunshine Coast hinterland — where river and creek flooding can be a real concern — this feature may be contributing to the more competitive premium.

Solar Panels

The presence of solar panels adds replacement value to the building sum insured. Insurers factor in the cost of repairing or replacing panels after events like hailstorms, falling debris, or fire. It's worth confirming with your insurer that your solar system is explicitly covered under the building policy.

Building Size (130 sqm) and Fittings Quality (Standard)

At 130 sqm with standard fittings, this is a modest home by most measures. Smaller floor area and standard (rather than premium) fixtures generally result in a lower sum insured requirement and, by extension, a more manageable premium.

---

Tips for Homeowners in Imbil

1. Review Your Sum Insured Regularly

Construction costs have risen sharply across Queensland in recent years. A sum insured of $350,000 for a 130 sqm home may be adequate today, but it's worth reassessing annually — particularly for an older weatherboard home where specialised trades may be required for repairs. Underinsurance is one of the most common and costly mistakes homeowners make.

2. Confirm Flood Cover Is Included

Imbil sits within a catchment that can experience significant rainfall events. Make sure your policy explicitly includes flood cover (as distinct from storm surge or rainwater runoff). Not all standard building policies include flood by default — always check the Product Disclosure Statement (PDS).

3. Take Advantage of Your Elevated Foundation

If you haven't already, document your home's elevation and provide this detail when obtaining quotes. Some insurers offer more competitive pricing for elevated homes in flood-risk areas, and this information can make a meaningful difference to your premium.

4. Shop Around — The Spread in Imbil Is Wide

With a 25th percentile of $1,841/yr and a 75th percentile of $6,621/yr, there is an enormous range of premiums being charged for homes in this postcode. That spread of nearly $4,800 between the cheapest and most expensive quartiles means that comparing multiple quotes is especially valuable here. Don't assume your renewal price is competitive just because it feels familiar.

---

Compare Your Home Insurance Quote Today

Whether you're insuring a heritage weatherboard cottage or a modern build, the best way to know if you're getting a fair deal is to compare. Get a home insurance quote at CoverClub and see how your premium stacks up against real data from your suburb, your state, and across Australia. With transparent pricing benchmarks and independent comparisons, CoverClub makes it easy to make a confident, informed decision.