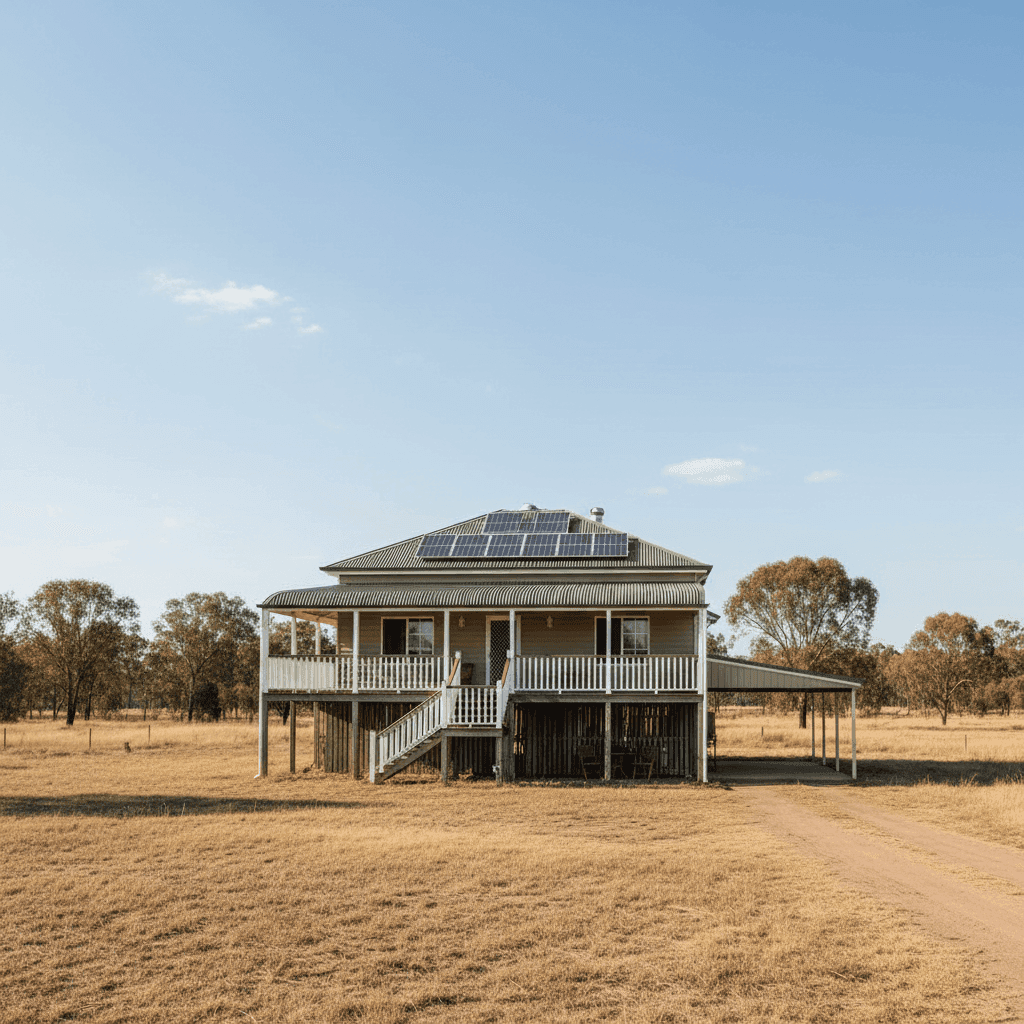

If you own a free standing home in Inglewood, QLD 4387, you've probably noticed that home insurance doesn't come cheap in this part of Queensland. Inglewood is a small inland town in the Goondiwindi Local Government Area, and like much of regional Queensland, its insurance premiums reflect a unique combination of property characteristics, local risk factors, and limited market competition. This article breaks down a real building insurance quote for a 2-bedroom, 1-bathroom free standing home in Inglewood — and helps you understand exactly what's driving the cost.

---

Is This Quote Fair?

The quote in question comes in at $6,574 per year (or $623/month) for building-only cover, with a $1,000 building excess and a sum insured of $509,000. Our price rating for this quote is FAIR — Around Average.

That "fair" rating is meaningful. It doesn't mean cheap, and it doesn't mean overpriced — it means this premium sits in a reasonable range given the suburb's pricing landscape. For homeowners who haven't compared their policy in a while, paying around average is actually a better outcome than many realise; a significant proportion of Australians are quietly overpaying on renewal without ever checking.

That said, "fair" still leaves room for improvement. Depending on which insurer you approach and how your property details are assessed, there may be scope to bring this premium down — particularly if you're willing to shop around or adjust your excess.

---

How Inglewood Compares

To put this quote in proper context, it helps to look at the numbers across three levels: suburb, state, and national.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Inglewood (QLD 4387) | $8,091/yr | $7,911/yr |

| Queensland (State) | $4,547/yr | $3,931/yr |

| Australia (National) | $2,965/yr | $2,716/yr |

| Goondiwindi LGA | $6,634/yr | — |

A few things stand out immediately. At $6,574/yr, this quote is actually below the Inglewood suburb average of $8,091 and below the suburb median of $7,911 — which is a positive sign. It also sits below the Goondiwindi LGA average of $6,634, putting it in a competitive position locally.

However, zoom out and the picture changes. Queensland's state average sits at $4,547/yr, meaning this Inglewood quote is roughly 45% higher than the typical Queensland premium. Compared to the national average of $2,965/yr, it's more than double. This gap isn't unusual for regional and inland Queensland towns, where older housing stock, storm risk, and limited insurer appetite can all push premiums upward.

For a detailed breakdown of what other homeowners in this postcode are paying, visit the Inglewood suburb insurance stats page. You can also explore Queensland-wide home insurance data or check out national home insurance benchmarks to see how your region stacks up.

It's worth noting the sample size for Inglewood is 18 quotes — a relatively small dataset. The 25th percentile sits at $5,614/yr and the 75th percentile at $10,677/yr, which is a wide spread. This tells us insurers are pricing this suburb quite differently from one another, making comparison shopping especially valuable here.

---

Property Features That Affect Your Premium

Several characteristics of this particular home have a direct bearing on the premium quoted. Understanding them can help you anticipate costs and make informed decisions.

Fibro Asbestos External Walls

This is arguably the most significant risk factor for insurers. Homes built with fibro asbestos (common in Queensland homes constructed before the mid-1980s) are more expensive to insure because of the specialist handling and disposal requirements if the material is damaged. Repairs cannot be done by standard tradespeople — licensed asbestos removalists must be engaged, which adds substantially to claim costs. With a construction year of 1960, this property falls squarely into that era.

Age of Construction (1960)

A 64-year-old home carries inherent risks around ageing plumbing, wiring, and structural components. Insurers factor this in when calculating the likelihood and potential cost of a claim. Older homes are also more likely to have features — like the fibro walls mentioned above — that complicate repairs.

Elevated on Stumps

The property is elevated by at least 1 metre on stumps, which is a classic Queensland design. While elevation can actually offer some protection from localised flooding or moisture, stump foundations require ongoing maintenance. Insurers may factor in the risk of subsidence or structural movement over time, particularly in homes of this age.

Steel/Colorbond Roof

This is a positive from an insurance perspective. Colorbond roofing is durable, fire-resistant, and performs well in storm conditions compared to older materials like terracotta tiles or corrugated iron. It's likely helping to keep this premium more competitive than it might otherwise be.

Solar Panels

Solar panels are listed as a feature of this property. Most building insurance policies will cover rooftop solar panels as part of the building sum insured, but it's worth confirming this with your insurer. The panels add replacement value to the structure, which may be reflected in the $509,000 sum insured.

Ducted Climate Control

Ducted air conditioning systems are another fixed asset that forms part of the building's insured value. Like solar panels, these systems should be explicitly confirmed as covered under your policy, as some insurers treat them differently depending on how they're installed.

---

Tips for Homeowners in Inglewood

1. Don't Accept Your Renewal Without Comparing

Given the wide spread of premiums in this suburb — from $5,614 at the 25th percentile to $10,677 at the 75th — there's clearly significant variation between insurers. If you're currently paying above the suburb average, a quick comparison could save you thousands annually.

2. Get an Asbestos Assessment

If you haven't already, having a licensed asbestos assessor document the condition and location of any asbestos-containing materials in your home can be valuable. Some insurers look more favourably on properties with a current asbestos register, as it demonstrates proactive risk management.

3. Review Your Sum Insured Carefully

At $509,000 for a 105 sqm home with fibro asbestos walls, the sum insured needs to account for the elevated cost of asbestos-safe demolition and rebuild. Make sure your sum insured reflects current building costs in regional Queensland — these have risen sharply in recent years. Underinsurance is a real risk, particularly for older homes with specialist materials.

4. Consider a Higher Excess to Reduce Premiums

If your financial situation allows, opting for a higher excess (say, $2,000 or $2,500 instead of $1,000) can meaningfully reduce your annual premium. This strategy works best for homeowners who have emergency savings to cover a larger out-of-pocket cost in the event of a claim.

---

Ready to Compare?

Whether you're reviewing your current policy or insuring for the first time, comparing multiple quotes is the single most effective way to ensure you're not overpaying. CoverClub makes it easy to see real quotes from a range of insurers side by side. Get a home insurance quote today and find out if you can do better than average in Inglewood.